Standing between the FDIC and the risks we have described is an array of private sector

and supervisory risk controls. By the end of the 1990s, it was clear that these

risk-mitigating tools were undergoing significant change. There was substantial discussion

about the implications of these trends for capital regulation, but discussions about the

implications for deposit insurance were in their infancy.Private sector risk management

strategies evolved considerably during the 1990s. An ongoing dialogue that included the

accounting profession, the financial regulatory community, and leading financial

institution practitioners resulted in a significant increase in the degree to which best

practices in risk management were formalized and made available. Quantitative tools to

measure and monitor risk became more sophisticated as well. Asset-liability management

software to assist in the evaluation and control of interest rate risk is now readily

available to financial institutions; market risks are being measured in real time through

value-at-risk models and other approaches; and credit risk modeling and measurement is

becoming more rigorous. As the decade closed, the risks identified through these tools

were being managed with financial instruments and financial technologies that did not

exist twenty years earlier.

Bank supervisors have long emphasized that the successful management of bank risk is

ultimately a function of the stewardship provided by bank management. During the 1990s,

the operational and policy implications of this philosophy began to be explored more

fully.

Supervisors placed more emphasis on

risk-focused loan review and transaction testing for the purpose of validating policies

and procedures, with more detailed testing where there was evidence of a need for further

review. In the arena of large or publicly traded banks, there was a clear policy momentum

towards improving the quality of management’s public disclosures, in order to enhance

the potential risk-mitigating effects of private market discipline.

The impact of these trends in risk management on

the FDIC’s losses will depend on the frequency of instances where specific aspects of

risk control systems do not work as intended. Thus, we should be concerned with any

systemic trend that increases the likelihood of such breakdowns. For example, we have seen

some cases where the opportunities to generate revenue inherent in a long expansion –

and the competitive pressures to do so – have led banks to compromise or neglect

important aspects of risk-management discipline. Warnings from the Securities and Exchange

Commission about the danger that some accounting firms may be compromising their

auditing business in favor of more lucrative consulting opportunities may provide another

example of a systemic trend towards an increasing volatility of risk-management outcomes.

Given these trends, it can be expected that the FDIC’s pricing and evaluation of risk

will, over time, continue to place heavy emphasis on identifying the quality of

banks’ risk controls.

| Risk-Related Premiums |

| The following tables

show the number and percentage of institutions insured by the Bank Insurance Fund (BIF)

and the Savings Association Insurance Fund (SAIF), according to risk classifications

effective for the first semiannual assessment period of 2000. Each institution is

categorized based on its capitalization and a supervisory subgroup rating (A, B, or C),

which is generally determined by on-site examinations. Assessment rates are basis points,

cents per $100 of assessable deposits, per year. |

| BIF Supervisory Subgroupsl |

|

A |

|

B |

|

C |

| Well

Capitalized: |

|

Assessment Rate |

0 |

|

3 |

|

17 |

|

Number of Institutions |

8,291

(93.7%) |

|

329

(3.7%) |

|

50 (0.6%) |

| Adequately

Capitalized: |

|

|

|

|

|

|

Assessment Rate |

3 |

|

10 |

|

24 |

|

Number of Institutions |

150

(1.7%) |

|

12 (0.1%) |

|

10 (0.1%) |

| Undercapitalized: |

|

|

|

|

|

|

Assessment Rate |

10 |

|

24 |

|

27 |

|

Number of Institutions |

2 (0.0%) |

|

0 (0.0%) |

|

8 (0.1%) |

|

| SAIF Supervisory Subgroupsn |

| Well

Capitalized: |

|

|

|

|

|

|

Assessment Rate |

0 |

|

3 |

|

17 |

|

Number of Institutions |

1,271

(91.6%) |

|

77 (5.5%) |

|

6 (0.4%) |

| Adequately

Capitalized: |

|

|

|

|

|

|

Assessment Rate |

3 |

|

10 |

|

24 |

|

Number of Institutions |

21 (1.5%)

|

|

5 (0.4%) |

|

7 (0.5%) |

| Undercapitalized: |

|

|

|

|

|

|

Assessment Rate |

10 |

|

24 |

|

27 |

|

Number of Institutions |

0 (0.0%) |

|

0 (0.0%) |

|

1 (0.1%) |

| l BIF data exclude SAIF-member "Oakar"

institutions that hold BIF-insured deposits. The assessment rate reflects the rate for

BIF-assessable deposits, which remained the same throughout 1999.

n SAIF

data exclude BIF-member "Oakar" institutions that hold SAIF-insured deposits.

The assessment rate reflects the rate for SAIF-assessable deposits, which remained the

same throughout 1999. |

|

|

A

New Legislative Framework  |

By a combination of legislative changes, regulatory choices and economic events, the

funding and pricing of FDIC insurance evolved during the 1980s and 1990s into something

fundamentally different from what existed during the first 50 years of the FDIC’s

history. The banking crisis of the 1980s led to two major pieces of legislation, the

Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA) and the FDIC

Improvement Act of 1991 (FDICIA). These laws have significantly changed the way the FDIC

conducts business in a number of areas, including the institutions it insures, the

insurance funds it administers, its enforcement powers, and the manner in which it

resolves failing institutions. Most noteworthy for the purposes of this article are two

requirements laid down by FDICIA: i) that the FDIC price insurance according to the risks

posed by individual institutions, in order to mitigate the moral hazard problems that can

attend any deposit insurance system; and ii) that it maintain the funds at designated

reserve ratios. The FDIC implemented its

risk-based deposit insurance premium system in 1993, the Bank Insurance Fund achieved its

designated reserve ratio in 1995, and it quickly became apparent that there were severe

tensions between a requirement for risk-based pricing and a requirement to manage the

insurance funds to a specific size. Implicit constraints on the size of the FDIC’s

insurance funds placed constraints on deposit insurance pricing at the individual

institution level. The tension between the twin requirements of risk-based pricing and

management of fund size became far more explicit in 1996, when the Deposit Insurance Funds

Act constrained both the FDIC’s ability to determine which insured institutions

belong in the best category for insurance purposes, and the premiums it can charge those

institutions.

In particular, when the insurance fund is above its

Designated Reserve Ratio (1.25 percent of insured deposits at year-end 1999), the FDIC in

effect cannot collect assessment revenue from institutions in its best insurance category,

which at year-end 1999 comprised 93 percent of all insured institutions. Conversely, when

the fund is below its designated ratio, the FDIC must collect sufficient assessment

revenue to return the fund to that Designated Reserve Ratio within one year, or else

collect average deposit insurance premiums of at least 23 basis points of domestic

deposits.

The new legislative and regulatory framework has resulted

in at least three striking departures from past practice. First is the zero

deposit-insurance premium paid by most banks. In contrast to the period 1933-1995, when

the FDIC assessed every dollar of domestic deposits at a rate of at least three basis

points per annum, after 1995 most deposits were not assessed at all. A striking feature of

a zero premium is that not only may the rate paid by vastly disparate banks be identical,

but the dollar amount as well: a bank with $100 billion in deposits can be billed the same

amount for its insurance as the smallest community bank.

Second, in reaching a point where the FDIC does not

collect assessment revenue from most institutions during good times, we have clearly

departed from any concept of spreading insurance losses over time. In contrast, prior to

1989 it could be argued that Congress intended the FDIC to operate under a form of

long-term expected loss pricing. During the period 1933-1989, when premiums were set by

statute and never departed from a range of between three and 8.9 basis points per annum,

accumulated premiums and the investment income on those balances enabled the system to

roughly pay for itself. The system in place today, in contrast, amounts essentially to

charging nothing in times of prosperity and a lot in times of adversity, thereby

potentially magnifying swings in the banking cycle.

A third change stems from the conjunction of two factors:

the FDIC’s original decision to rely on examination ratings as a significant input to

the risk based premium system, and the assessment revenue constraints of the 1996 Deposit

Insurance Funds Act. The banks that were paying for deposit insurance at the end of the

1990s were those that had run afoul of capital regulations or the supervisory process.

Thus, another departure from past practice was that the pricing of deposit insurance at

the individual institution level had evolved into a penalty system for the few, rather

than a priced service for all.

|

| Issues

for Deposit Insurance Fund Management |

From the FDIC’s standpoint, it was clear as the nineties drew to a close that the

terms of the tradeoff between the ability to price deposit insurance based on risk and

constraints on aggregate revenue needed to be re-evaluated. That tradeoff had been

resolved by the Deposit Insurance Funds Act in favor of a zero premium for most

institutions. As a result, by the end of the 1990s, the moral hazard problems FDICIA

intended to address through risk-based deposit insurance premiums may have become more

firmly entrenched than ever. At year-end 1999, the FDIC provided a non-priced guarantee of

over two trillion dollars in bank liabilities.Under

pure risk-based pricing, it is likely that every bank in the U.S. with insured deposits

would pay something for its deposit insurance, for the same reason that every bank pays at

least some spread over Treasuries for unsecured debt. Given the long and uncertain

duration of banking cycles, however, under such a system it would never be clear in

advance whether the premiums accumulated during times of prosperity were more, or less,

than what would ultimately be needed during periods of economic upheaval. Consequently,

there will inevitably be questions about the appropriate disposition of these accumulated

funds. The answer to such questions depends on one’s vision of how the costs and

benefits of the deposit insurance system should be shared.

Under one extreme, deposit insurance could be

viewed as completely private. Under this pure mutual model, monies collected by the

insurer are the collective property of the banks that contributed, any insurance losses

are their sole responsibility, and pricing of deposit insurance is not the subject for

public policy discussions but is of concern only to the banking industry. The history of

banking and financial crises in both the U.S. and other countries provides numerous

examples where bank losses were so severe and so systemic that the government was forced

to step in, either through loans or taxpayer bailouts. This experience calls into question

whether pure private deposit insurance would be economically viable over long periods of

time. |

|

BIF Report

SAIF Report

|

|

Another endpoint, in

which the mutual aspect of insurance is removed completely, might be termed the user-fee

or priced service model of deposit insurance. The insurer collects premiums on an

expected-loss or risk-adjusted basis from each institution. The premium is simply a

payment for a service, namely the use of the deposit guarantee for a specified time. In

this "demutualized" model, the premium payer has neither an ownership interest

in collected premiums nor a responsibility to pay for the insurance losses of other banks.

An insurance fund to provide rapid resolution flexibility is consistent with this model,

provided government reaps all surplus funds during good times and readily recapitalizes it

to cover all insurance losses. The pure priced

service model, taken to its logical extreme, makes moot a number of issues raised in this

article. Concentrations of deposit insurance exposure – although an issue for the

government insurer and its ability to diversify risks – are not an issue for insured

institutions because they are never asked to help pay for the failures of other banks.

Rebates from the insurance funds are ruled out, but conversely banks are relieved of the

responsibility to rebuild a fund during periods of economic hardship.

|

| Whereas history casts doubt

on the long-term economic viability of a pure private deposit insurance model, it also

casts doubt on the long-term political sustainability of a pure user-fee model. It is

human nature to keep score. As assessment revenues mount far above cumulative insurance

losses during good times, bankers will point out that the

costs of the system appear to be outstripping its benefits, and they will be heard, as

they were heard in 1950 when Congress required the FDIC to institute rebates of excess

assessment revenues, and again in 1996 with the Deposit Insurance Funds Act. Conversely,

during bad times Congress is unlikely to sit by while losses mount, under the theory that

everything will even out in the end. Instead, as they have in the past, the banking

industry probably would be asked to pay for as significant a share of losses as possible

before recourse is had to the taxpayer. |

| Between the two

endpoints of a purely private system and a pure user fee system – between a pure

mutual system and a completely demutualized one – are the intermediate models of

mutual insurance with a federal backstop against catastrophic loss. Under these

approaches, banks are mutually obligated to pay aggregate insurance losses up to a point,

and mutually entitled to some of the benefits of favorable fund performance. Under any

such approach, the federal government’s guarantee against catastrophic loss gives it

a significant public policy stake in ensuring that the guarantee is appropriately priced.

At the same time, all participants in the system have a significant stake in the manner in

which aggregate system performance results in shared costs and shared benefits. For example, under the current system, banks are mutually

obligated to recapitalize the insurance funds if the funds fall below a designated ratio;

conversely, when the funds remain above the designated ratio they are mutually entitled to

a benefit, namely zero-cost federal deposit insurance for most institutions. This

particular set of mutual obligations and benefits carries with it all of the issues we

described: the zero premium during good times; a |

|

|

| potentially

heavy assessment during bad times; and a growing concentration of contingent deposit

insurance exposures. Current arrangements also create an issue we have so far deferred:

the tendency of a zero premium under a mutual insurance arrangement to create free-rider

problems, in which new banks, fast growing banks and non-banks can, at no cost to

themselves, increase the mutually shared obligations or reduce the mutually shared

benefits of other members of the system. There may be other quasi-mutual models where the rules for doling

out mutual costs and benefits are different than in our current system, and that do not

create the degree of perverse or unintended consequences as our current system. For

example, it is not clear that the shared benefit that accrues to the banking industry

during good times should necessarily be in the form of a zero deposit insurance premium.

One could imagine, for example, that premiums collected during good times could go first

to the insurance fund, and then to some asset in which member banks have a collective or

individual interest. There are many ways banks’ collective interest in such an asset

could be structured – through a rebate system, through a credit-union approach in

which each bank carries its share of the asset on its books, or some other approach in

which the collective asset only generates cash flows for banks during bad times. Under any

of these approaches, if ownership of the collective asset were apportioned analogous to a

mutual fund, with a dollar of premiums buying a dollar of shares, the free-rider problems

described above could be mitigated.

|

| Implications

for Deposit Insurance Pricing |

Risk-based deposit insurance pricing at the

individual institution level has two goals: to provide beneficial incentives to control

excessive risk taking and mitigate the moral hazard problems associated with flat-rate

deposit insurance; and to lessen the degree to which strong institutions subsidize weak

and poorly managed institutions, so that the cost of the insurance program is shared in an

equitable manner.

An interesting question is whether deposit insurance

pricing is conceptually redundant with supervision as a policy instrument to accomplish

these goals. There are reasons to think not. There are built-in limits in a market economy

on the degree that supervisors can or should attempt to control individual institution

behavior. To use a private insurance analogy, a supervisor is unlikely to take away

someone’s driver’s license simply because that person owns a sports car; an

insurer, without trying to change the behavior, can price it. Even under a theoretically

perfect supervisory capital regime where all institutions have an identical estimated

probability of failure, market pricing or other indicators may at times suggest that the

risk profiles of some institutions are significantly different than others. In such

instances deposit insurance pricing can be a policy tool that complements the tools

available to supervisors.

In practice, there are limits to what deposit insurance

pricing can and should try to achieve. The FDIC provides a monopoly-priced service, and it

may be undesirable for a federal agency to make exceedingly fine subjective distinctions

that have the effect of allocating credit to favored activities or institutions. Within

those limits, however, risk differentiation is important, and the technical issues of how

best to achieve it are significant.

PDF version of chart (39Kb PDF file - PDF help or hard copy)

|

|

If a significant adverse change in the banking and economic cycle

occurs in the next few years, historical experience suggests that many of the resulting

bank failures will come from institutions that did not pay insurance premiums at year-end

1999. The question will then be how many of those premium misclassifications were the

result of what one might call random errors – the price we willingly accepted for not

having an overly burdensome regulatory and supervisory structure – and how many were

the result of systematically subsidizing certain types of riskier institutions at the

expense of other members of the system. |

| When we consider the more than 9,500 insured

institutions that all paid no premium at year-end 1999, there clearly were some systematic

factors that distinguished their risk profiles. The distinction between banks with

composite examination ratings of 1 and 2 is one example, but there may be others. For

example, should new banks or fast growing banks pay additional premiums, both for reasons of risk differentiation and to force

them to pay for the external cost they impose on other members in a mutual structure? Are

there indicators that would identify those banks within the best risk-related premium

category that have high concentrations of risky assets, significant interest-rate risk or

market risk, or weak risk-management practices? The best risk indicators may not be the same for large

institutions as for small institutions, and indeed, both onsite and offsite examination

procedures vary depending on the size, complexity and risk profile of a bank. FDICIA

provided the FDIC with authority to establish separate premium systems for large versus

small institutions. Because of their size, scope and complexity, large institutions and

their supervisors necessarily measure and manage risk differently than is the case for a

typical small bank. By the end of the nineties it was clear that some thought needed to be

given to the implications of the developments in large-bank risk measurement for the way

the FDIC measures risk for insurance purposes, so that the FDIC might benefit from the

results of risk measurement undertaken by industry practitioners, as well as by their

supervisors and publicly available sources. Likewise, risks taken by large banks are

priced in a variety of markets, conceivably resulting in useful information that may be

valuable in pricing deposit insurance. And the proliferation of financial instruments by

which risks are transferred and priced is at least suggestive of the possibility that new

instruments could be developed that could enhance risk-based pricing at the individual

institution level, or provide market signals about the direction of the FDIC’s

aggregate exposure.

Given the potential for a bank’s risk profile

to change quickly, changes in risk profiles in the interval between examinations may take

on added significance in the years ahead. The FDIC already has a number of offsite tools

for evaluating these inter-examination trends, and the importance of continuing to refine

such tools and develop new ones is likely to increase.

Finally, if risks are indeed becoming more opaque and

complex to monitor as we have argued, there is room for discussion of the implications for

deposit insurance pricing. An interesting public policy question is what role, if any,

deposit insurance premiums should have in providing incentives to banks regarding the

quality of their disclosures about the risks they undertake.

|

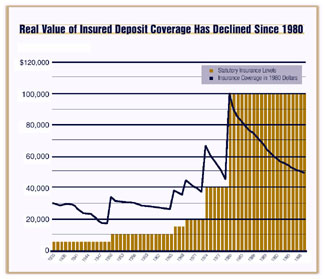

| Insurance Coverage |

There has been considerable discussion since

year-end 1999 about whether and how deposit insurance coverage should be adjusted for

inflation. The merits of indexing coverage ultimately depend on one’s view of the

role of deposit insurance in the financial system. Deposit insurance was implemented not

only to protect small savers, but to correct a market failure: the susceptibility of banks

to deposit runs, a susceptibility that arises from banks’ combination of illiquid

assets and liquid liabilities.

There was always a danger that deposit insurance would

simply replace one ill with another. While deposit runs are a thing of the past, in their

place we have a greater potential for the distortions and moral hazard problems that come

with a federal safety net. For those who do not think this has been a good tradeoff, the

policy prescription is clear: allow the deposit insurance coverage limit to erode in real

terms over time.

On the other side of the debate are those who point to

the array of private sector and supervisory risk mitigation tools, and more recently,

risk-based premiums, that can act as a counterweight to the potential moral hazard

problems. In this view, the increased stability deposit insurance brings is not completely

offset by other problems. There is also the view that every country has deposit insurance

– whether it knows it or not – and that meaningful, explicit coverage results in

lower costs in the event of banking crises than would occur under negligible or implicit

coverage. The argument is that little or no formal coverage may well turn into unlimited

coverage in times of crisis, while a meaningful and explicit coverage limit is more likely

to be adhered to. Proponents of this view would be more likely to recommend a coverage

limit that adjusts over time to maintain the same relative importance in the financial

system.

* * *

None of the issues discussed in this article are easy to

address, but their importance is undeniable. The time appears ripe for a productive debate

on how the U.S. deposit insurance system should be strengthened to meet the new

challenges.

|