|

| 2011 Annual Report

|

| Previous | Contents | Next |

I. Management's Discussion and Analysis

The Year in Review

During 2011, the FDIC continued to pursue an ambitious agenda in meeting its responsibilities. The FDIC continued implementation of Dodd-Frank, issued guidance, and piloted programs designed to help consumers. The FDIC also enhanced risk management procedures and created a branch to manage risks of mid tier insured depository institutions (IDIs), which further strengthened supervisory and consumer protection programs.

Highlighted in this section are the FDIC’s 2011 accomplishments in each of its major business lines—Insurance, Supervision, Consumer Protection, and Receivership Management—as well as its program support areas.

Insurance

The FDIC insures bank and savings association deposits. As insurer, the FDIC must continually evaluate and effectively manage how changes in the economy, the financial markets, and the banking system affect the adequacy and the viability of the Deposit Insurance Fund (DIF).

State of the Deposit Insurance Fund

Estimated losses to the DIF were $7.9 billion from failures occurring in 2011 and were lower than losses from failures in each of the previous three years. The fund balance became positive in the second quarter of 2011 following seven quarters of negative balances. Assessment revenue and fewer anticipated bank failures drove the increase in the fund balance. The fund reserve ratio rose to positive 0.17 percent at December 31, 2011 from negative 0.12 percent at the beginning of the year.

Long-Term Comprehensive Fund

Management Plan

As a result of the Dodd-Frank Act revisions to its fund management authority, the FDIC developed a comprehensive, long-term management plan for the DIF designed to reduce pro-cyclicality and achieve moderate, steady assessment rates throughout economic and credit cycles while also maintaining a positive fund balance even during a banking crisis. The plan was finalized in rulemakings adopted in December 2010 and February 2011.

Setting the Designated Reserve Ratio

Using historical fund loss and simulated income data from 1950 to the present, the FDIC analyzed how high the reserve ratio would have had to have been before the onset of the two crises that occurred since the late 1980s to have maintained both a positive fund balance and stable assessment rates throughout the period. The analysis concluded that a moderate, long-term average industry assessment rate would have been sufficient to have prevented the fund from becoming negative during the crises, though the fund reserve ratio would have had to exceed 2.0 percent before the onset of the crises.

Therefore, under provisions in the Federal Deposit Insurance Act that require the FDIC Board to set the Designated Reserve Ratio (DRR) for the DIF annually, the FDIC Board adopted in December 2010 a DRR of 2.0 percent for 2011 and voted in December 2011 to maintain a 2.0 percent DRR for 2012. The FDIC views the 2.0 percent DRR as a long-term goal and as the minimum level needed to withstand future crises of the magnitude of past crises. The 2.0 percent DRR should not be viewed as a cap on the fund. The FDIC’s analysis shows that a reserve ratio higher than 2.0 percent would increase the chance that the fund will remain positive during a future economic and banking downturn similar to or more severe than past crises.

Long-Term Assessment Rate Schedules and

Dividend Policies

Once the reserve ratio reaches 1.15 percent, assessment rates can be reduced to a moderate level. Therefore, under its statutory authority to set assessments, in February 2011, the FDIC Board adopted a lower assessment rate schedule to take effect when the fund reserve ratio exceeds 1.15 percent. To increase the probability that the fund reserve ratio will reach a level sufficient to withstand a future crisis, the FDIC also suspended dividends indefinitely when the fund reserve ratio exceeds 1.5 percent. In lieu of dividends, the FDIC Board adopted progressively lower assessment rate schedules when the reserve ratio exceeds 2.0 percent and 2.5 percent. These lower assessment rate schedules serve much the same function as dividends, but provide more stable and predictable effective assessment rates.

Restoration Plan

In October 2010, under the comprehensive plan, the FDIC adopted a Restoration Plan to ensure that the reserve ratio reaches 1.35 percent by September 30, 2020, as required by the Dodd-Frank Act. The Act also requires that the FDIC offset the effect on institutions with less than $10 billion in assets of increasing the reserve ratio from 1.15 percent to 1.35 percent. The FDIC will promulgate a rulemaking that implements this requirement at a later date to better take into account prevailing industry conditions at the time of the offset.

Change in the Deposit Insurance Assessment Rules

The Dodd-Frank Act also required the FDIC to adopt a rule revising the deposit insurance assessment base. The final rule implementing the requirement, adopted in February 2011, also made conforming changes to the deposit insurance assessment system. In addition, the rule substantially revised the assessment system applicable to large IDIs.

New Assessment Base

Dodd-Frank requires the FDIC to amend its regulations to define the assessment base as average consolidated total assets minus average tangible equity, rather than total domestic deposits (which, with minor adjustments, it has been since 1935). The Act allows the FDIC to modify the assessment base for banker’s banks and custodial banks. The FDIC finalized these changes to the assessment base in February 2011, and they became effective April 1, 2011.

Dodd-Frank also requires that, for at least five years, the FDIC must make available to the public the reserve ratio and the DRR using both estimated insured deposits and the new assessment base. As of December 31, 2011, the FDIC estimates that the reserve ratio would have been 0.10 percent using the new assessment base (compared to 0.17 percent using estimated insured deposits) and that the 2.0 percent DRR using estimated insured deposits would have been 1.2 percent using the new assessment base.

Conforming Changes to Risk-Based Premium

Rate Adjustments

The changes to the assessment base necessitated changes to existing risk-based assessment rate adjustments. The previous assessment rate schedule incorporated adjustments for types of funding that either pose heightened risk to the DIF or that help to offset risk to the DIF. Because the magnitude of these adjustments and the cap on the adjustments had been calibrated to a domestic deposit assessment base, the rule changing the assessment base also recalibrated the unsecured debt and brokered deposit adjustments. Since secured liabilities are now included in the assessment base, the rule eliminated the secured liability adjustment.

The assessment rate of an institution is also adjusted upwards if it holds unsecured debt issued by other IDIs. The issuance of unsecured debt by an IDI usually lessens the potential loss to the DIF if an institution fails; however, when the debt is held by other IDIs, the overall risk in the system is not reduced.

Conforming Changes to Assessment Rates

The new assessment base under Dodd-Frank, defined as average consolidated total assets minus average tangible equity, is larger than the previous assessment base, defined as total domestic deposits (with minor adjustments). Applying the current rate schedule to the new assessment base would have resulted in larger total assessments than had been previously collected. Accordingly, the rule changing the assessment base also established new rates that took effect in the second quarter of 2011. These rates resulted in collecting nearly the same amount of assessment revenue under the new base as under the previous rate schedule using the domestic deposit base. The new rate schedule also incorporates the changes from the proposed large bank pricing rule that was finalized in February 2011 (discussed below) along with the change in the assessment base. The initial base rates for all institutions range from 5 to 35 basis points.

The initial base assessment rates, range of possible

rate adjustments, and minimum and maximum

total base rates are shown in the table below.

Changes to the assessment base, assessment

rate adjustments, and assessment rates took

effect April 1, 2011. As explained above, the rate

schedule will decrease when the reserve ratio

reaches 1.15, 2.0, and 2.5 percent.

Current Initial and Total Base Assessment Rates¹

|

Risk

Category I |

Risk

Category II |

Risk

Category III |

Risk

Category IV |

Large and Highly

Complex Institutions |

Initial base

assessment rate |

5–9 |

14 |

23 |

35 |

5-35 |

Unsecured debt

adjustment² |

(4.5)–0 |

(5)–0 |

(5)–0 |

(5)–0 |

(5)–0 |

Brokered deposit

adjustment |

…… |

0–10 |

0–10 |

0–10 |

0–10 |

Total Base

Assessment Rate |

2.5–9 |

9–24 |

18–33 |

30-45 |

2.5–45 |

|

Changes to the Large Bank Assessment System

The FDIC continued its efforts to improve risk differentiation and reduce pro-cyclicality in the deposit insurance assessment system by issuing a final rule in February 2011. The rule revises the assessment system applicable to large IDIs to better reflect risk at the time a large institution assumes the risk, to better differentiate large institutions during periods of good economic conditions, and to better take into account the losses that the FDIC may incur if such an institution fails. The rule became effective April 1, 2011.

The rule eliminates risk categories for large institutions. As required by Dodd-Frank, the FDIC no longer uses long-term debt issuer ratings to calculate assessment rates for large institutions. The rule combines CAMELS¹ ratings and financial measures into two scorecards—one for most large institutions and another for the remaining very large institutions that are structurally and operationally complex or that pose unique challenges and risks in case of failure (highly complex institutions). In general, a highly complex institution is an institution (other than a credit card bank) with more than $50 billion in total assets that is controlled by a parent or intermediate parent company with more than $500 billion in total assets, or a processing bank or trust company with at least $10 billion in total assets.

Both scorecards use quantitative measures that are readily available and useful in predicting an institution’s long-term performance to produce two scores—a performance score and a loss severity score—that are combined into a total score and converted to an initial assessment rate. The performance score measures an institution’s financial performance and its ability to withstand stress. The loss severity score quantifies the relative magnitude of potential losses to the FDIC in the event of the institution’s failure.

The rule also authorizes the FDIC to adjust an institution’s total score by as much as 15 points, up or down. The FDIC proposed in April 2011 and adopted in September 2011 guidelines that describe the process the FDIC follows to determine whether to make an adjustment, to determine the size of any adjustment, and to notify an institution of an adjustment and how large it will be.

|

Effect of Implementing Changes to Assessment Base, Assessment Rates, and Large Bank Assessment System

Consistent with the intent of Congress, the change to the assessment base resulted in an increase in the share of overall assessments paid by large institutions, which rely less on domestic deposits for their funding than do smaller banks. For the second quarter of 2011, when the changes to the assessment base and other assessment system changes described above became effective, banks with more than $10 billion in assets accounted for approximately 80 percent of assessments, up from 70 percent in the first quarter and commensurate with the increase in their share of the assessment base. Second quarter assessments for banks with less than $10 billion in assets were 33 percent lower in aggregate than first quarter assessments.

Temporary Liquidity Guarantee Program

On October 14, 2008, the FDIC announced and implemented the Temporary Liquidity Guarantee Program (TLGP). The TLGP consisted of two components: (1) the Transaction Account Guarantee Program (TAGP), an FDIC guarantee in full of noninterest-bearing transaction accounts; and (2) the Debt Guarantee Program (DGP), an FDIC guarantee of certain newly issued senior unsecured debt.

The TAGP initially guaranteed in full all domestic noninterest-bearing transaction deposits held at participating banks and thrifts through December 31, 2009. The deadline was extended twice and expired on December 31, 2010.

Under the DGP, the FDIC initially guaranteed in full, through maturity or June 30, 2012, whichever came first, the senior unsecured debt issued by a participating entity between October 14, 2008, and June 30, 2009. In 2009 the issuance period was extended through October 31, 2009. The FDIC’s guarantee on each debt instrument also was extended in 2009 to the earlier of the stated maturity date of the debt or December 31, 2012.

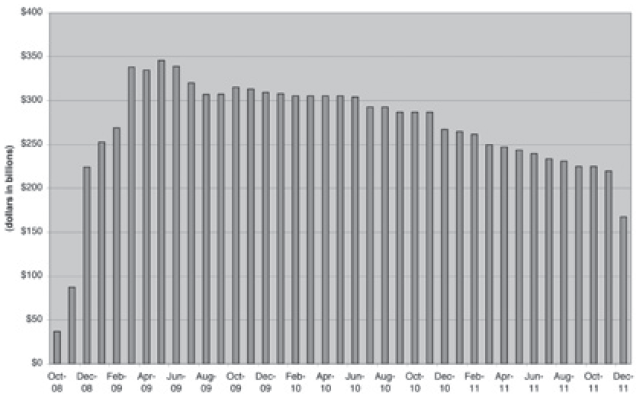

Program Statistics

Over the course of the DGP’s existence, 122 entities issued TLGP debt. At its peak, the DGP guaranteed almost $345.8 billion of debt outstanding (see chart below). As of December 31, 2011, the total amount of remaining FDIC-guaranteed debt outstanding was $167.4 billion.

The FDIC collected $10.4 billion in fees and surcharges under the DGP. As of December 31, 2011, the FDIC paid or accrued $152 million in estimated losses resulting from six participating entities defaulting on debt issued under the DGP. The majority of these estimated losses ($112 million) arose from banks with outstanding DGP notes that failed in 2011 and were placed into receivership. The FDIC expects to pay an additional $682 thousand in interest payments on defaulting notes in 2012.

The FDIC collected $1.2 billion in fees under the TAGP. Cumulative estimated TAGP losses on failures as of December 31, 2011, totaled $2.2 billion.

Overall, TLGP fees are expected to exceed the losses from the program. From inception of the TLGP, it has been FDIC’s policy to recognize revenue to the DIF for any deferred revenue not absorbed by losses upon expiration of the TLGP guarantee period (December 31, 2012) or earlier for any portion of guarantee fees determined in excess of amounts needed to cover potential losses. As of December 31, 2011, $2.6 billion in TLGP assets were transferred to the DIF. If fees are insufficient to cover the costs of the program, the difference will be made up through a systemic risk special assessment.

| OUTSTANDING TLGP DEBT BY MONTH |

|

|

Temporary Unlimited Coverage for

Noninterest-Bearing Transaction Accounts

Under the Dodd-Frank Act

Dodd-Frank provides temporary unlimited deposit insurance coverage for noninterest-bearing transaction accounts from December 31, 2010, through December 31, 2012, regardless of the balance in the account and the ownership capacity of the funds. This coverage essentially replaced the TAGP, which expired on December 31, 2010, and is available to all depositors, including consumers, businesses, and government entities. The coverage is separate from, and in addition to, the standard insurance coverage provided for a depositor’s other accounts held at an FDIC-insured bank.

A noninterest-bearing transaction account is a deposit account in which interest is neither accrued nor paid, depositors are permitted to make transfers and withdrawals, and the bank does not reserve the right to require advance notice of an intended withdrawal.

Similar to the TAGP, the temporary unlimited coverage also includes trust accounts established by an attorney or law firm on behalf of clients, commonly known as IOLTAs, or functionally equivalent accounts. Money market deposit accounts (MMDAs) and NOW accounts are not eligible for this temporary unlimited insurance coverage, regardless of the interest rate and even if no interest is paid.

As of December 31, 2011, insured institutions had $1.4 trillion in domestic noninterest-bearing transaction accounts above the basic coverage limit of $250,000 per account. This amount is fully insured until the end of 2012 under Dodd-Frank.

Large Bank Programs

The FDIC’s responsibilities for IDIs include deposit insurance, primary supervision of state nonmember (FDIC-supervised) IDIs, back-up supervision of non-FDIC-supervised IDIs, and resolution planning. For large IDIs, these responsibilities often present unique and complex challenges. The FDIC’s ability to analyze and respond to risks in these institutions is of particular importance, as they make up a significant share of the banking industry’s assets. The Large Bank Program’s objectives are achieved through two primary centralized groups that work extensively with the FDIC and the other bank and thrift regulators.

Office of Complex Financial Institutions

The Office of Complex Financial Institutions (OCFI) was created in 2010 to focus on the expanded responsibilities of the FDIC by Dodd-Frank. The OCFI is responsible for oversight and monitoring of large, systemically important financial institutions (SIFIs) and for resolution strategy development and planning. During 2011, OCFI began to carry out its new statutory responsibilities to monitor risks in these large SIFIs, conduct resolution planning to respond to potential crisis situations, and coordinate with foreign regulators on significant cross-border resolution issues.

In 2011, OCFI established its complex financial institution monitoring program and engaged in continuous review, analysis, examination and assessment of key risks and control issues at institutions with assets over $100 billion. This work is being accomplished both off- and on-site at designated complex financial institutions throughout the United States. The FDIC is working with other federal regulators to analyze and gain a solid understanding of the risk measurement and management practices of these institutions and assessing the potential risks these companies pose to financial stability. In addition, off-site financial analysts complete the monitoring function by providing subject matter expertise in analyzing complex financial institution’s key business lines and potential critical areas of risk. These efforts ensure that the FDIC has established advance in-depth institutional knowledge required to identify and evaluate risks in financial institutions that are designated as systemically important.

Substantial progress has been made in developing resolution planning and implementation capabilities within OCFI to meet the expanded responsibilities and authorities under Dodd-Frank, including completing regulations governing these responsibilities. In July 2011, the FDIC approved a final rule implementing the Orderly Liquidation Authority that provides the authority to resolve SIFIs. During 2011 OCFI established its internal frameworks for SIFI resolution under Title II of Dodd-Frank, and began developing the capabilities necessary to implement such resolutions. Additionally, OCFI revised and built out specific resolution plans for the largest domestic SIFIs. In 2011, the FDIC adopted two rules regarding resolution plans (living wills) that covered financial institutions will be required to prepare. The first rule, which implements requirements of the Dodd-Frank Act, became final and was published jointly with the Federal Reserve Board in the Federal Register on November 1, 2011, and was effective on November 30, 2011. It requires bank holding companies with total consolidated assets of $50 billion or more and certain nonbank financial companies designated by the Financial Stability Oversight Council for supervision by the Federal Reserve Board to develop, maintain, and periodically submit plans for their rapid and orderly resolution under the Bankruptcy Code, in the event they experience material financial distress. Under the rule, covered companies with nonbank U.S. assets greater than $250 billion are required to submit initial plans by July 1, 2012. A second rule, (issued as an Interim Final Rule on September 14, 2011, and adopted in final form on January 17, 2012) requires IDIs with assets greater than $50 billion to submit plans for resolution under the Federal Deposit Insurance Act. OCFI, working in partnership with the Federal Reserve, has been developing structure and guidance for the initial Dodd-Frank rule submissions, so that these submissions may be more effectively evaluated for completeness and compliance with rule requirements. The overall focus will be on the covered company’s strategy for orderly resolution, including an assessment of its resolvability and its analysis of potential impediments to implementing a resolution in an orderly manner.

Also in 2011, OCFI commenced activities to manage its global outreach, communication and coordination with appropriate domestic and foreign financial supervisory, regulatory and resolution authorities and representatives of financial institutions for the purpose of planning and executing the resolution of globally active SIFIs. The International Coordination Group of OCFI maintains close, collaborative relations with key international stakeholders to facilitate effective domestic and global cooperation on matters relating to cross-border resolution for all covered institutions. OCFI actively participates in the Financial Stability Board’s (FSB) Cross-Border Crisis Management Working Groups and supports related policy development initiatives by the FSB’s Resolution Steering Group.

Mid Tier Bank Branch

The FDIC established a Mid Tier Bank Branch (MTB) within its Division of Risk Management and Supervision in January 2011. MTB is responsible for monitoring the risk management supervision of IDIs with total assets of $10 billion to $100 billion. For large FDIC-supervised institutions, the supervision programs are staffed and administered at the regional office level. MTB provides oversight and examination and analytical support to ensure consistency in FDIC’s large bank supervisory programs. MTB examination specialists also provide examination support when the FDIC exercises its backup authority at these large institutions. MTB is also responsible for managing nationwide risk management programs including the Large Insured Depository Institution (LIDI) Program, the interagency Shared National Credit Program, and certain initiatives established under the Dodd-Frank Act such as resolution planning for banking companies with total assets from $50 billion to $100 billion.

The LIDI Program remains the primary instrument for off-site monitoring of IDIs with $10 billion or more in total assets. The LIDI Program provides a comprehensive process to standardize data capture and reporting through nationwide quantitative and qualitative risk analysis of large and complex institutions. The LIDI Program was refined in 2011 to better quantify risk, to provide a more prospective assessment of large institutions’ vulnerability to both asset and funding stress, and to more closely align with the large bank deposit insurance pricing program. The comprehensive LIDI Program is essential to effective large bank supervision by capturing information on risks, determining the need for supervisory action, and supporting large bank insurance assessment decisions and resolution planning efforts. As of December 31, 2011, the LIDI Program encompassed 112 institutions with total assets of $11.0 trillion.

Center for Financial Research

The Center for Financial Research (CFR) is responsible for encouraging and supporting innovative research on topics that are important to the FDIC’s role as deposit insurer and bank supervisor. During 2011, the CFR co-sponsored two major conferences.

The CFR organized and sponsored the 21st Annual Derivatives Securities and Risk Management Conference jointly with Cornell University’s Johnson Graduate School of Management and the University of Houston’s Bauer College of Business. The conference was held in March 2011 at the Seidman Center and attracted over 100 researchers from around the world. Conference presentations were on topics including options markets, derivatives pricing, fixed income markets, volatility risk premiums, sovereign risk and commodity markets.

The CFR also organized and sponsored the 11th Annual Bank Research Conference jointly with The Journal for Financial Services Research (JFSR) in September 2011. The conference theme, Lessons from the Crisis, focused on the recent financial crisis included 13 paper presentations and was attended by over 120 participants. Experts discussed a range of topics including government support and bank behavior, measuring risk, bank performance and lending, and CEO compensation.

In addition to conferences, workshops and symposia, eight CFR working papers were completed and made public on topics including global retail lending, foreclosure trends, systemic risk, and the use of credit default swaps.

International Outreach

Throughout 2011, the FDIC played a leading role among international standard-setting, regulatory, supervisory, and multi-lateral organizations by contributing to the development of policies with respect to reducing the moral hazard and other risks posed by SIFIs. Among the institutions the FDIC collaborated with, were the Basel Committee on Banking Supervision (BCBS), the FSB, and the International Association of Deposit Insurers (IADI).

Key to the international collaboration was the ongoing dialogue among the FDIC Chairman, Acting Chairman, other senior FDIC leaders and a number of senior financial regulators from the United Kingdom (UK) about the implementation of Dodd-Frank, Basel III, compensation policies, and how changes in the US financial regulations compare to regulatory developments in the UK and Europe. In light of the large cross-border operations, the primary areas of discussion and collaboration were development of recovery and resolution plans for SIFIs, the FDIC’s plans for executing a SIFI resolution, and the importance of cross-border coordination in the event a SIFI becomes distressed.

The FDIC participated in Governors and Heads of Supervision and BCBS meetings and the supporting work streams, task forces, and Policy Development Group meetings to address the BCBS’s work to calibrate and finalize the implementation of Basel III, monitor the new leverage ratio and liquidity standards, and complete work on the treatment of counterparty credit risk and determination of surcharges on globally systemically important banks (G-SIBs). In addition to Basel III capital and liquidity reforms, the FDIC also participated in the BCBS initiatives related to surveillance standards, remuneration, supervisory colleges, operational risk, accounting issues, corporate governance, the fundamental review of the trading book, and credit ratings and securitization. Other major issues in these work streams include the recalibration of risk weights for securitization exposures, the comprehensive review of capital charges for trading positions, and the imposition of a capital charge for exposures to central counterparties.

Under the leadership of the FDIC Vice Chairman, who also serves as the President of IADI and the Chairman of its Executive Council, IADI made significant progress in advancing the 2009 IADI and the BCBS Core Principles for Effective Deposit Insurance Systems (Core Principles). The IADI and the BCBS released a Methodology for assessing compliance with the Core Principles in December 2010. The development of the Methodology was a collaborative effort led by IADI in partnership with the BCBS, the International Monetary Fund (IMF), the World Bank, the European Forum of Deposit Insurers (EFDI), and the European Commission (EC). Early in 2011, the Core Principles and Methodology were officially recognized by the IMF and the World Bank to assess the effectiveness of deposit insurance systems in the Financial Sector Assessment Program (FSAP), where the IMF and World Bank undertake comprehensive analyses of countries’ financial sectors. Subsequently, in February 2011, the FSB approved the Core Principles and Methodology for inclusion in their Compendium of Key Standards for Sound Financial Systems. The official recognition of the Core Principles and Methodology by the IMF, the World Bank, and the FSB represent an important milestone in the acceptance of the role of effective systems of deposit insurance in maintaining financial stability.

The FSB Standing Committee on Standards Implementation (SCSI) agreed in late 2010 to conduct a thematic peer review of G20 deposit insurance systems.

The key objectives of the review are threefold: to take stock of members’ deposit insurance systems using, as a benchmark, the Core Principles; to identify any planned changes in national systems in response to the crisis; and to identify lessons on implementing deposit insurance reforms. In May 2011, the SCSI appointed a review team headed by the Deputy Chief Executive of the Hong Kong Monetary Authority, which included the FDIC’s Director of Division of Insurance and Research. The FDIC completed the questionnaire addressing key features of the U.S. deposit insurance system, reforms recently undertaken, and the status of implementing the Core Principles. The SCSI discussed the preliminary FSB report on December 13–14, 2011, and presented the report to the FSB in early 2012.

Senior FDIC officials participated in meetings of the FSB Resolution Steering Group (ReSG), and on September 26, 2011, the FDIC hosted a meeting of the ReSG at the Seidman Center. With input from the various working groups, the ReSG prepared a number of documents for consideration by the FSB and G20 Leaders. These documents covered a range of subjects relating to cross-border resolutions including the Key Attributes of Effective Resolution Regimes for Financial Institutions, which covered such areas as cross-border cooperation agreements, resolvability assessments, recovery and resolution plans, and temporary stays on early termination rights. The Key Attributes document was released as a consultative document for public comment in July, and in November 2011, was presented to the G20 Leaders Summit in Cannes, France, as part of the overall recommendations to address threats to global financial stability.

In continuing support of the Association of Supervisors of Banks of the Americas (ASBA) mission and strategic development, the FDIC participated in ASBA’s Board and technical committee meetings throughout 2011, led three technical assistance training missions in 2011, hosted the XIV ASBA Annual Assembly and Conference, and established a secondment program for ASBA members. Under the newly created secondment program, up to four ASBA members per year will be selected to participate in a ten-week developmental program at the FDIC wherein the selected officials will get an “insider’s view” of key Division of Risk Management Supervision (RMS) policy and operational systems. In recognition of the FDIC’s leadership in the Association, the General Assembly elected FDIC’s Director of RMS to serve a two-year term as Vice Chairman. |

A delegation from Ukraine visits the FDIC’s Dallas Regional Office to learn about franchise and asset marketing and other bank resolution topics. Delegation members with FDIC staff.

From left: Sergii Naboka, Roman Rym, Andrii Olenchyk, Nataliia Lapaieva, and Liudmyla Lashchuk, all of the Deposit Guarantee Fund, Ukraine; George Fitz, DRR; Oleksii Tkachenko, National Bank of Ukraine; Jim Gallager, DRR; and Bob Carpenter, Legal. |

The FDIC continued to provide technical assistance through training, consultations, and briefings to foreign bank supervisors, deposit insurance authorities, and other governmental officials, including the following:

- The FDIC, on behalf of IADI, provided the content and technical subject matter expertise in the development of a tutorial on the Core Principles, which was released through the Financial Stability Institute’s (FSI) Connect online system. The FDIC led the development of the IADI training seminar on “Deposit Insurance Assessments and Fund Management” and hosted the IADI executive training seminar. Working with the IADI Core Principles Working Group, the FDIC designed and led workshops on conducting assessments of the Core Principles. The design included development of a Handbook for Conducting an Assessment, applying the methodology approved by the IADI and BCBS. The training seminars were held in Washington, DC; Tirana, Albania; Basel, Switzerland; and Abuja, Nigeria.

- The FDIC provided speakers to ASBA for several technical seminars including Credit Risk Analysis, Supervision of Operational Risk, and Financial Institution Analysis Training.

- The FDIC hosted 106 visits with over 825 visitors from approximately 48 jurisdictions in 2011. In addition to several meetings with UK officials, the FDIC met with representatives from the Bank of Canada, Canada Department of Finance, the Office of the Superintendent of Financial Institutions, and the Canada Deposit Insurance Corporation. The purpose of the meeting with the Canadians was to discuss living wills and the resolution process for large complex financial institutions. The heads of the Indonesia Deposit Insurance Corporation, the Fondo Interbancario di Tutela dei Depositi (FITD) from Italy, the Instituto para la Protección de Ahorro Bancario (IPAB) from Mexico, and other senior staff from their respective agencies visited the FDIC for multi-day study tours. The delegations met with senior FDIC management and staff to learn about FDIC policies and procedures in a range of areas, including public affairs, bank resolutions, and fund management.

- June 1, 2011, marked the four-year anniversary of the secondment program agreed upon by the Financial Services Volunteer Corps (FSVC) and the FDIC to place one or more FDIC employees full-time in FSVC’s Washington, DC, office. In 2011, the FDIC provided support to several projects supporting the Central Bank of Iraq’s (CBI) bank supervision program. The support included multiple training sessions, as well as a commentary addressing strategic recommendations and an overview of the effectiveness of the current bank supervisory program. Under the FDIC’s guidance, the CBI has begun to build the technical skills needed for effective regulation of Iraq’s banks. In addition, the FDIC welcomed two examiners from the Central Bank of Russia to shadow FDIC examiners during the on-site examination of a commercial bank in Texas. This shadowing assignment provided the Russians a unique opportunity to observe a U.S. bank examination and to develop new skills in their risk analysis toolkit.

- As an additional element of its leadership role in promoting effective bank supervision practices, the FDIC provides technical assistance, training, and consultations to international governmental banking regulators in the area of Information Technology (IT) examinations. The FDIC sent two IT examiners to Serbia on December 5–9, 2011. The IT examiners participated in an assessment of the National Bank of Serbia’s IT Supervision Program. The assessment included banking practices, applicable regulations, and staff skill levels. This assessment will be used to identify and prioritize measures needed to strengthen and improve the IT supervision program in Serbia. The engagement was organized by the World Bank as part of a larger program to strengthen independent banking in Serbia.

- In 2011, the FDIC hosted the China Banking Regulatory Commission (CRBC) to provide an overview of the IT examination process and the roles and responsibilities of the FDIC in the US bank regulatory environment.

- As part of IPAB’s visit in September 13, 2011, Acting Chairman Gruenberg and IPAB Executive Secretary Mr. José Luis Ochoa signed a technical assistance memorandum of understanding (MOU) that formally establishes a collaborative and cooperative relationship between the FDIC and IPAB. An MOU for technical assistance was also established with the Deposit Guarantee Fund (DGF) of Ukraine that provides for ongoing communication with the DGF as they await the passage of a new law granting the DGF expanded powers to resolve problem banks and serve as receiver of the failed bank estates.

- During 2011, the FDIC provided subject matter experts to participate in 17 FSI seminars around the world. The topics included implementation of an international leverage ratio, effective macro prudential tools, stress testing, supervising credit risk, SIFI and bank resolutions, governance, accounting, deposit insurance, and risk-based supervision.

. |

| Previous | Contents | Next |

| Last Updated

09/05/2012 |

communications@fdic.gov |

|