|

Home > About FDIC > Financial Reports > 1998 Annual Report |

|||

|

1998 Annual Report |

||

Condition of the Funds |

The FDIC administers two deposit insurance funds, the Bank Insurance Fund (BIF) and the Savings Association Insurance Fund (SAIF). The agency also manages a third fund fulfilling the obligations of the former Federal Savings and Loan Insurance Corporation (FSLIC), called the FSLIC Resolution Fund (FRF). On January 1, 1996, the FRF assumed responsibility for the assets and obligations of the Resolution Trust Corporation (RTC). The economic environment in 1998 remained favorable for the banking and thrift industries, resulting in relatively few problem institutions, high profitability and increased capitalization. During the third quarter, a default in Russian debt and the resulting difficulties with hedge funds, such as those experienced by Long Term Capital Management, LP, illustrated the speed with which financial market volatility and foreign sector developments can affect insured institutions. During 1998, some insured institutions continued to increase their exposures to an economic downturn through higher-risk lending and other practices. This is suggested by evidence of weakening underwriting standards, narrower interest-rate spreads, and increased concentrations in higher-risk loans. The potential effect of these trends on the deposit insurance funds depends on the nature of any national or regional economic downturns. An overview of the funds’ performance during 1998 follows. (Full details about the funds appear in the financial statements).

For more details on the Savings Association Insurance Fund (SAIF), please click here.

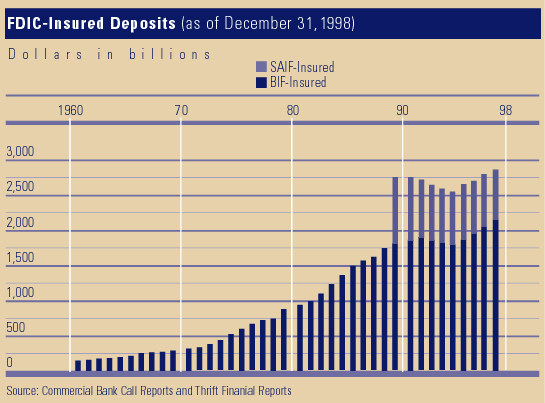

With banks experiencing another highly profitable year and only three bank failures, 1998 was another positive year for the BIF, despite adverse trends in the global economic picture. The BIF has grown steadily from a negative fund balance of $7 billion at year-end 1991 to $29.6 billion at year-end 1998. The 1998 fund balance represents a 4.7 percent increase over the 1997 balance of $28.3 billion. BIF-insured deposits grew by 4.1 percent in 1998, yielding a reserve ratio of 1.38 percent of insured deposits at year-end 1998, unchanged from year-end 1997. Deposit insurance assessment rates in 1998 were unchanged from 1997. For both semiannual assessment periods in 1998, the Board voted to retain rates ranging from 0 to 27 cents annually per $100 of assessable deposits. Under these rates, 95.1 percent of BIF-member institutions, or 8,808 institutions, were in the lowest-risk assessment rate category and paid no deposit-insurance assessments for the second semiannual assessment period of 1998. This rate schedule resulted in an average 1998 BIF rate of 0.08 cents per $100 of assessable deposits. As in 1997, interest earned on U.S. Treasury investments ($1.7 billion) exceeded assessment revenue ($22 million) and was the primary source of revenue for the BIF in 1998. This was a result of minimal insurance losses and receivership activity, the continued low assessment rate schedule and the concentration of institutions in the lowest-risk category. Bank failures continued to be minimal in 1998. Only three BIF-member institutions, with assets totaling $370 million, failed during the year. In 1997, one BIF-member institution with assets of $25.9 million failed. Estimated insurance losses of the banks that failed in 1998 were $179 million, compared to $4 million in estimated losses for the one failure in 1997. For the BIF in 1998, investments in U.S. Treasury obligations continued to be the main component of total assets, at 94.4 percent, compared to 93.8 percent in 1997. The financial position of the BIF continued to improve as cash and investments at year-end were 92 times total liabilities, up from 85.6 times the total liabilities in 1997. In 1998, the BIF had operating expenses of $697.6 million and net income of $1.3 billion, compared to operating expenses of $605 million and net income of $1.4 billion in 1997.

Savings Association Insurance Fund The SAIF ended 1998 with a fund balance of $9.8 billion, a 5.0 percent increase over the year-end 1997 balance of $9.4 billion. Estimated insured deposits increased by 2.8 percent in 1998. During the year, the reserve ratio of the SAIF grew from 1.36 percent of insured deposits to 1.39 percent. For both semiannual assessment periods of 1998, the Board retained the rate schedule in effect for 1997, a range of 0 to 27 cents annually per $100 of assessable deposits. Under this schedule, the percentage of SAIF-member institutions that paid no assessments increased from 90.9 percent in the first semiannual assessment period to 91.9 percent in the second half of the year, as more institutions qualified for the lowest-risk assessment rate category. This rate schedule resulted in an average 1998 SAIF rate of 0.21 cents per $100 of assessable deposits. The SAIF earned $15 million in assessment income in 1998, compared to $563 million in interest income. In 1998, the SAIF had operating expenses of $85 million and net income of $467 million, compared to operating expenses of $72 million and net income of $480 million in 1997. For the second consecutive year, no SAIF-member institution failed in 1998. Under the Deposit Insurance Funds Act of 1996, the FDIC must set aside all SAIF funds above the statutorily required Designated Reserve Ratio (DRR) of 1.25 percent of insured deposits in a Special Reserve on January 1,1999. No assessment credits, refunds or other payments can be made from the Special Reserve unless the SAIF reserve ratio falls below 50 percent of the DRR and is expected to remain below 50 percent for the following four quarters. Effective January 1,1999, the Special Reserve was funded with $978 million, reducing the SAIF unrestricted fund balance to $8.9 billion and the SAIF reserve ratio to 1.25 percent. The SAIF Special Reserve was mandated by Congress in the Deposit Insurance Funds Act. It was not proposed in order to address any deposit-insurance issues. However, by eliminating any cushion above the DRR, the creation of the Special Reserve on January 1, 1999, increases the likelihood of the SAIF dropping below the DRR. This, in turn, increases the possibility that the FDIC would be required to raise SAIF assessment rates sooner or higher than BIF assessment rates, resulting in an assessment rate disparity between the SAIF and the BIF. In 1998, legislation that would have eliminated the Special Reserve was introduced in the Congress but did not pass.

The FRF was established by law in 1989 to assume the remaining assets and obligations of the former FSLIC arising from thrift failures before January 1,1989. Congress placed this new fund under FDIC management on August 9, 1989, when FSLIC was abolished. On January 1,1996, the FRF also assumed the RTC’s residual assets and obligations. Today, the FRF consists of two distinct pools of assets and liabilities. One pool, composed of the assets and liabilities of the FSLIC, transferred to the FRF upon the dissolution of the FSLIC on August 9,1989 (FRF-FSLIC). The other pool, composed of the RTC’s assets and liabilities, transferred to the FRF on January 1, 1996 (FRF-RTC). The assets of one pool are not available to satisfy obligations of the other. The FRF-FSLIC had resolution equity of $2.098 billion as of December 31, 1998, and the FRF-RTC had resolution equity of $8.224 billion as of that date. |

| FDIC HOME | TOP OF REPORT | CONTENTS | PREVIOUS PAGE | NEXT PAGE |

| Last Updated 03/21/2000 | communications@fdic.gov |