|

2008 Annual Report

The Banking Crisis

|

Consequences of Failure

Oklahoma’s Penn Square Bank speculated heavily in oil and gas lending. The construction of its new headquarters was halted by the bank’s failure in 1982.

Image courtesy of the Oklahoma Historical Society |

The banking crisis of the 1980s and 1990s was the greatest challenge the FDIC had ever faced. The crisis had four main causes. Boom-and-bust economic activity occurred in certain regions and economic sectors. Legal restrictions on branching made banks more vulnerable to regional and sectoral recessions. Many banks exhibited weak risk management. And inappropriate government policies, such as less-frequent bank examinations, also played a role.

Agriculture

A 1970s boom in farm commodity prices and farm real estate values was followed by a downturn in the early 1980s. Many banks that concentrated in agricultural lending failed.

Energy

Soaring oil prices in the 1970s and early 1980s generated a boom in the Southwest. When energy prices dropped sharply, the region’s economy was devastated and many banks failed.

Real Estate

Both the Northeast and California had booming economies in the 1980s. But aggressive real estate lending led to overbuilding and inflated prices. When recessions struck in the early 1990s, banks in both regions failed.

The S&L Crisis

Deregulation let S&Ls enter new fields where they had little expertise. In addition, capital standards were lax and supervision inadequate. Given government policy and the FSLIC’s lack of resources, many institutions that should have been closed stayed open. By 1986, the industry was clearly in crisis—672 S&Ls and the FSLIC itself were insolvent.

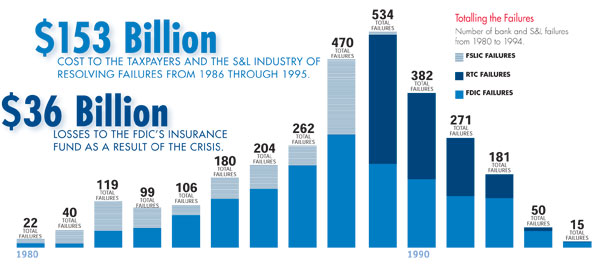

Crisis and Resolution

From 1980 through 1994, a total of 1,618 banks failed. The FDIC handled these failures without the public losing confidence in the banking system and without the need for taxpayer funding. By the early 1990s, favorable interest rates and economic conditions helped the industry rebound and enter a period of unparalleled growth and profitability.

Banking REFORM

In 1991, a new law strengthened the insurance funds and increased regulatory supervision. Its provisions called for insurance premiums based on risk and annual on-site examinations of most banks and thrifts. Regulators also were required to take “prompt corrective action” against weakening institutions and to close critically undercapitalized institutions at the least cost to the FDIC.

Image courtesy of the National Archives |

On August 9, 1989, President George H.W. Bush signed the Financial Institutions Reform, Recovery, and Enforcement Act.

Image courtesy of the George Bush Presidential Library and Museum |

S&L Reform

In 1989, a new law reformed the S&L industry, imposing stricter capital requirements and limiting investment and lending activities. The industry’s regulatory structure was overhauled. The FSLIC was abolished, and the FDIC became the federal deposit insurer of thrifts. S&Ls received a new federal regulator, the Office of Thrift Supervision, and the Resolution Trust Corporation (RTC) was created to dispose of the assets of failed thrifts.

Resolving the S&L Crisis

The RTC, operating from 1989 to 1995, resolved 747 failed thrifts with assets of about $450 billion, successfully ending the thrift crisis. FDIC personnel and expertise were essential to the creation and operation of the RTC, and the FDIC managed the RTC during its first two years.

22,586 – Number of FDIC and RTC employees at year-end 1991.

|