Banking Issues in Focus provides an in-depth analysis of topical banking issues. These articles range from timely analysis of economic and banking trends at the national and regional level that may affect the risk exposure of FDIC-insured institutions to research on issues affecting the banking system and the development of regulatory policy.

In the past, these articles were featured in FDIC Quarterly Volumes.

Recent Articles

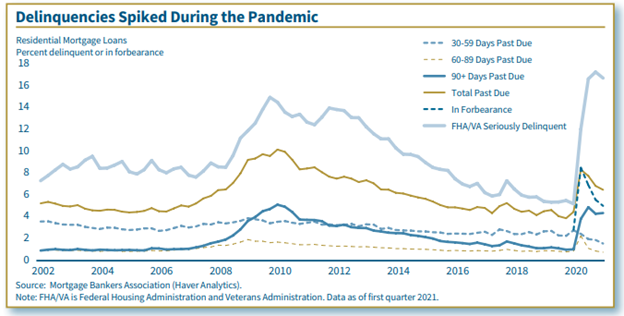

Residential Lending During the Pandemic

By Cynthia Angell (2021)

The housing market rebounded from the COVID-19 pandemic-induced recession faster than other sectors of the economy, helped by historically low interest rates and fiscal support. Still, weaker economic fundamentals led to tightening of mortgage credit and underwriting standards as lenders sought to reduce credit risk from new mortgages. Mortgage credit performance improved after deteriorating at the start of the pandemic, but high rates of delinquent loans reflect lingering financial distress for many borrowers. The coming expiration of federal programs that have aided homeowners raises concern about the possible increased risk of mortgage credit quality deterioration and reduced credit availability. Nevertheless, banks have been resilient and, despite the uncertain outlook, continue to extend residential loans.

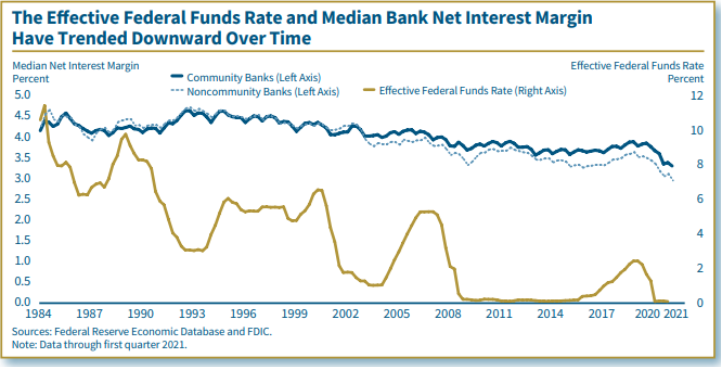

The Historic Relationship Between Bank Net Interest Margins and Short-Term Interest Rates

By Angela Hinton and Chester Polson (2021)

The years since the Great Recession generally demonstrate that protracted periods of low interest rates tend to compress net interest margin (NIM) at FDIC-insured banks. NIM decreased during the period of historically low interest rates after that recession, increased during the upward interest rate cycle between 2015 and 2019, and decreased again as interest rates fell toward zero with the onset of the COVID-19 pandemic. In most rate cycles since the 1980s, the median NIM, representative of typical banks, has moved in the same direction as changes in the federal funds rate. But this relationship has been much less pronounced for banks with high concentrations of long-term assets. Those banks with a relatively high proportion of long-term assets to total assets report greater insulation from changes in short-term interest rates. This means that their NIM falls less during downward rate cycles but rises less during upward rate cycles. The overall positive relationship between short-term interest rates and NIM and the effect of maturity structure on this relationship generally hold true over time for both community and noncommunity banks.

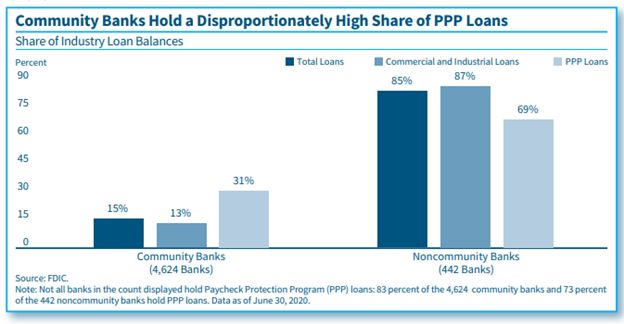

The Importance of Community Banks in Paycheck Protection Program Lending

By Margaret Hanrahan and Angela Hinton (2020)

During the current public health emergency, community banks are playing a vital role in supporting small businesses through the Small Business Administration’s Paycheck Protection Program (PPP). Community banks throughout the country participated in the program, with community bank PPP loan portfolios representing over 30 percent of total bank PPP loans.

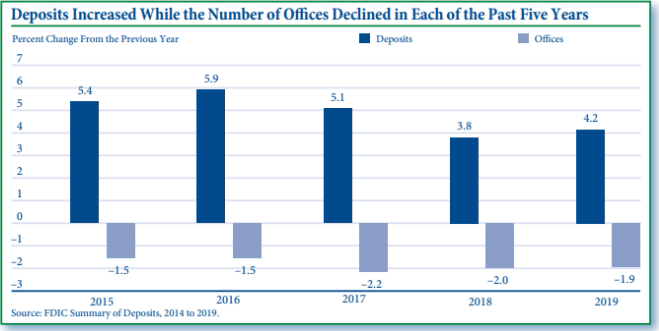

2019 Summary of Deposits Highlights

By Joseph Harris III, Caitlyn Kasper, Christopher Raslavich and Derek Thieme (2020)

The 2019 Summary of Deposits Survey showed an increase in deposits and a decrease in the number of branch offices, continuing recent trends. The reduction in the number of bank offices occurred nationwide, but the number of counties with a banking office has remained relatively stable over the past five years. The rate of decline was faster among offices in metropolitan counties, limited-service offices, and offices with lower reported levels of deposits. This article examines characteristics of the offices of operating banks that close versus those that are sold or leased, and of offices that close versus those that remain open after bank acquisitions. The rate of deposit growth increased for both community and noncommunity banks, but the merger-adjusted or “organic” rate of deposit growth at community banks exceeded that of noncommunity banks for the third consecutive year. For selected topics, comparative information about credit unions is included.

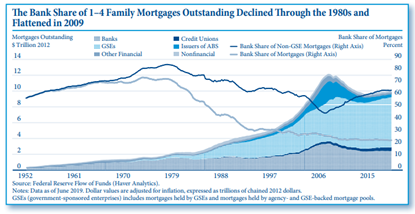

Trends in Mortgage Origination and Servicing: Nonbanks in the Post-Crisis Period

By Kayla Shoemaker (2019)

The mortgage market changed notably after the collapse of the U.S. housing market in 2007 and the financial crisis that followed. A substantive share of mortgage origination and servicing, and some of the risk associated with these activities, migrated outside of the banking system. Some risk remains with banks or could be transmitted to banks through other channels, including bank lending to nonbank mortgage lenders and servicers. Changing mortgage market dynamics and new risks and uncertainties warrant investigation of potential implications for systemic risk.