Examination Program

The FDIC's strong bank examination program is the core of its supervisory program. At year-end 2007, the Corporation was the primary federal regulator for 5,257 FDIC-insured state-chartered institutions that are not members of the Federal Reserve System (generally referred to as "state nonmember" institutions). Through safety and soundness, consumer compliance and Community Reinvestment Act (CRA), and other specialty examinations, the FDIC assesses their operating condition, management practices and policies, and their compliance with applicable laws and regulations. The FDIC also educates bankers and consumers on matters of interest and addresses consumers' questions and concerns.

In 2007, the Corporation conducted 2,258 statutorily-required safety and soundness examinations, including a review of Bank Secrecy Act compliance, and all required follow-up examinations for FDIC-supervised problem institutions within prescribed time frames. The FDIC also conducted 1,773 CRA/Compliance examinations (1,241 joint CRA/compliance examinations, 528 compliance-only examinations,2 and four CRA-only examinations) and 2,941 specialty examinations. All CRA/compliance examinations were also conducted within the time frames established by FDIC policy, including required follow-up examinations of problem institutions. The accompanying table compares the number of examinations, by type, conducted in 2005, 2006 and 2007.

| FDIC Examinations 2005 - 2007 |

| |

2007 |

2006 |

2005 |

|---|

| Safety and Soundness: |

| State Nonmember Banks |

2,039 |

2,184 |

2,198 |

| Savings Banks |

213 |

201 |

199 |

| Savings Associations |

3 |

2 |

1 |

| National Banks |

0 |

0 |

0 |

| State Member Banks |

3 |

1 |

1 |

| Subtotal - Safety and Soundness Examinations |

2,258 |

2,388 |

2,399 |

| CRA/ Compliance Examinations: |

| Community Reinvestment Act - Compliance |

1,241 |

777 |

815 |

| Compliance - only |

528 |

1,177 |

1,198 |

| CRA - only |

4 |

5 |

7 |

| Subtotal CRA/ Compliance Examinations |

1,773 |

1,959 |

2,020 |

| Specialty Examinations: |

| Trust Departments |

418 |

468 |

450 |

| Data Processing Facilities |

2,523 |

2,584 |

2,708 |

| Subtotal - Specialty Examinations |

2,941 |

3,052 |

3,158 |

| Total |

6,972 |

7,399 |

7,577 |

As of December 31, 2007, there were 77 insured institutions with total assets of $22.2 billion designated as problem institutions for safety and soundness purposes (defined as those institutions having a composite CAMELS3 rating of "4" or "5"), compared to the 51 problem institutions with total assets of $8.5 billion on December 31, 2006. This constituted a 51 percent year-over-year increase in the number of problem institutions and a 161 percent increase in problem institution assets. During 2007, 38 institutions with aggregate assets of $6.4 billion were removed from the list of problem financial institutions, while 64 institutions with aggregate assets of $26.5 billion were added to the list of problem financial institutions. The FDIC is the primary federal regulator for 47 of the 77 problem institutions.

During 2007, the Corporation issued the following formal and informal corrective actions to address safety and soundness concerns: 48 Cease and Desist Orders, three Temporary Cease and Desist Orders, one modified Cease and Desist Order, and 158 Memoranda of Understanding. Of these actions issued, 25 Cease and Desist Orders and 31 Memoranda of Understanding were issued based, in part, on apparent violations of the Bank Secrecy Act.

As of December 31, 2007, 43 FDIC-supervised institutions were assigned a "4" rating for safety and soundness and four institutions were assigned a "5" rating. Forty-two of the "4"-rated institutions were examined in 2007, and formal or informal enforcement actions have been finalized to address the FDIC's examination findings. All "5"-rated institutions were examined in 2007.

As of December 31, 2007, eight FDIC-supervised institutions were assigned a "4" rating for compliance; no institutions were assigned a "5" rating. In total, three of the "4"-rated institutions were examined in 2007; three were examined prior to 2007 but are currently in various stages of appealing the ratings, and the remaining two were examined in 2006. With regard to the two for which examinations were last conducted in 2006, an informal enforcement action for one was issued in September 2007; therefore, an examination is not due until 2008. The other institution is operating under a Cease and Desist Order and the examination remains open.

The Corporation has issued enforcement actions to address the examination findings for all five of the institutions that were not in the process of an appeal. These actions include one Cease and Desist Order as noted above and four Memoranda of Understanding.

Revisions to Compliance Examination Guidance

The FDIC conducted an internal analysis of compliance examination reports to determine if appropriate follow-up action is initiated on significant violations cited during compliance examinations. The review revealed that a change was needed to clarify guidance to ensure that the most problematic weaknesses and significant violations cited in examination reports are promptly addressed by bank management. In response, a Regional Director Memorandum entitled, Compliance Examination Process: Clarification of "Significant" Violations and Amendments to Enforcement Action and Post-Examination Processes was issued in 2007. The post-examination follow-up process was formalized, through which state nonmember banks will be required to respond to examination staff in writing, outlining actions planned and taken to address identified deficiencies including significant violations. This process will enable the FDIC to more consistently assess an institution's success or failure in addressing the issues during the interim period between examinations.

Joint Examination Teams

The FDIC used joint compliance/risk management examination teams (JETs) to assess risks associated with new, nontraditional and/or high-risk products being offered by FDIC-supervised institutions. The JET approach recognizes that to fully understand the potential risks inherent in certain products and services, the expertise of both compliance and risk management examiners is required. The JET approach has three primary objectives:

- To enhance the effectiveness of the FDIC's supervisory examinations in unique situations;

- To leverage the skills of examiners who have experience with emerging and alternative loan and deposit products; and

- To ensure that similar supervisory issues identified in different areas of the country are addressed consistently.

The JET concept evolved from the FDIC's examination of state nonmember banks that were conducting payday lending activities through third-party vendors. Payday lending involved unique and complex products with significant safety and soundness and consumer protection risks for the institutions involved in this activity. Joint examination teams were subsequently used in the examination of credit card lenders that were targeting subprime customers. As with the payday lenders, such products present a myriad of safety and soundness and consumer protection risks for these lenders.

In 2007, the FDIC has used JETs in institutions involved in significant subprime or nontraditional mortgage activities; institutions affiliated with or utilizing third parties to conduct significant lending activities, especially in the credit card area; and institutions for which the FDIC has received a high volume of consumer complaints or complaints with serious allegations of improper conduct by banks.

Subprime Hybrid Adjustable Rate Mortgages

In 2007, the FDIC continued to closely monitor the expansion of subprime hybrid adjustable rate mortgages (ARMs), typically offered to subprime borrowers. Hybrid ARMs start with a low fixed interest rate for an initial period, which often lasts for two to three years, and then resets to a variable rate. Mortgage lenders typically qualified borrowers based on the low introductory payment amount rather than at the fully indexed interest rate, assuming a fully amortizing repayment schedule. Such underwriting standards and loan terms can cause payment shock, the consequences of which may not have been fully explained to borrowers. In addition, many lenders combined these loans with other potentially risky features, such as requiring little or no documentation of income, high loan-to-value ratios, and simultaneous second-lien mortgages, which could compound the risk to both borrowers and lenders.

To address these concerns, the FDIC joined the other federal financial institution regulatory agencies in issuing the Statement on Subprime Mortgage Lending (Subprime Guidance) on July 10, 2007. The guidance covers three primary areas: risk management practices, consumer protection principles, and control systems. The risk management section focuses on avoiding predatory lending, following prudent underwriting standards for qualifying borrowers, and encouraging institutions to work constructively with residential borrowers who are in default or whose default is reasonably foreseeable.

The consumer protection principles section recommends that communications with consumers, including advertisements, oral statements and promotional materials, provide borrowers with full and balanced information about the costs, terms, features and risks of subprime hybrid ARMs in a timely manner. The FDIC joined the other regulatory agencies in providing illustrations for disclosures for public comment. The control systems section specifies that institutions should develop and implement strong control systems to monitor whether their subprime lending activities are performing as expected, and whether actual practices are consistent with their policies and procedures. These systems should monitor both the institution's personnel and third party originators, such as mortgage brokers or correspondents.

Working through Mortgage Resets

The FDIC became increasingly concerned about borrowers' ability to service the higher debt load resulting from payment shock when their hybrid ARMs payments reset. Many borrowers, especially those who were qualified at a low introductory payment amount rather than the fully indexed interest rate and on a fully amortizing repayment schedule, may not have sufficient financial capacity to make the higher contractual payments owed on their home loans.

To address this concern, the FDIC led the agencies in issuing the Statement on Working with Mortgage Borrowers in April 2007. This guidance primarily addresses those instances when a financial institution has retained a residential mortgage loan on its books. The agencies issued the Statement on Loss Mitigation Strategies for Servicers of Residential Mortgages in September 2007 to provide guidance to entities that service residential mortgage loans for others. In addition, the FDIC joined the Conference of State Bank Supervisors and the American Association of Residential Mortgage Regulators in issuing the Supplemental Information for Loss Mitigation Strategies. This guidance encourages servicers to consider the borrower's ability to repay modified obligations, taking into account the borrower's total monthly housing-related payments as a percentage of the borrower's gross monthly income.

The FDIC is encouraging servicers to adopt a streamlined approach to making the decision to grant loan modifications where necessary. Where the homeowner generally has been current at the starter rate, but cannot refinance in today's market or make the higher payments after the interest rate resets, then the loan should be modified to keep it at the starter rate for a long-term sustainable period. Such modification arrangements would also benefit lenders and investors who would not only have a higher level of performing loans, but would also avoid administrative expenses associated with servicing delinquent debts or foreclosing on the property. In addition, financial institutions may receive favorable CRA consideration for programs that transition low-to moderate-income borrowers from higher cost credit to lower cost credit, provided that the loan modifications are made in a prudent manner.

Regulatory Relief

On October 13, 2006, the President signed Public Law No. 109-351, the Financial Services Regulatory Relief Act of 2006 (FSRRA). The law required the FDIC and other federal regulatory agencies to revise certain rules and regulations and supervisory processes. In 2007, the GAO began a review of Currency Transaction Reports as required under FSRRA. The FDIC has provided the GAO with requisite information to support this review.

Regulation R

The FDIC joined the Office of the Comptroller of the Currency (OCC), the Federal Reserve Board (FRB), the Office of Thrift Supervision (OTS), and the Securities and Exchange Commission (SEC) in drafting and finalizing the joint FRB/SEC Regulation R - Definitions of Terms and Exemptions Relating to the "Broker" Exceptions for Banks. The FSRRA required the Federal Reserve, in consultation with the other federal banking regulatory agencies, and the SEC to develop a regulation implementing the exceptions for banks from the definition of broker contained in the Gramm-Leach-Bliley Act of 1999. The final Regulation R was published in the Federal Register on October 3, 2007, and became effective on December 3, 2007. Regulation R sets forth the circumstances and conditions under which banks can continue to effect securities transactions for customers without being subject to registration as a broker under the Securities Exchange Act of 1934.

Model Privacy Notices

The FDIC also worked with the other federal banking agencies, the National Credit Union Administration, the SEC and the Federal Trade Commission to develop model privacy notices that financial institutions have the option of using.

Review of the Reports of Condition

Section 604 of the Financial Services Regulatory Relief Act of 2006 requires the federal banking agencies to review the content of bank Call Reports and Thrift Financial Reports (TFR). The objective of Section 604 is for the agencies to use the results of the review as a basis for eliminating or reducing any information collected in Call Reports and TFRs found to be unnecessary or inappropriate. The Federal Financial Institution Examination Council 's (FFIEC) Task Force on Reports surveyed various Call Report user groups to identify the purposes for which each group uses each Call Report item, the extent of usage for each item, and the frequency with which each data item is needed. There were 165 survey participants from the four banking agencies and the Conference of State Bank Supervisors (CSBS). The survey was completed in August and the results were evaluated and reported to the FFIEC principals in October 2007.

FDIC Rules and Regulations

The FDIC also revised the following rules and regulations:

- Part 348 To raise the threshold allowing depository organizations with total assets of $50 million (previously $20 million) to be exempt from the prohibition against having interlocking management officials, if the depositories are located, or have an affiliate located, in the same metropolitan statistical area, primary metropolitan statistical area, or consolidated metropolitan statistical area.

- Part 337.12 To expand the examination cycle for "1" and "2"-rated community banks to 18 months by raising the asset threshold eligibility from $250 million to $500 million.

- Statement of Policy on Bank Mergers Transactions and Applicable Sections of Part 303 To eliminate the competitive factors report from other banking agencies, and the post-approval waiting period for mergers with affiliates.

- Applicable Sections of Part 308 and the Application Process To extend the time for review of a change-in-control notice to address issues arising from so-called "stripped charters." In addition, Part 308 was amended to clarify that the appropriate federal banking agency may suspend or prohibit individuals charged with certain crimes from participating in the affairs of any relevant depository institution.

- Part 309 To reflect broad authority for the FDIC to provide confidential supervisory information to any other federal or state agency or authority with supervisory or regulatory authority over the depository institution that is determined to be appropriate.

- Statement of Policy on Section 19 of the FDI Act To reflect amendments made by the Financial Services Regulatory Reform Act of 2006.

Disaster Relief

Recognizing that many communities and families may need an extended period of time to recover from the devastation caused by Hurricane Katrina, the FDIC and the other federal banking agencies issued a reminder to examiners and financial institutions to consider the principles outlined in the Hurricane Katrina Examiner Guidance. In addition, during the year the FDIC issued 12 financial institution letters that provided regulatory relief to financial institutions and facilitated recovery in areas damaged by fire, flood and other natural disasters.

Protection of Federal Benefit Payments

The FDIC, along with the other federal financial institution regulators, proposed guidance that encourages federally regulated financial institutions to follow best practices to protect federal benefit payments from garnishment orders. Federal law protects federal benefit payments such as Social Security benefits and Veterans' benefits from garnishment orders and the claims of judgment creditors, subject to certain exceptions. Creditors and debt collectors are often able to obtain orders from state courts garnishing funds in a consumer's account that do not meet the requirements of exempt funds. To comply with state court garnishment orders, financial institutions often place a temporary freeze or hold on an account upon receipt of a garnishment order, which can cause significant hardship for the account holder. The agencies developed proposed guidance, which includes best practices, to encourage financial institutions to minimize the hardships encountered by federal benefit funds recipients and to do so while remaining in compliance with applicable laws. The comment period closed in November 2007 and the agencies have reviewed the comments and will determine the best course of action during 2008.

Large Complex Financial Institution Program

The FDIC's Large Complex Financial Institution Program addresses the unique challenges associated with the supervision, insurance and potential resolution of large and complex financial institutions. A significant share of the banking industry's assets and insured deposits are held in a small number of large institutions. This program ensures a consistent approach to large-bank supervision and risk analysis on a national basis. This is achieved by compiling key data and performing analyses of large-bank operations for use by various FDIC divisions and offices, and by providing specialists with information to support supervisory activities for large banks.

In 2007, the FDIC led a comprehensive initiative to standardize data capture and reporting through the Large Insured Depository Institution (LIDI) Program. Under this Program, supervisory staff throughout the nation performs comprehensive quantitative and qualitative risk analysis on institutions with assets over $10 billion, or under this threshold at regional discretion. This information is used by various business lines to perform critical functions related to insurance, resolutions and supervision.

In 2007, the LIDI Program supported the insurance function in analyzing and setting appropriate insurance premiums for large insured financial institutions. The Corporation also led and supported various initiatives designed to better understand potential resolution challenges posed by complex insured financial institutions.

The FDIC continued to assess internal and industry preparedness relative to Basel II capital rules and was actively involved in domestic and international discussions intended to ensure effective implementation of the New Capital Accord. This included participation in numerous supervisory working group meetings with foreign regulatory authorities to address Basel II home-host issues.

Bank Secrecy Act/Anti-Money Laundering

The FDIC pursued a number of Bank Secrecy Act (BSA), Counter-Financing of Terrorism (CFT) and Anti-Money Laundering (AML) initiatives in 2007.

International AML/CFT Initiatives

The FDIC conducted three training sessions in 2007 for 57 central bank representatives from Algeria, Bosnia, Egypt, Indonesia, Jordan, Kuwait, Morocco, Pakistan, Paraguay, Philippines, Tanzania, and Turkey. The training focused on AML/CFT controls, the AML examination process, customer due diligence, suspicious activity monitoring, and foreign correspondent banking. The sessions also included presentations from the Federal Bureau of Investigation on combating terrorist financing, and the Financial Crimes Enforcement Network (FinCEN) on the role of financial intelligence units in detecting and investigating illegal activities.

In addition to hosting onsite AML/CFT instruction, the FDIC provided guidance and resources for international AML/CFT financial system assessments and training. In 2007, the FDIC provided technical assistance in Yemen and Senegal to evaluate AML controls and each country's AML statutory and legislative framework. Also, the FDIC delivered an AML presentation at the U.S.-Middle East/North Africa Private Sector Dialogue conference in Dubai, United Arab Emirates. Finally, the FDIC met with representatives from the Deposit Insurance Corporation of Japan, the Korean Financial Intelligence Unit, the Banco Central del Uruguay and the Bank of Al-Maghrib, Morocco, to discuss the AML examination process, enforcement authority and the FDIC's supervisory role in combating money laundering and other illicit financial activities.

Certification of Specialists

The FDIC continued to increase regulatory knowledge to keep abreast of current issues related to money laundering and terrorist financing as an additional 10 percent of BSA/AML subject matter experts nationwide earned the designation of Certified Anti-Money Laundering Specialists. As of December 31, 2007, 38 BSA subject matter experts had completed the AML certification process by passing the certification examination given by the Association of Certified Anti-Money Laundering Specialists.

Money Services Businesses Project

The FDIC developed an action plan to gain a better understanding of state regulators' AML supervision and enforcement of money services businesses (MSBs). As part of the project, the FDIC partnered with the Money Transmitter Regulators Association (MTRA), the Conference of State Bank Supervisors and FinCEN. MTRA surveyed state MSB agencies to gather BSA/AML compliance, licensing, supervision and enforcement information. The FDIC then conducted several interviews with state MSB regulators to better understand the MSB supervision process. The FDIC also conducted a pilot review to assess the feasibility of incorporating state MSB AML examination findings into FDIC risk management examinations.

2007 FFIEC BSA/AML Examination Manual

The FDIC coordinated the revision and issuance of the 2007 FFIEC BSA/AML Examination Manual. The manual was released by the FFIEC for publication and distribution on August 24, 2007. It reflects the ongoing commitment of the federal banking agencies to provide current and consistent guidance on risk-based policies, procedures and processes for banking organizations to comply with the BSA and safeguard operations from money laundering and terrorist financing. The manual has been updated to further clarify supervisory expectations and incorporate regulatory changes since its 2006 release. The revisions also reflect feedback from the banking industry and examination staff. Additionally, the FDIC had the manual translated into Spanish and responses to the Spanish language version of the manual have been positive.

Enforcement Actions

The FDIC, along with the other federal banking agencies, released the Interagency Statement on Enforcement of BSA/AML Requirements on July 19, 2007. The statement provides for greater consistency in BSA enforcement decisions and offers insight into how those decisions were made. The statement describes the circumstances and provides examples under which the federal banking agencies will issue a cease and desist order. Applicable statutes mandate that the appropriate agency shall issue a cease and desist order if a regulated institution fails to establish and maintain a BSA compliance program or correct a previously identified problem with its BSA compliance program.

Promoting Economic Inclusion

The FDIC pursued a number of initiatives in 2007 to promote inclusion of traditionally underserved populations in banking services and to ensure protection of consumers in the provision of these services.

The Advisory Committee for Economic Inclusion

The FDIC Advisory Committee on Economic Inclusion (ComE-IN) was established by Chairman Sheila C. Bair and the FDIC Board of Directors pursuant to the Federal Advisory Committee Act. The ComE-IN was chartered in November 2006, and provides the FDIC with advice and recommendations on important initiatives focused on expanding access to banking services by underserved populations.

Three ComE-IN meetings were held during 2007. The inaugural meeting addressed access to affordable small dollar loans. One recommendation that resulted was to launch a small dollar loan pilot program. The Board of Directors of the FDIC subsequently approved a two-year pilot project to review affordable and responsible small-dollar loan programs in financial institutions. The purpose of the study is to identify effective and replicable business practices to help banks incorporate affordable small-dollar loans into their other mainstream banking service offerings. Best practices resulting from the pilot will be identified and become a resource for other institutions.

The second meeting addressed the subprime mortgage situation, how it developed and possible solutions. The third meeting covered ways to ensure safe, available services for the money services businesses and examined their access to the banking system.

Alliance for Economic Inclusion

In 2007, the FDIC formally launched the Alliance for Economic Inclusion (AEI), a broad-based coalition of banks, community organizations, foundations, educators, and local, state and federal agencies in nine underserved markets across the nation the Greater Boston area; Wilmington, DE; Baltimore, MD; South Texas (Houston/Austin); Chicago; the Louisiana and Mississippi Gulf Coast; Alabama's Black Belt; Kansas City; and Los Angeles. These diverse markets include low- and moderate-income neighborhoods, urban neighborhoods, minority communities and rural areas. The goal of the AEI initiative is to work with financial institutions and other partners in select markets to bring those who are unbanked and underserved into the financial mainstream. More than 700 banks and other organizations have joined the AEI. Under the auspices of the AEI, approximately 28,000 bank accounts have been opened; 29,000 consumers have received financial education; 41 banks are developing small dollar loan programs; and 21 banks now offer remittance products allowing customers to send money to friends or family members outside the U.S.

The FDIC has also included a component of its foreclosure prevention efforts within the AEI. An AEI partnership with NeighborWorks® America to promote foreclosure prevention and education was announced on July 13, 2007. Since July, both NeighborWorks® America and FDIC have conducted more than 28 local outreach and training events. These events were designed to provide assistance to NeighborWorks® Centers for Foreclosure Solutions and other local organizations in developing and implementing strategies to educate at-risk homeowners about the availability of foreclosure prevention counseling services and other resources. Each of the nine AEI coalitions is also coordinating foreclosure prevention efforts to provide support and expand local foreclosure prevention programs already underway within their communities.

Additionally, FDIC reviewed its supervisory guidance and determined that the Case Managers Manual and the Risk Management Manual of Examination Policies should be revised to ensure that they encourage economic inclusion consistent with safe and sound banking practices.

Affordable Small-Dollar Loan Guidelines and Pilot Program

Many consumers with bank accounts turn to high-cost payday or other non-bank lenders because they are accessible and can quickly provide small loans to cover unforeseen circumstances. To help enable insured institutions to better serve an underserved and potentially profitable market while helping consumers avoid, or transition away from, reliance on high-cost debt, the FDIC issued its Affordable Small-Dollar Loan Guidelines on June 19, 2007. The guidelines explore several aspects of product development, including affordability and streamlined underwriting. They also discuss tools, such as financial education and linked savings accounts that may address long-term financial issues that concern borrowers. The guidelines also note that FDIC-supervised institutions offering products that comply with consumer protection laws, and are structured in a responsible, safe and sound manner, may receive favorable consideration under the Community Reinvestment Act (CRA).

Additionally, on June 19, 2007, the FDIC Board approved a two-year pilot project to review affordable and responsible small-dollar loan programs in financial institutions and assist bankers by identifying and disseminating information on replicable business models for small-dollar loans. A web site was developed to provide information on the pilot and participant banks were recruited for the study. Participants applied and twenty-nine were selected in 2007. During 2008, participating institutions will be asked to provide summary data to the FDIC about the loans in the program, the overall value and profitability of the program, and the benefit to consumers. Information collected will be highlighted in FDIC publications and speeches. A final report is planned for 2010.

Home Mortgage Disclosure Act

The winter 2007 edition of Supervisory Insights contained the article "Using the HMDA Pricing Data to Identify and Analyze Outliers." The article describes the process used by the FDIC for loan review and analysis at institutions that, based on an initial screening of Home Mortgage Disclosure Act (HMDA) data, have pricing practices that are potentially discriminatory. The article offers suggestions to bankers and examiners gleaned from analyses of two years of HMDA pricing data.

Economic Inclusion Surveys

During 2007, the FDIC also commenced work on two surveys intended to provide extensive new data regarding economic inclusion. Both of these survey efforts are related to a mandate in section 7 of the Federal Deposit Insurance Reform Conforming Amendments Act of 2005 requiring the FDIC to conduct a survey of FDIC-insured institutions every two years regarding their efforts to serve the unbanked. The first of these surveys, the Survey of Banks' Efforts to Serve the Unbanked and Underbanked, will be conducted during 2008 and is expected to yield significant insight about bank efforts to serve unbanked and underbanked populations. The FDIC is also exploring the feasibility of conducting a survey of U.S. households to estimate the percentage of the U.S. population that is unbanked and underbanked. The survey is scheduled to be conducted in January 2009 as a supplement to the Bureau of the Census's Current Population Survey. It is expected to yield significant new data on the extent of the population that is unbanked and/or underbanked and the reasons why some households do not make greater use of traditional banking services.

Overdraft Protection Programs Study

Over the last few years, the use of automated overdraft protection programs has significantly risen. The banking regulators published guidance on these programs in 2005. The Federal Reserve amended Regulation DD in 2006 to encompass additional disclosure and advertising requirements for certain types of automated overdraft protection programs.

With little empirical data on these programs, the FDIC has initiated a two-part Study of Overdraft Protection Programs to systematically gather information about the types, characteristics and usage of overdraft programs offered by FDIC-supervised banks. This effort will help the FDIC more fully understand this rapidly growing and changing product. The study results should help the industry develop more effective overdraft programs that better serve customers.

Information is being gathered through a survey instrument and a download of account and transaction level data requested from banks. Using the survey instrument, field staff is gathering information at 500 randomly selected institutions. The survey will gather information on how overdraft protection is offered to the public as well as how banks manage non-sufficient funds (NSF) items and programs. A data download is being requested from up to 100 institutions to gather 12 months of customer-level micro data on NSF and overdraft activity.

This study will continue through 2008 and once it has been completed, the FDIC plans to make the findings and aggregate information public. (No personally identifiable information will be gathered and no individual bank information will be published.) The FDIC will use this information to better formulate future policy decisions.

Minority Depository Institutions

The FDIC has long recognized the importance of minority depository institutions (MDIs), particularly in promoting the economic viability of minority and under-served communities. As a reflection of the FDIC's commitment to MDIs, on April 9, 2002, the FDIC issued the Policy Statement Regarding Minority Depository Institutions. The policy statement implements an outreach program designed to preserve and encourage minority ownership of financial institutions.

Since the adoption of the policy by the Board, the FDIC's National Coordinator for MDIs has maintained contact with various MDI trade associations and has met periodically with the other federal banking regulators to discuss the initiatives underway at the FDIC. The coordinator has worked to identify opportunities where the federal banking agencies might work together to assist minority institutions. Since the adoption of the policy statement, all of the FDIC regional offices have held annual MDI outreach programs, have annually contacted each FDIC-supervised MDI to offer to meet with bank boards to discuss issues of interest, and have offered to make return visits to these institutions following the examination process.

The FDIC's Minority Bankers' Roundtable series is a forum designed to, among other things, explore possible partnerships between the MDI community and the FDIC, as well as to seek input on how the FDIC can better promote the availability of technical assistance to the MDI segment of the industry. From the 2006 Roundtable sessions evolved ideas for two partnerships that were piloted during 2007. The first initiative, a "University Partnerships" pilot, is designed to do the following:

- Promote financial literacy at Historically Black Colleges and Universities (HBCUs) or other schools with a significant minority population;

- Provide the partnering MDI and the FDIC an opportunity to keep the business school deans aware of current industry issues and to build goodwill on campus; and

- Offer both the MDI and the FDIC an opportunity to showcase their respective career opportunities.

The second 2007 Roundtable initiative involved partnering with the Puerto Rico Bankers Association to deliver a high-level specialized Compliance School. This event took place from November 6-9, 2007, in San Juan, Puerto Rico, and was attended by 150 bankers. This type of partnership was the first for the FDIC and was consistent with the goal of increasing usage of FDIC technical assistance.

In July 2007, the FDIC hosted the second annual National Minority Depository Institution Conference in Miami, Florida. This event was coordinated on an interagency basis and drew approximately 170 attendees. In addition to presentations by senior officials from all of the federal banking regulatory authorities, the program covered these topics: Broadening Access to the Financial Mainstream, Opportunities for NeighborWorks® America and Minority Community Bankers, and Capital Enhancement and Investment Opportunities, including a presentation on the Community Development Financial Institution Fund. The program also included workshops on Information Technology, BSA Emerging Issues, Compliance and CRA Hot Topics, and the Revised Interagency Policy Statement on the Allowance for Loan and Lease Losses. Feedback from the attendees was overwhelmingly positive. A third annual interagency conference is planned for 2008.

Other FDIC MDI accomplishments for 2007 include the following:

- Updating the examiner guidance memorandum "Minority Depository Institution Program";

- Inviting minority bankers to speak at regional examiner training conferences to foster a better understanding by the examiners of the unique challenges MDIs face;

- Making improvements to the FDIC's external website to better organize and provide easier access to MDI information; and

- Developing a survey that was sent to all MDIs on December 21, 2007, to provide all MDIs, including those not supervised by the FDIC, an opportunity to rate the effectiveness of the FDIC's MDI program, FDIC-sponsored conferences and roundtables, outreach efforts, and technical and general assistance. The survey results and comments will be used to improve our current efforts and to develop MDI initiatives going forward.

Homeland Security

The FDIC has taken a leadership role in ensuring that the financial sector a critical part of the infrastructure of the United States is prepared for a financial emergency. As a member of the Financial and Banking Information Infrastructure Committee (FBIIC), the FDIC has sponsored a series of outreach meetings titled "Protecting the Financial Sector: A Public and Private Partnership."

Information Technology, Cyber Fraud and Financial Crimes

The FDIC and other FFIEC regulatory agencies jointly issued guidance requiring financial institutions to strengthen account access credentials in an effort to curb online fraud and protect both consumer and commercial Internet banking customers. The guidance required the implementation of stronger authentication for most institutions on or before January 1, 2007. FDIC examiners tracked and reported on compliance with the guidance during various examination activities in 2007. Details collected suggest that an overwhelming majority (94 percent) of the institutions have complied with the provisions of the guidance. Most of the remaining institutions have plans to comply. Industry feedback suggests that stronger authentication has reduced online Internet banking-related fraud through more secure access credential management practices.

Other major accomplishments during 2007 in combating identity theft included the following:

- Assisted financial institutions in identifying and shutting down approximately 1,400 "phishing" Web sites. The term "phishing" as in fishing for confidential information refers to a scam that encompasses fraudulently obtaining and using an individual's personal or financial information.

- Issued 323 Special Alerts to FDIC-supervised institutions of reported cases of counterfeit or fraudulent bank checks.

- Participated on the President's Identity Theft Task Force and five of its primary subgroups. The FDIC was one of seventeen federal agencies that participated. The Task Force submitted its report to the President on April 11, 2007. The report contains a comprehensive description of the problem as well as numerous recommendations concerning what the federal government and private industry can do to mitigate this serious problem. Since the report was submitted to the President, the FDIC continues to participate in several Task Force subgroups that are performing additional research on specific aspects of identity theft and plan to submit additional recommendations to the President in the spring of 2008.

- The FDIC, in addition to the other federal banking agencies and the Federal Trade Commission, published a final identity theft red flag regulation and guidelines on November 9, 2007. The regulation and guidelines implement sections 114 and 315 of the Fair and Accurate Credit Transactions Act of 2003. Compliance is expected by November 1, 2008.

Consumer Complaints and Inquiries

The FDIC investigates consumer complaints about FDIC-supervised institutions and answers inquiries from the public about consumer protection laws and banking practices. In 2007, the FDIC received 11,624 written complaints, of which 4,457 were against state nonmember institutions. The Corporation responded to over 93 percent of these complaints within timeliness standards established by corporate policy. The FDIC also responded to 3,656 written and 3,321 telephone inquiries from consumers regarding state nonmember institutions. Overall in 2007, the FDIC handled 5,856 consumer telephone calls from the public and members of the banking community about consumer protection issues not including deposit insurance inquiries which are discussed on the following page.

Deposit Insurance Education

An important part of the FDIC's role in insuring deposits and protecting the rights of depositors is ensuring that bankers and consumers have access to accurate information about the FDIC's deposit insurance rules. The FDIC has an extensive deposit insurance education program consisting of seminars for bankers, electronic tools for estimating deposit insurance coverage, and written and electronic information targeted for both bankers and consumers. The FDIC also responds to thousands of telephone and written inquiries each year from consumers and bankers regarding FDIC deposit insurance coverage.

Effective October 12, 2006, the FDIC Board of Directors adopted final rules that implemented provisions of the Federal Deposit Insurance Reform Act of 2005 pertaining to deposit insurance coverage. Following the adoption of the final rule changes, the FDIC completed a multi-pronged effort in 2007 to update numerous publications and educational tools for consumers and bankers on FDIC insurance coverage, including consumer brochures, banker resource guides, videos and the Electronic Deposit Insurance Estimator.

To address current questions and issues relating to changes in the FDIC insurance coverage of deposit accounts, the FDIC hosted two identical series of telephone seminars for bankers on the FDIC's rules for deposit insurance coverage – one series in October and one in November. Each series consisted of topics on Basic Concepts of Deposit Insurance Coverage, Coverage for Retirement and Employee Benefit Plan Accounts, Trust Account Coverage, and Coverage for Business and Government Accounts. The seminars were designed to provide bankers with a comprehensive review of the FDIC's rules for deposit insurance coverage. These free seminars were open to employees of all FDIC-insured banks and savings associations. The telephone conferences were attended by bankers in approximately 11,000 locations. Many of these locations represent bank branch offices where multiple employees took part in the training.

The FDIC coordinated with bank trade associations to conduct seven comprehensive seminars for financial institution employees on the rules for deposit insurance coverage. These seminars, which were conducted in classroom settings throughout the United States, provided a comprehensive review of how FDIC insurance works, including the 2006 changes to the FDIC's final rules for insurance coverage.

The FDIC also completed a comprehensive and authoritative resource guide for bankers, attorneys, financial advisors and similar professionals on the FDIC's rules and requirements for deposit insurance coverage of revocable and irrevocable trust accounts. The new trust guidebook will be published on the FDIC's Web site in the first quarter of 2008.

In 2007, the FDIC received over 119,000 telephone and written inquiries from consumers and bankers regarding federal insurance coverage of bank deposits. Of these inquiries, 4,125 required formal written responses, 98 percent of which were completed within timeliness standards established by corporate policy.

Financial Education and Community Development

In 2001, the FDIC recognizing the need for enhanced financial education across the country inaugurated its award-winning Money Smart curriculum, which is now available in six languages, large print and Braille versions for individuals with visual impairments and a computer-based instruction version. Since its inception, over 1.4 million individuals (including approximately 200,000 in 2007) have participated in Money Smart classes and self-paced computer-based instruction. Approximately 163,000 of these participants have subsequently established new banking relationships. During 2007, the FDIC updated and enhanced the Money Smart curriculum and training tools. These changes included guidance on consumer-related concerns such as identity theft, remittances and how to assess mortgage product options.

In recognition that public schools are one of the best venues for reaching the next generation of consumers of all income levels, the FDIC embarked on a pilot project to expand its outreach and enhance the availability of the Money Smart financial curriculum in high schools. Over 339 schools, school systems and related entities have been contacted regarding the availability of Money Smart. Several hundred secondary school teachers and volunteers have been trained to deliver Money Smart. The FDIC also began work on developing a Money Smart curriculum for young adults.

The FDIC completed a major multi-year study in 2007 to evaluate the effectiveness of the Money Smart curriculum. The study, A Longitudinal Evaluation of the Intermediate-term Impact of the Money Smart Financial Education Curriculum upon Consumers' Behavior and Confidence, shows that the training can positively influence how people manage their finances. The survey examines the impact of financial education on the behavior of a broad audience up to one year after completing the training. The goal was to measure, over time, not only whether trainees' knowledge of financial matters improved, and whether they intended to change their financial behaviors, but also whether, months after the training, they had actually acted on their intentions. Survey results indicate that those who took the Money Smart course were more likely to open deposit accounts, save money, use and adhere to a budget, and have increased confidence in their financial abilities when contacted 6 to 12 months after completing the course. A majority of those surveyed reported an increase in personal savings, a decrease in debt, a better understanding of financial principles, and an increased willingness to comparison shop for financial services.

During 2007, the FDIC also undertook over 195 community development, technical assistance and outreach activities. These activities were designed to promote awareness of investment opportunities to financial institutions, access to capital within communities, knowledge-sharing among the public and private sector, and wealth-building opportunities for families. Representatives throughout the financial industry and their stakeholders collaborated with the FDIC on a broad range of initiatives structured to meet local and regional needs for financial products and services, credit, asset-building, affordable housing, small business and micro-enterprise development and financial education.

International Outreach

During 2007, the FDIC focused its international programs and activities toward the goal of helping to build strong and effective systems for protecting depositors, supervising financial institutions and resolving failures. Efforts included arranging and conducting training sessions, technical assistance missions and foreign visits, leadership roles in international organizations, bilateral consultations with foreign regulators, and many other activities and consulting services.

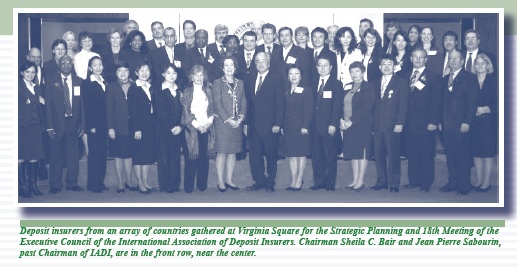

The FDIC's strengthened international leadership role paved the way for the election of the FDIC's Vice Chairman to the position of President of the International Association of Deposit Insurers (IADI) and Chair of the IADI Executive Council. In addition, the Vice Chairman, as Chair of the IADI Training and Conference Standing Committee, developed and led the first-ever Executive Training Program, providing training to 35 IADI members from 27 countries. The FDIC was elected for the first time to serve on the Board of Directors for the Association of Supervisors of Banks in the Americas (ASBA) and to represent the North American Region. The FDIC's leadership within ASBA included providing technical training to ASBA members on operational risk management and leading two working groups in developing ASBA guidance on key supervisory issues. The FDIC also established strong working relationships and presented at several European Forum of Deposit Insurers (EFDI) meetings, including the EFDI/IADI Joint Symposium on Cross Border Issues.

The FDIC continued to enhance the effectiveness and broaden the scope and impact of its three primary international programs – technical assistance, foreign visitors and training. The FDIC provided technical assistance to 12 central banks, bank supervisors and deposit insurers from 11 countries. A highlight of this assistance was an expanded partnership with the Financial Services Volunteer Corp (FSVC) in supporting the Central Bank of Egypt in developing an examiner commissioning program. The FDIC also provided critical technical assistance to Albania on resolution practices and the legal framework for establishing the backup financial support from the government to strengthen the deposit insurance safety net. In addition, the FDIC hosted 66 foreign country visits, including 417 foreign visitors from 28 countries. Noteworthy among these visits was the second U.S.-China Seminar on Bank Supervision, delegations representing parliament officials from South Africa, United Kingdom, Sweden and Italy, and an extended visit by board members and staff of the Nigerian Deposit Insurance Corporation. Lastly, 168 foreign students from 17 countries received training in examinations, financial institution analysis, loan analysis, examination management, information technology examination, and anti-money laundering and counter-terrorism financing.

The FDIC expanded relationships with key international banking and deposit insurance organizations by expanding the secondment program (detailing staff from one country to another), technical assistance agreements and initiating new supervisory information sharing agreements. Secondment Memoranda of Understanding (MOU) were entered into with Japan, Albania, Poland, Nicaragua, and Korea to allow for selected employees from these countries to come to the FDIC to receive training and gain expertise in areas of supervision, resolution management and deposit insurance. Technical assistance agreements were executed with the People's Bank of China and the U.K. Financial Services Authority, providing FDIC subject matter expertise in promoting deposit insurance best practices. Notable examples of forging strong relationships with key countries included the FDIC Chairman's visits to China, Japan and South Korea, the Vice Chairman's visits to Malaysia, Turkey and other IADI- and EFDI-member countries and the Chief Operating Officer's visits to Russia, China and the United Kingdom. The FDIC also entered into supervisory information sharing MOUs with Brazil, Argentina, the Netherlands, and Australia.