This regular feature focuses on developments that affect the bank examination function. We welcome ideas for future columns. Readers are encouraged to e-mail suggestions to SupervisoryJournal@fdic.gov.

The FDIC encourages banks to lend to creditworthy small businesses, and Small Business Administration (SBA) loans provide an avenue for small business lending that is of interest to many institutions. To participate in SBA lending, lenders must be knowledgeable about the products, rules, and documentation specific to SBA loan programs. This article provides useful information that will help lenders successfully navigate the requirements related to underwriting, servicing, and selling SBA loans.

In the wake of the financial crisis, community banks are looking for ways to stabilize and increase revenue and expand lending opportunities to small businesses to help reinvigorate local economies. As a result, interest in Small Business Administration (SBA) lending programs is growing. Created in 1953, the SBA provides support to small businesses through entrepreneurial development, government contracting, advocacy, and access to capital. This article provides information that may be of use to bankers involved in SBA lending and examiners involved in reviewing these activities.

Small businesses are a critical driver in the U. S. economy and access to credit is an important component to support their operations. However, these firms often lack sufficient collateral to pledge or require longer repayment periods on loans than most lenders can prudently provide. The federal banking agencies recognize the importance of credit availability to creditworthy small businesses and other borrowers, and have issued industry guidance to encourage prudent lending.1

Addressing the current credit needs of local communities, combined with a goal by some institutions to reduce reliance on higher-risk land development and speculative single-family residential construction lending, have made commercial and industrial (C&I) lending - particularly to small businesses - increasingly attractive to smaller institutions. However, for some community banks, increasing C&I lending can present challenges to loan officers unfamiliar with this business line and can heighten the risk of loss to a bank’s portfolio.

SBA lending, traditionally focused on C&I lending, offers a wide range of products and requires specialized expertise to manage the risks and minimize potential losses. SBA products are intended to minimize the risk and increase the profitability of small-business loans by encouraging lenders to loan against lower collateral values and offer longer repayment periods. The SBA guaranty, while an attractive feature, is conditional,2 and a lender’s ability to obtain the guaranty is subject to specific rules requiring considerable documentation (referred to henceforth as “The Rules”).3 This article focuses on the SBA products lenders most often use and the requirements for underwriting, servicing, risk grading, liquidating, and selling SBA loans.

SBA Lending Products

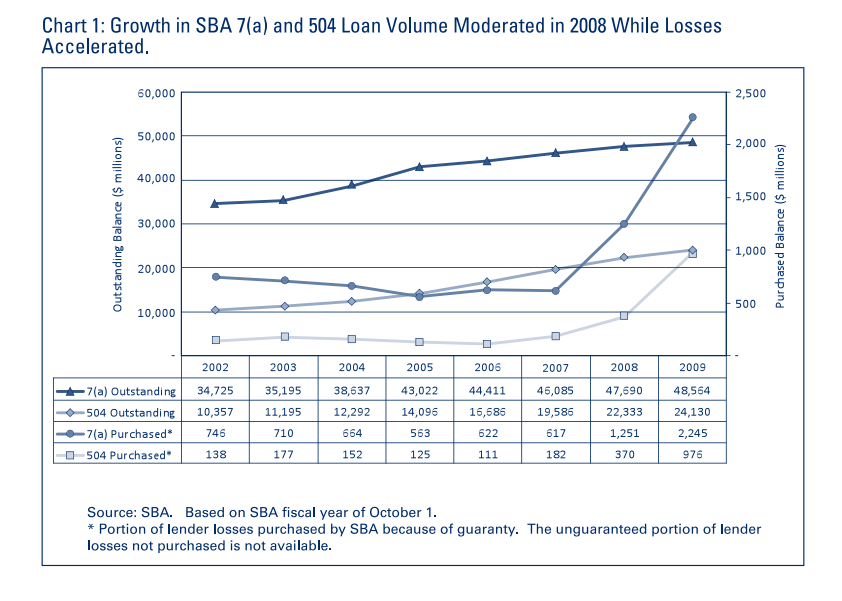

The SBA is well known for the guaranty programs it administers, including 504 and 7(a) programs. (See Chart 1 for information on the volume of 504 and 7(a) loans outstanding since 2002.) The 504 Loan Program provides small businesses with long-term financing to acquire major fixed assets, such as real estate, machinery, and equipment. Typically, lenders will finance 50 percent of the acquisition with a senior lien. The business will provide at least 10 percent equity and the remaining balance is financed by a Certified Development Company (CDC) with a second lien. A CDC is a private, nonprofit corporation that contributes to local economic development. The CDC receives funding from a debenture that is 100 percent guaranteed by the SBA. The advantage under this program is that the CDC portion is a fixed, below market rate loan for 20 years.

The 7(a) Loan Program features a range of products, including standard, special-purpose, express, export, and rural business loans. These loans are funded by lenders and conditionally guaranteed by the SBA. Banks participate in 7(a) Loan Programs as a regular, certified, preferred, SBAExpress, or Patriot Express lender and must submit applications to the SBA to receive approval for these designations. Each designation provides lenders with varying degrees of authority and responsibility. The preferred, SBAExpress, and Patriot Express designations allow lenders to make loan approval decisions without prior review by the SBA; lenders must be approved for these designations every two years. The SBA makes all loan approval decisions under the regular and certified designations. The most widely used 7(a) programs are standard and SBAExpress loans.

As of May 2011, Standard 7(a) program loans are for a maximum of $5,000,000 with a guaranty of no more than $3,750,000 or 75 percent of the loan amount. Standard loan terms can be up to 25 years for real estate, up to 10 years for equipment, and up to 7 years for working capital.4 Interest rates are based on published indices as well as the size and maturity of the loan.

The SBA Express program features an accelerated loan approval process. As of May 2011, the guaranty is 50 percent of the loan amount, and the maximum loan is $1,000,000.5 The advantage is that lenders can use their own closing documents – rather than SBA closing documents – which saves time and expense. This program also allows lenders to fund lines of credit up to 7 years, which is not allowed under the standard program.

Requirements for underwriting, servicing, risk grading, and liquidating SBA loans often differ from those for conventional lending programs. As a result, lenders should identify and understand these requirements and develop an SBA lending program that includes opportunities for ongoing training.

Underwriting SBA Loans

The 7(a) Program is primarily designed to support loans that have a reasonable assurance of timely repayment but that may have weaker collateral protection. The Rules state the underwriting requirements, including:

Lenders must analyze each application in a commercially reasonable manner, consistent with prudent lending standards. On SBA-guaranteed loans, the cash flow of the Small Business Applicant is the primary source of repayment, not the liquidation of collateral. Thus, if the lender’s financial analysis demonstrates that the Small Business Applicant lacks reasonable assurance of repayment in a timely manner from the cash flow of the business, the loan request must be declined, regardless of the collateral available. (SOP 50 10 5 (C), Chapter 4. See https://www.sba.gov/partners/lenders).

For example, a dentist may need working capital to open a practice. Based on a feasible business plan,6 the cash flow for the practice may be acceptable, but only limited collateral may be available for protection. In this case, a lender may seek a guaranty to bolster collateral protection. In short, the guaranty does not make a risky loan viable and should not induce a lender to make a risky loan.

The Rules also outline the information required in a credit approval memorandum. The minimum requirements include:

- A discussion of the owners’ and managers’ relevant experience in the type of business, as well as their personal credit histories.

- A financial analysis of repayment ability based on historical income statements and/or tax returns (if an existing business) and projections, including the reasonableness of the supporting assumptions.

- A site visit consistent with the lender’s internal policy for similarly sized non-SBA guaranteed commercial loans. (See also Chapter 2, Paragraph IV.H.7.a)(2) of this Subpart and Paragraph II.C.4 of this Chapter.) (SOP 50 10 5(C), Chapter 4. See https://www.sba.gov/partners/lenders).

If these requirements are not included in a lender’s underwriting practices, the guaranty may be jeopardized, increasing the overall risk of the portfolio.

Following approval of the loan, the SBA provides a Loan Authorization to the lender. The Loan Authorization states the terms and conditions of the SBA’s guaranty, including the required structure, collateral, terms, lien position and disbursement of funds. The lender is responsible for closing the loan in compliance with the Loan Authorization; not doing so may place the guaranty at risk.

Lenders must disburse the loan proceeds in accordance with the Loan Authorization and document each disbursement. The documentation must contain sufficient detail for the SBA to determine:

- The recipient of each disbursement;

- The date and amount of each disbursement;

- The purpose of each disbursement; and

- Evidence to support disbursements, such as cancelled checks or paid receipts, to ensure that the borrower used loan proceeds for purposes stated in the Authorization. (SOP 50 10 5(C), Chapter 7. See https://www.sba.gov/partners/lenders).

The underwriting process includes critical steps which lenders must follow, including verifying the eligibility of a business, scrutinizing cash-flow projections, verifying the borrower’s and guarantor’s statement of personal history, obtaining all available collateral, and properly documenting and funding disbursements.7 In addition, the underwriting process will benefit from the incorporation of these best practices: using SBA documentation software, centralizing the documentation preparation process, creating documentation checklists and credit approval reports specific to SBA lending, using attorneys with SBA experience for closings, and centralizing documentation review after closings.

Servicing SBA Loans

Once a loan is closed and disbursed, lenders must service 7(a) loans as carefully as they would the non-SBA portfolio. For example, throughout the life of a loan, lenders must ensure that documents requiring periodic renewals, such as hazard insurance and Uniform Commercial Code (UCC) -1 financing statements,8 remain current. A lender is also required to submit a report to Colson Services Corp. (Colson Report) every month.9 The Colson Report includes information about the next due date, status of the loan, undisbursed loan amount, guaranteed portion of principal and interest received, and the guaranteed portion of the outstanding balance.

Lenders can modify terms by extending maturities, implementing interest-only periods, and releasing collateral. The SBA encourages lenders to work with borrowers as concessions generally are within the framework of The Rules. However, certain modifications require the SBA’s approval. If a concession is granted because of a borrower’s financial difficulties, the modified loan would be a troubled debt restructuring that should be appropriately accounted for and disclosed based on outstanding guidance for such restructurings, including the measurement of impairment under Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 310, Receivables (formerly FASB Statement No. 114, “Accounting by Creditors for Impairment of a Loan”), and nonaccrual treatment. Small-business loans are not predominantly collateral dependent; as a result, impairment calculations should be consistent with the present value methodology.10 In cases where the loan book value (Call Report balance) and the customer balance (contractual obligation) are different, lenders are required to report the customer balance in the Colson Report.

Common servicing missteps on SBA loans include not renewing appropriate documents, releasing collateral without prior SBA approval (when required), modifying credits inappropriately, or incorrectly assuming that the existence of the guaranty means that problem credits need not be reported as such. As with non-SBA loans, lenders should collect and analyze annual financial statements and consider incorporating the following best practices into their servicing processes and procedures: using SBA documentation software for the Colson Report, referring to the SBA Servicing and Liquidation Actions 7(a) Lender Matrix11 before making any modifications, and documenting the reasons for any modifications in the credit files.

Risk Grades for SBA Loans

Lenders should risk grade the SBA portfolio using the same metrics applied to the non-SBA portfolio. SBA loans will tend to fall into higher-risk grade categories because of the longer amortizations, weak collateral protection, and general volatility12 given that the majority of these loans are for less-established businesses. Lenders may mistakenly rely on the guaranty in assigning a lower risk grade to a higher-risk loan. Lenders must keep in mind that risk grades should reflect the underlying risk of SBA loans without consideration of the guaranty.

If adverse classification is warranted, examiners should consider the extent of the protection provided by the guaranty when determining the portion to be classified. If no deficiencies are identified with the underwriting, servicing, or liquidation documentation, adverse classifications generally will be limited to the unguaranteed portion. However, if deficiencies are identified, the guaranty is put at risk for reduction or denial by the SBA, and examiners should consider adversely classifying the entire loan.

Liquidation of Collateral

Lenders should make every effort to work with borrowers before considering liquidation of collateral. When a business fails, the lender is responsible for documenting the liquidation of collateral for the highest possible recovery. This includes allowing the borrower to liquidate collateral for the lender,13 or the lender taking possession to liquidate. If a loss14 exists, the lender must file a 10 Tab package for the SBA to purchase the unpaid principal amount of the guaranteed portion of the loan; this package requires certain underwriting, servicing, and liquidation documentation.15 (See Chart 1 for information on the volume of guarantees purchased by the SBA since 2002.)

If the lender submits a complete 10 Tab package, the SBA generally will purchase the guaranteed portion within 45 business days. However, purchase of the guaranteed portion could take significantly longer if the 10 Tab package does not include all required information. As part of a SBA loan liquidation, lenders must conduct site visits, properly dispose of collateral, and accurately apply recoveries to SBA loans.16 In addition, lenders should consider centralizing the completion of the 10 Tab package, using the SBA Servicing and Liquidation Actions 7(a) Lender Matrix before liquidation, and documenting all actions during liquidation.

Losses Associated with SBA Lending

Lenders could incur additional losses on SBA loans if they do not carefully follow appropriate underwriting, servicing, and liquidating processes. If deficiencies are identified with these processes, the SBA determines the impact these deficiencies have on losses. Depending on the severity of the deficiency, the SBA has the option of repairing the guaranty, which occurs when the SBA discounts or reduces the amount of the guaranty. For example, if a lender fails to file a lien on equipment that is a small percentage of total collateral protection, the SBA will deduct the value of the equipment from the unpaid principal amount of the guaranteed portion of the loan it will be purchasing. However, if the deficiency is considered significant, the SBA will deny the guaranty. For example, if the borrower’s small business fails because the fire and the hazard insurance coverage had expired, the SBA will deny purchase. In many cases, the SBA may advise a bank to withdraw a 10 Tab package if a significant deficiency is identified, rather than formally denying the package.

Loan Sales

Following the origination of an SBA loan, lenders can hold loans to their maturity (hold model) or sell the guaranteed portion of loans to the secondary market (sale model). The hold model provides lenders with a long-term source of interest income. The sale model provides high levels of non-interest income but also requires high levels of loan originations.17

In the secondary market, guaranteed loans are liquid and command a premium. Investors buy these loans because the interest rates are generally high compared to the risk, as the only risk the investor incurs is prepayment risk. Loans with longer terms and higher yields realize higher premiums. The lender retains all servicing rights for sold loans and must follow the servicing requirements in The Rules. The lender receives a monthly minimum servicing fee of one percent on an annualized basis on the unpaid principal amount of the guaranteed portion of the loan that is sold at a premium. For example, for a hypothetical $1,000,000 loan originated with a 75 percent guaranty, the income might be broken down as follows:

Loan

1,000,000 x .75 = $750,000

Servicing Fee

$750,000 x .01 = $7,500 annually18

Premium

$750,000 x .10 = $75,000

The lender would realize $82,500 in the first year and $7,500 each subsequent year until the loan matures.19 Because the benefits of servicing typically are expected to more than adequately compensate the lender for performing servicing, the lender also books an intangible servicing asset and is required to value the servicing asset correctly.20 In many cases, the lender will rely on a consultant or accountant to provide quarterly valuations.

The sale model may be more prone to disruption or unexpected developments because of issues with loan restructurings and reliance on the level of originations. The secondary market is less receptive to loan modifications and restructurings because the SBA is required to repurchase the guaranteed portion of a loan after 60 days of non-payment.21 The secondary market would rather see the loan repurchased than concede interest income for an extended period of time as a result of a restructuring involving a reduction in the stated interest rate on the loan.

In addition, under the sale model, the amount of premium income a lender receives is based on the number of originations. As a result, to reach origination and premium income goals, lenders may relax underwriting standards or tie employee performance reviews and compensation to the number of originations without adequately considering risk. It is critical that lenders underwrite these loans as if they were planning to hold them and place emphasis on originating prudent loans when developing employee performance and compensation plans. Incentive compensation arrangements, in particular, should balance financial rewards to the employee with the long-term health of the institution.22

It is critical that examiners understand what to look for when reviewing SBA loan portfolios. The next section provides information examiners need to consider when evaluating a lender’s SBA program.

Reviewing an SBA Portfolio

Experience suggests examiners should consider the following areas when risk focusing a review of a bank’s SBA program:

- Review the lending policy. If involved in SBA lending, the institution must address this type of lending in its Lending Policy. The Policy could borrow language from or reference The Rules to help ensure all relevant areas are covered. The Policy should include the types of SBA programs in which the bank will engage, any asset limits on specific SBA programs, the normal trade area for SBA lending, and any credit concentration limitations.

- Review the internal risk-grade process. Evaluate how accurately management identifies and measures risks in SBA loans. To ensure lenders are not grading loans too highly because of the SBA guaranty, an internal loan review system specific to the SBA loan portfolio must be designed and implemented. This system should verify that initial grades are appropriate and any grade changes are made when needed. The risk grading system for SBA loans can be part of a lender’s overall internal loan review system, but should effectively capture the specific risks that SBA loans pose to the institution.

- Review ongoing training. The Rules are extensive and updated regularly. As a result, lenders should receive comprehensive training before engaging in SBA lending and enroll in ongoing training to remain current on any updates. Training is offered by the SBA, trade associations such as the National Association of Government Guaranteed Lenders (NAGGL),23 consultants, and attorneys.

- Review the SBA audit report. The SBA performs on-site audits for all lenders with $10 million or more in outstanding SBA loans. These audits are performed at least every two years and address portfolio performance, SBA management and operations, credit administration, and compliance. If a lender cannot provide a copy of the audit report, the examiner should contact the lender’s SBA District Office.

- Review the quarterly Lender Portal report. The SBA tracks various portfolio performance ratios, such as past-due, liquidation, and delinquency rates. Based on portfolio performance, the SBA assigns a Lender Risk Rating of “1” to “5” (“1” representing optimal performance). Lenders rated “1” are considered strong in every respect, a “2” rating is considered good, lenders rated “3” are considered average, a “4” rating is considered below average, and lenders rated “5” are considered well below average. All lenders have access to their Lender Portal report, but must first register on the SBA Web site at http://www.sba.gov/content/lender-portal-login. If a lender cannot provide a copy of the Lender Portal report, the examiner should contact the lender’s SBA District Office.

- Review the number of repairs, denials, and withdrawals of guarantees for the lender. This information should be available from the lender.

- Review for any industry credit concentrations. Examiners should perform more in-depth reviews of portfolios with high industry concentrations. Bank management should monitor credit concentrations by North American Industry Classification System (NAICS) codes, and this information should be made available to the examiner. Industries have different SBA failure rates and repurchase rates. For example, from October 1, 2000 to September 30, 2009, SBA loans to the veterinary services industry had the lowest combined failure and repurchase rates while the shellfish fishing industry ranked highest among the larger industries (see Chart 2 and Chart 3).24

- Review for general concentrations. In general, concentrations of credit add a dimension of risk that should be monitored, measured, and controlled by management. Common risk factors such as borrower affiliation, industry, and geographic location should be considered when assessing portfolio risk and establishing concentration limits. Excessive or unmonitored exposures would require heightened scrutiny during the examination process.

- Review the Loan Authorization of a credit. Evaluate how well management has documented the authorization requirements and determine if supporting documentation for disbursements satisfies the Loan Authorization. Weak practices in this area should be noted in examination findings.

Conclusion

SBA-guaranteed loans present opportunities for banks to expand their lending to small businesses. However, lending to small businesses, even with an SBA guaranty, is not without risk. Small disruptions in cash flow can significantly affect the viability of the business and, therefore, the performance of the loan. Small businesses that require SBA loan guarantees carry additional risk due to other weaknesses that may disqualify them from conventional lending, such as insufficient collateral and longer amortizations. Lenders must take particular care to understand the technical and detailed requirements for SBA underwriting, servicing, and liquidation processes.

In addition, loan risk grades should be determined without regard to the protection afforded by the SBA guaranty. Lenders should appropriately identify the risks in SBA loans and not assign unrealistic risk grades inconsistent with those assigned to non-SBA loans. The guaranty does not provide additional support for weaker cash flow loans, improve risk grades, or make risky loans viable.

Examiners’ review of SBA portfolios is intended to help ensure prompt identification of shortcomings or weaknesses in an institution’s SBA lending program. Together, examiners and lenders can work to correct and strengthen existing policies and procedures.

Ryan C. Senegal

Supervisory Examiner

rsenegal@fdic.gov

Bryan P. Stevens

Mr. Stevens was formerly a Loan Review Specialist with the FDIC.

1 Interagency Statement on Meeting the Credit Needs of Creditworthy Small Business Borrowers (FIL-5-2010, February 12, 2010, http://www.fdic.gov/news/news/financial/2010/fil10005.html) and Interagency Statement on Meeting the Needs of Creditworthy Borrowers (FIL-128-2008, November 12, 2008, http://www.fdic.gov/news/news/financial/2008/fil08128.html).

2 However, when the guaranteed portion of an SBA loan is transferred to an investor in the secondary market, the SBA’s guaranty becomes unconditional as it applies to the investor.

3 These requirements are outlined in Standard Operating Procedures (SOPs), official notices, and procedural guides for each program (referred to in this article collectively as “The Rules”). SOPs cover policies and procedures for all guaranteed lending program and include SOP 50 10 (Credit/Underwriting), SOP 50 50 (Servicing), and SOP 50 51 (Liquidation). Notices provide information or update policy and procedures. The Rules are very detailed, and lenders should check regularly for updates. The Rules are subject to change, and a guaranty is subject to The Rules outstanding at origination. If The Rules have been updated since origination, examiners should refer to The Rules outstanding at origination.

4 Terms are subject to change. For current terms, refer to the SBA Program Matrix at https://www.sba.gov/partners/lenders/7a-loan-program/terms-conditions-eligibility.

5 See footnote 4.

6 Lenders should scrutinize cash-flow projections and should not accept projections without analyzing the feasibility of the underlying assumptions.

7 Verifying the statement of personal history includes checking for prior tax liens, felony convictions, or defaults on any government debt, such as a student loan. Although the SBA will work with borrowers with limited collateral, it generally requires all available collateral be pledged to the loan. Disbursements include no funds to pay for purposes other than approved.

8 A lender must file UCC -1 financing statement to perfect the lender’s security interest in borrower assets. This document is in effect for five years unless a continuation statement is filed.

9 Colson Services Corp. provides loan payment accounting and servicing to the SBA.

10 If an impaired small-business loan is collateral dependent, impairment should be measured based on the fair value of the collateral.

11 The Matrix can be found at https://www.sba.gov/document/support--servicing-liquidation-actions-7a-lender-matrix.

12 Bureau of Labor Statistics data show that only 49 percent of establishments survive at least 5 years; 34 percent survive at least 10 years; and 26 percent survive 15 years or more. U.S. Small Business Administration, “Frequently Asked Questions”.

13 In these cases, the lender is required to inventory the collateral and conduct site visits every 90 days.

14 In addition to collateral shortfall, this includes 120 days of accrued interest and collections costs, such as reasonable attorney and appraisal fees.

15 The 10 Tab package was developed by the SBA and contains mandatory documentation for all guaranty purchases. If a borrower files for bankruptcy protection, the lender may file a 10 Tab package before liquidating all collateral. If a business fails within 18 months of the origination of the loan, the SBA requires that the lender submit all underwriting, servicing, and liquidation documentation.

16 In some cases, lenders will fund other non-SBA guaranteed loans and attempt to apply recoveries to these loans before the SBA loan with senior lien position.

17 For the purposes of this discussion of loan sales, transfers of guaranteed portions of SBA loans are presumed to be at a price in excess of par (i.e. at a premium) and to qualify for sale accounting as of the transfer date.

18 This assumes that the loan does not amortize and principal remains constant. In most cases, the unpaid principal amount would decline as the loan is repaid, so even in the first year the servicing fee would be less than $7,500.

19 See footnote 16.

20 A servicing asset is initially measured at fair value. Each class of servicing assets should be subsequently measured using either the amortization method (with quarterly assessments of impairment based on fair value) or the fair value measurement method. For further information, see FASB ASC Topic 860 and the Glossary entry for “Servicing Assets and Liabilities” in the Call Report instruction book.

21 Lenders retain responsibility for reimbursing the SBA for any repairs or denials on the loans repurchased.

22 Interagency Guidance on Sound Incentive Compensation Policies (FDIC Press Release 138-2010, June 21, 2010, http://www.fdic.gov/news/news/press/2010/pr10138.html).

23 NAGGL is the most prominent trade association for SBA lenders. For more information on this trade group’s activities, go to http://www.naggl.org.

24 Information from the 2010 NAICS Coleman Report. Larger industries have disbursed loan volumes that exceed the average during the period. For more information, go to http://www.colemanpublishing.com.