Banking Issues in Focus provides an in-depth analysis of topical banking issues. These articles range from timely analysis of economic and banking trends at the national and regional level that may affect the risk exposure of FDIC-insured institutions to research on issues affecting the banking system and the development of regulatory policy.

In the past, these articles were featured in FDIC Quarterly Volumes.

Recent Articles

Leveraged Lending and Corporate Borrowing: Increased Reliance on Capital Markets, With Important Bank Links

By Frank Martin-Buck (2019)

Over the past decade, U.S. nonfinancial corporate debt reached record highs as issuance of corporate bonds and leveraged loans grew rapidly while credit quality and lender protections deteriorated. Much of this growth in corporate borrowing came through capital markets, though important connections to the banking system remain. This article examines this shift in corporate borrowing to capital markets over the past several decades. It also details the ways corporate debt has grown, the resulting risks this shift poses to banks since the 2008 financial crisis, and what factors could mitigate those risks.

Read article

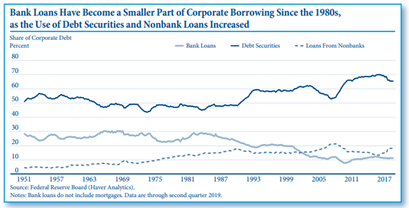

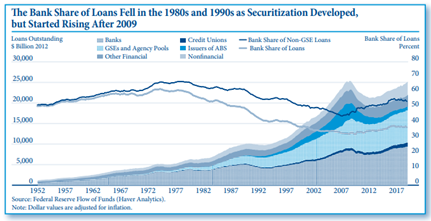

Bank and Nonbank Lending Over the Past 70 Years

By Kathryn Fritzdixon (2019)

Total lending in the U.S. has grown dramatically in the past 70 years and since the 1970s, the share of bank loans has generally fallen as nonbanks gained market share in residential mortgage and corporate lending. In other business lines, shifts in loan holdings from banks to nonbanks have been less pronounced as banks and nonbanks continue to play important roles in lending for commercial real estate, agricultural loans, and consumer credit. Studying the roles that banks and nonbanks play in lending markets allows for a better understanding of how banks respond to growth in nonbank lending and the implications of associated risks for the banking sector and the broader economy.

Read article

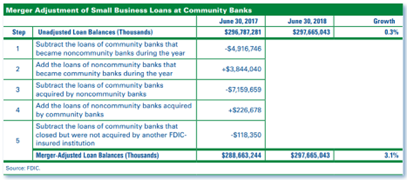

Merger Adjusting Bank Data: A Primer

By Eric Breitenstein and Derek Thieme (2018)

Analysis of banking trends often focuses on specific industry subgroups. The analyst tracks the performance or characteristics of an industry subgroup over time, and the results, if compelling, can serve as input to policy decisions. An important component of analyzing industry subgroups is a procedure called merger adjustment. This article describes how and when FDIC analysts use merger adjustment when analyzing the banking industry. It discusses when to merger adjust and when not to merger adjust and offers guidance for interpreting the results.

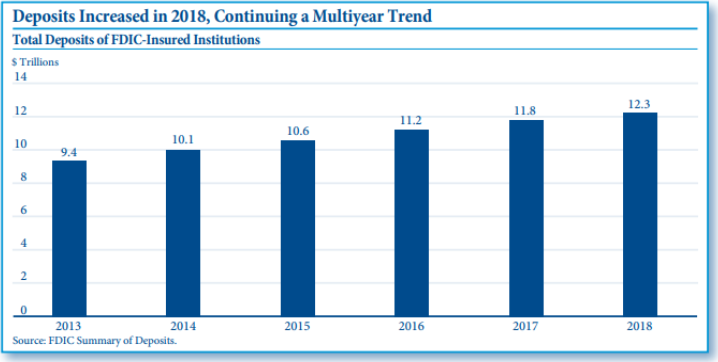

2018 Summary of Deposits Highlights: Deposit Growth Slows and Office Decline Continues

By Joseph Harris III, Derek Thieme and Angela Woodhead (2018)

The 2018 Summary of Deposits Survey showed that FDIC-insured institutions reported an increase in deposits and a decrease in offices over the past year. During the year ended June 2018, deposits increased at both noncommunity banks and at community banks, but at slower rates than in recent years. The decrease in the number of offices is a decade-long trend in both community banks and noncommunity banks, although the office opening and closing patterns of these two types of institutions has differed markedly. This article will describe these trends in detail and will look at the association between office closures and changes in bank profitability and efficiency. Analysis of Call Report data indicates that banks that closed offices at higher rates between 2013 and 2018 reported improved efficiency ratios and stronger profitability.

Read article

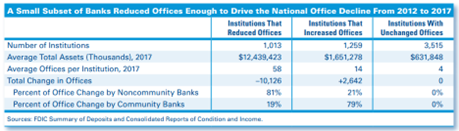

Factors Shaping Recent Trends in Banking Office Structure for Community and Noncommunity Banks

By Nathan Hinton, Derek Thieme and Angela Woodhead (2017)

Total industry deposits grew once again in 2017, and the rate of deposit growth was higher at community banks than at noncommunity banks, according to the 2017 Summary of Deposits (SOD) survey. Key findings from the SOD survey also show that the number of offices operated by noncommunity banks declined on a merger-adjusted basis in the most recent year and over the past five years, while the number of community bank offices increased slightly over both intervals. Relatively few banks have reported a net decline in their number of offices over the past five years, yet cutbacks in offices at these banks have been large enough to drive a sizable decline in the overall number of banking industry offices since 2012. This continuing trend of fewer banking offices can be attributed to factors such as population migration, office expense mitigation, industry consolidation, and financial technology.

Read article