Banking Issues in Focus provides an in-depth analysis of topical banking issues. These articles range from timely analysis of economic and banking trends at the national and regional level that may affect the risk exposure of FDIC-insured institutions to research on issues affecting the banking system and the development of regulatory policy.

In the past, these articles were featured in FDIC Quarterly Volumes.

Recent Articles

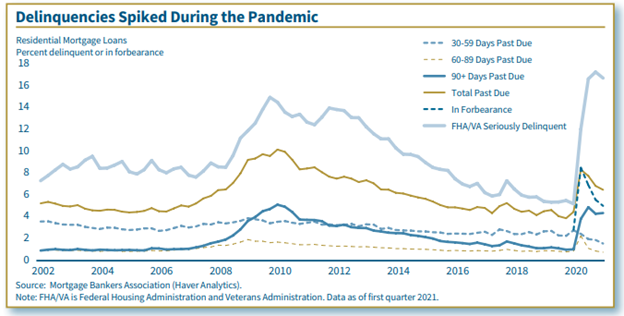

Residential Lending During the Pandemic

By Cynthia Angell (2021)

The housing market rebounded from the COVID-19 pandemic-induced recession faster than other sectors of the economy, helped by historically low interest rates and fiscal support. Still, weaker economic fundamentals led to tightening of mortgage credit and underwriting standards as lenders sought to reduce credit risk from new mortgages. Mortgage credit performance improved after deteriorating at the start of the pandemic, but high rates of delinquent loans reflect lingering financial distress for many borrowers. The coming expiration of federal programs that have aided homeowners raises concern about the possible increased risk of mortgage credit quality deterioration and reduced credit availability. Nevertheless, banks have been resilient and, despite the uncertain outlook, continue to extend residential loans.

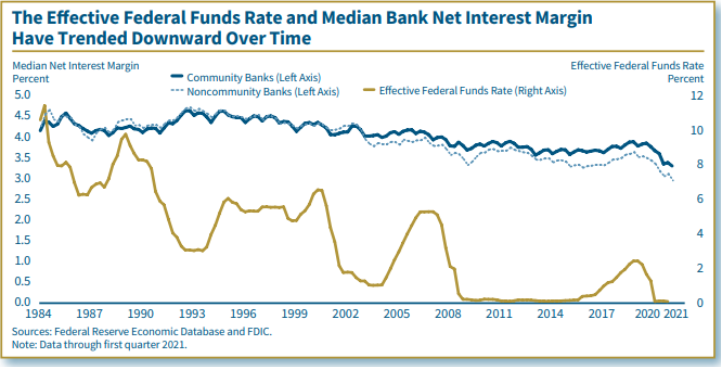

The Historic Relationship Between Bank Net Interest Margins and Short-Term Interest Rates

By Angela Hinton and Chester Polson (2021)

The years since the Great Recession generally demonstrate that protracted periods of low interest rates tend to compress net interest margin (NIM) at FDIC-insured banks. NIM decreased during the period of historically low interest rates after that recession, increased during the upward interest rate cycle between 2015 and 2019, and decreased again as interest rates fell toward zero with the onset of the COVID-19 pandemic. In most rate cycles since the 1980s, the median NIM, representative of typical banks, has moved in the same direction as changes in the federal funds rate. But this relationship has been much less pronounced for banks with high concentrations of long-term assets. Those banks with a relatively high proportion of long-term assets to total assets report greater insulation from changes in short-term interest rates. This means that their NIM falls less during downward rate cycles but rises less during upward rate cycles. The overall positive relationship between short-term interest rates and NIM and the effect of maturity structure on this relationship generally hold true over time for both community and noncommunity banks.

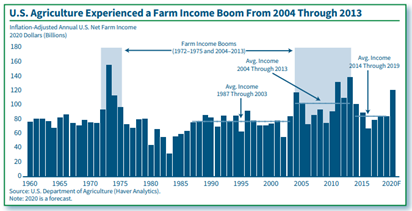

Farm Banks: Resilience Through Changing Conditions

By Richard Cofer Jr. and John M. Anderlik (2021)

The U.S. agricultural sector has experienced large swings over the past decade and a half, from a lengthy period of prosperity in agriculture that ended in 2013 to subsequent years that presented a slow, weak recovery. Most farmers and farm banks were cautious with farm real estate lending during the strong years. As a result, farm banks have held up well despite the agricultural industry’s challenges since 2014. The COVID-19 pandemic initially looked to be harmful for U.S. agriculture, but record government payments helped forecasted 2020 farm income reach the highest level since 2013.

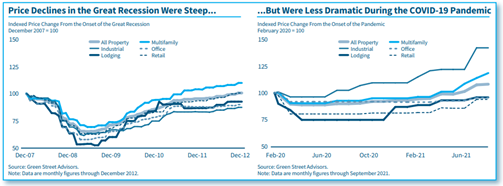

Commercial Real Estate: Resilience, Recovery, and Risks Ahead

By Jeffrey Ayres, Robert DiChiara, Alexander Gilchrist, James Presley-Nelson and Stephen Simpson (2021)

Commercial real estate (CRE) lending is important to the banking industry, which holds $2.7 trillion in CRE loans. In the pandemic, CRE conditions in several property types came under stress. The pandemic challenged the brick-and-mortar retail, hotel, and office sectors, while multifamily largely held up and the industrial sector benefitted from increased demand. Market conditions improved with economic recovery in 2021, but some of the changes the CRE industry experienced in the pandemic may be long-lasting. The issues facing CRE will be important considerations for a large share of the banking industry. Initially the pandemic threatened to significantly challenge banks’ CRE loan quality, but loan delinquency rates remained low through third quarter 2021 against the backdrop of economic rebound, stimulus support, and loan forbearance. This article analyzes conditions across major CRE property types and discusses FDIC-insured institutions’ exposure to CRE loans, credit quality, and potential challenges ahead.

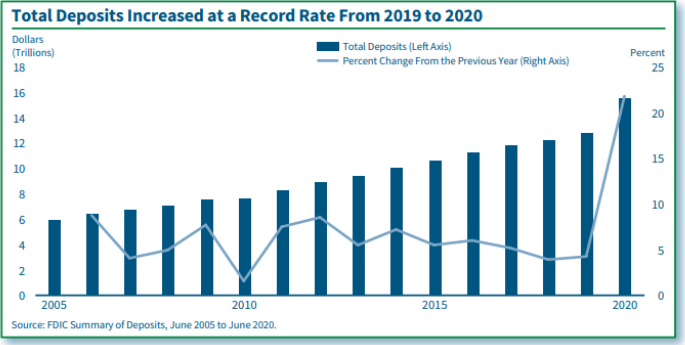

2020 Summary of Deposits Highlights

By Joseph Harris III, Caitlyn Kasper, Camille Keith and Derek Thieme (2021)

The 2020 Summary of Deposits Survey showed deposit growth of 21.7 percent between June 2019 and June 2020, the largest one-year increase in nearly 80 years. The large year-overyear increase in deposits occurred primarily in the first two quarters of 2020, and was likely driven by reactions of individuals, businesses, and U.S. fiscal and monetary authorities to the COVID-19 pandemic. Deposits increased the most for noncommunity banks, midsize banks, banks with a mortgage lending specialization, and offices in metropolitan counties. The number of bank offices declined for the 11th consecutive year but at a lower rate than in the previous three years. The relatively low rate of decline in the number of offices was influenced by a low rate of closures among offices acquired through mergers. Further, the number of noncommunity bank offices and offices in metropolitan counties declined at low rates from June 2019 to June 2020 compared to previous years.