I. Management's Discussion and Analysis

The Year in Review

Overview

Much of our work during 2012 focused on a number of key areas, all mission-based. First was moving forward on implementing our new responsibilities under the Dodd-Frank Act. This effort included continuing implementation of FDIC’s systemic resolution responsibilities under the Dodd-Frank Act, including resolution planning and promoting cross border cooperation and cooperation with respect to any orderly resolution of a globally active, systemically important financial institution. We commenced a Community Banking Initiative to further the understanding of the future of community banking, which included outreach, research, and efforts to streamline examinations without compromising safe and sound banking practices. As always, our mission to maintain stability and public confidence in the nation’s financial system guided our work. The sections below fill in the details and highlight some of our accomplishments during the year.

Insurance

The FDIC insures bank and savings association deposits. As insurer, the FDIC must continually evaluate and effectively manage how changes in the economy, the financial markets, and the banking system, affect the adequacy and the viability of the Deposit Insurance Fund (DIF).

Long-Term Comprehensive Fund Management Plan

In 2010 and 2011, the FDIC developed a comprehensive, long-term management plan designed to reduce the effects of cyclicality and achieve moderate, steady assessment rates throughout economic and credit cycles, while also maintaining a positive fund balance even during a banking crisis. The plan is designed to ensure that the reserve ratio will reach 1.35 percent by September 30, 2020, as required by the Dodd-Frank Act.1 The plan includes a reduction in rates that the FDIC Board has adopted to become effective once the reserve ratio reaches 1.15 percent. To increase the probability that the fund reserve ratio will reach a level sufficient to withstand a future crisis, the FDIC Board has—pursuant to the plan—suspended dividends indefinitely. The plan prescribes progressively lower assessment rates that will become effective when the reserve ratio exceeds 2.0 percent and 2.5 percent. These lower assessment rates serve almost the same function as dividends, but provide more stable and predictable effective assessment rates.

Under provisions in the Federal Deposit Insurance Act that require the FDIC Board to set the Designated Reserve Ratio (DRR) for the DIF annually, the FDIC Board voted in December 2012 to maintain the 2.0 percent DRR for 2013. Using historical fund loss and simulated income data from 1950 to 2010, FDIC analysis showed the reserve ratio would have had to exceed 2.0 percent before the onset of the two crises that occurred since the late 1980s, to have maintained both a positive fund balance and stable assessment rates throughout both crises. The analysis assumes a moderate, long-term average industry assessment rate, consistent with the rates set forth in the plan. The 2.0 percent DRR should not be viewed as a cap on the fund. The FDIC views the 2.0 percent DRR as a long-term goal and the minimum level needed to withstand future crises of the magnitude of past crises.

State of the Deposit Insurance Fund

Estimated losses to the DIF were $2.7 billion from failures occurring in 2012, and were lower than losses from failures in each of the previous four years. The fund balance continued to grow through the fourth quarter of 2012, with 12 consecutive quarters of positive growth. Assessment revenue, fewer anticipated bank failures, and the transfer of fees previously set aside for debt guaranteed under the Temporary Liquidity Guarantee Program (TLGP) have driven the increase in the fund balance. The fund reserve ratio rose to 0.35 percent at September 30, 2012, from 0.17 percent at the beginning of the year.

Assessment System for Large and Highly Complex Institutions

On October 9, 2012, the FDIC Board approved a final rule to amend the assessment system for large and highly complex institutions. The rule amends definitions adopted in the February 2011 large bank pricing rule used to identify concentrations in higher-risk assets. This rule, which went into effect on April 1, 2013, amends the definitions of leveraged loans and subprime loans, which are areas of significant potential risk. The revised definition of leveraged loans, renamed higher-risk C&I (commercial and industrial) loans and securities, focuses on large loans to the riskiest borrowers—those that are highly leveraged as the result of loans to finance a buyout, acquisition, or capital distribution. The revised definition of subprime consumer loans, renamed higher-risk consumer loans, focuses on the most important characteristic—the probability of default. The final rule resulted from concerns raised by the industry about the cost and burden of reporting under the definitions in the February 2011 rule. Nonetheless, the new definitions better reflect the risk that institutions pose to the DIF.

Temporary Liquidity Guarantee Program

On October 14, 2008, as part of a coordinated response by the U.S. government to the disruption in the financial system and the collapse of credit markets, the FDIC implemented the Temporary Liquidity Guarantee Program (TLGP). By calming market fears and encouraging lending, the TLGP helped bring stability to financial markets and the banking industry during the crisis period. The TLGP consisted of two components: (1) the Transaction Account Guarantee Program (TAG), an FDIC guarantee in full of non interest-bearing transaction accounts; and (2) the Debt Guarantee Program (DGP), an FDIC guarantee of certain newly issued senior unsecured debt.

The TAG Program initially guaranteed in full all domestic non interest-bearing transaction deposits held at participating banks and thrifts through December 31, 2009. The deadline was extended twice and expired on December 31, 2010.

The TAG Program brought stability and confidence to banks and their business customers by removing the risk of loss from deposit accounts that are commonly used to meet payroll and other business transaction purposes. Deposits provide the primary source of funding for most banks, and they are particularly important for smaller institutions. The temporary coverage allowed institutions, particularly smaller ones, to retain these accounts and maintain the ability to make loans within their communities.

Under the DGP, the FDIC initially guaranteed in full, through maturity or June 30, 2012, whichever came first, the senior unsecured debt issued by a participating entity between October 14, 2008, and June 30, 2009. In 2009, the issuance period was extended through October 31, 2009. The FDIC’s guarantee on each debt instrument was also extended in 2009 to the earlier of the stated maturity date of the debt or December 31, 2012.

The DGP enabled financial institutions to meet their financing needs during a period of record high credit spreads and aided the successful return of the credit market to near normalcy, despite the recession and slow economic recovery. This improvement in the credit markets was reflected in the increasing ability of banks and their holding companies to issue longer-term debt over the course of the DGP issuance period. At the inception of the program, firms heavily relied upon the DGP to roll over short-term liabilities because of the fragility of the credit markets and investors’ continued aversion to risk. By providing the ability to issue debt guaranteed by the FDIC, the DGP allowed institutions to extend maturities and obtain more stable unsecured funding.

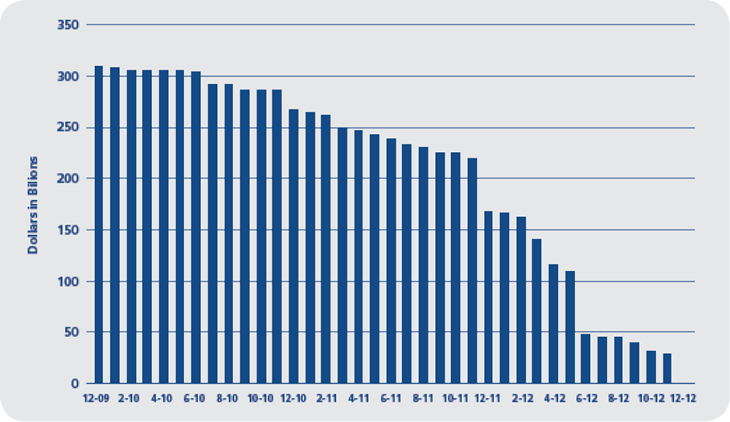

Outstanding TLGP Debt by Month

Program Statistics

Over the course of the DGP’s existence, 122 entities issued TLGP debt. At its peak, the DGP guaranteed $345.8 billion of debt outstanding (see the chart above). The DGP guarantee on all TLGP debt that had not already matured, expired on December 31, 2012. Therefore, at the end of 2012, no debt guaranteed by the DGP remained.

The FDIC collected $10.4 billion in fees and surcharges under the DGP. As of December 31, 2012, the FDIC paid $153 million in losses resulting from six participating entities defaulting on debt issued under the DGP. The majority of these losses ($113 million) arose from banks

with outstanding DGP notes that failed in 2011 and were placed into receivership.

The FDIC collected $1.2 billion in fees under the TAG Program. Cumulative estimated TAG Program losses on failures as of December 31, 2012, totaled $2.1 billion.

Overall, TLGP fees exceeded the losses from the program. From inception of the TLGP, it was the FDIC’s policy to recognize revenue to the DIF for any deferred revenue not absorbed by losses upon expiration of the TLGP guarantee period (December 31, 2012) or earlier, for any portion of guarantee fees determined in excess of amounts needed to cover potential losses. In total, $9.3 billion in TLGP fees and surcharges were deposited into the DIF.

Temporary Unlimited Coverage for Non interest-Bearing Transaction Accounts under the Dodd-Frank Act Ends

The Dodd-Frank Act provided temporary unlimited deposit insurance coverage for non interest-bearing transaction accounts from December 31, 2010, through December 31, 2012, regardless of the balance in the account and the ownership capacity of the funds. This coverage essentially replaced the TAG Program, which expired on December 31, 2010, and was available to all depositors, including consumers, businesses, and government entities. The coverage was separate from, and in addition to, the standard insurance coverage provided for a depositor’s other accounts held at an FDIC-insured bank.

A non interest-bearing transaction account is a deposit account in which interest is neither accrued nor paid, depositors are permitted to make transfers and withdrawals, and the bank does not reserve the right to require advance notice of an intended withdrawal.

Similar to the TAG Program, the temporary unlimited coverage also included trust accounts established by an attorney or law firm on behalf of clients, commonly known as IOLTAs, or functionally equivalent accounts. Money market deposit accounts and negotiable order of withdrawal accounts were not eligible for this temporary unlimited insurance coverage, regardless of the interest rate and even if no interest was paid.

As of September 30, 2012, insured institutions had $1.5 trillion above the basic coverage limit of $250,000 per account in domestic non interest-bearing transaction accounts. This amount was fully insured through the end of 2012 under the Dodd-Frank Act.

The provision of the Dodd-Frank Act extending unlimited FDIC coverage to non interest-bearing transaction accounts through 2012, like the original TAG Program, served as a source of stability to both banks and their business customers in the wake of the financial crisis and economic downturn.

1 The Act also requires that the FDIC offset the effect on institutions with less than $10 billion in assets of increasing the reserve

ratio from 1.15 percent to 1.35 percent. The FDIC will promulgate a rulemaking that implements this requirement at a later

date to better take into account prevailing industry conditions at the time of the offset. |