Managing interest rate risk (IRR) is one of the most important jobs of a banker. IRR can be a technical subject, but it deals with some of the most significant strategic and operational questions that banks face. When the economy or interest rates shift direction, how will that affect the bank’s deposit base, loan customers, and investments? Will revenue growth keep pace with rising deposit costs? Will there be sufficient deposit funding to meet increasing loan demand, or will potentially depreciated securities need to be sold for liquidity? Most importantly, does the bank need to change its strategy now to be better prepared for the future? While technical experts and IRR software can help answer such questions, senior management and the board of directors need to be actively engaged in IRR oversight to ensure that key strategic issues are carefully considered and addressed on a regular basis.

In the years since the financial crisis, some banks have extended their asset maturities to generate income in response to low market interest rates and a challenging earnings environment. As a result, these institutions’ earnings, equity capital, and liquidity could be adversely affected by a sustained and substantial increase in interest rates. Managing IRR is a central aspect of prudent banking, and in recent years the FDIC has re-emphasized the importance of effective policies, strong internal monitoring and control procedures, and appropriate risk mitigation strategies to appropriately manage rate sensitivity.1 Good planning now can help minimize the potential for negative impacts.

This article highlights the elements of a successful IRR management process through a discussion of supervisory expectations and observed practices at well-rated institutions. An overview of risk mitigation strategies is presented to illustrate that IRR can be appropriately managed through various prudential methods.

Governance and the Board of Directors

The 1996 Joint Agency Policy Statement on Interest Rate Risk (“the 1996 Policy Statement”) and the 2010 Advisory on Interest Rate Risk Management (“the 2010 Advisory”)2 state that the board of directors is ultimately responsible for the degree of IRR taken by an institution and should understand and monitor exposures that may potentially affect the institution’s financial condition. This does not mean that directors need to be well versed in the technical aspects of IRR mechanics and modeling, but a basic understanding of IRR commensurate with the institution’s activities is essential. Frequently, the recorded minutes of board and asset-liability management committee (ALCO) meetings at well-rated institutions include director comments or questions on matters that go beyond the current and prospective interest rate environment and include pricing strategies, product mix, and most notably, the rationale behind policy deviations and underlying causes of changes in the bank’s risk profile. IRR management from a director’s perspective is not about projecting how and when rates will change; instead, it is about understanding how the bank will be affected by a range of outcomes and ensuring that assumed risks are reasonable and properly compensated for. Such notations in the minutes portray an engaged and informed directorate that ensures its strategies are executed within established policy. Senior management’s primary objectives should be administering board-approved policies, including day-to-day oversight of risk taking; maintaining an effective IRR measurement system; and collecting and interpreting meaningful data to inform the directorate of exposure levels.

A clearly articulated asset-liability management policy with appropriate IRR guidelines ensures that IRR exposure is measured, reported, and maintained within tolerable parameters. The policy should establish clear lines of authority and responsibility; define allowable products, services, and activities; and include risk mitigation strategies. To prudently control rate sensitivity, written policies should require regular IRR measurement3 and meaningful risk limits.

Establishing Policy Limits: Setting the Board’s Tolerance for IRR

Examiners are sometimes asked, “What limits are reasonable for changes in net interest income (NII) or economic value of equity (EVE)?” Rules of thumb exist in the industry, but each bank is unique, and it is difficult to apply a uniform set of limits. In establishing limits, the board and senior management should focus on the potential impact of interest rate scenarios on net income and EVE, taking into consideration the effect on the value of the investment portfolio, the ability of the bank’s existing borrowers to repay their loans, and depositor behavior. The bank’s financial condition and risk profile should be the guiding factors that influence the level of tolerance the board mandates in setting limits. Limits should not be so low as to frequently require exception approval or refinement, and they should not be set so high as to allow for an unacceptable level of IRR. If established limits have been or are about to be breached, management should take mitigating steps to ensure that IRR is maintained within board-approved limits.

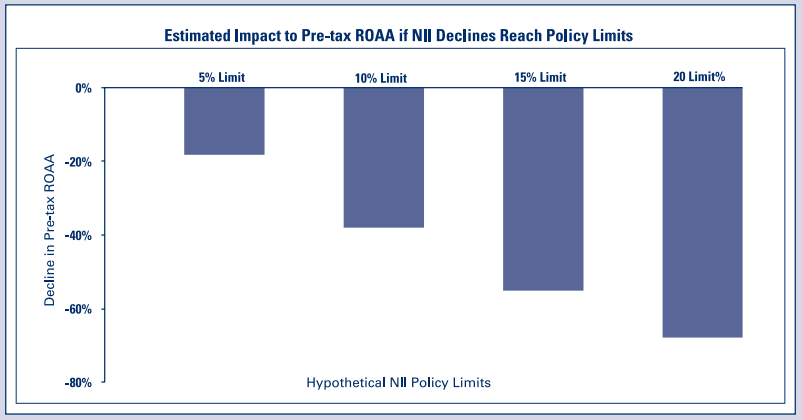

It is important for directors to consider what the limit is based on (for example, a 20 percent change in NII is different from a 20 percent change in ROAA). In the graph shown below, we can observe the impact to net income (vertical axis) if net interest income (horizontal axis) were to decline by as much as 20 percent. In this case, pre-tax ROAA would decline more than 60 percent through what may have been considered only a moderate and acceptable degree of NII exposure at 20 percent. In evaluating the appropriateness of 20 percent as a policy limit, the bank’s board should consider how it would address the potential for a pronounced decline in net income and weigh the impact and feasibility of those actions against the impact of lower policy limits For example, one approach may be to adjust asset growth expectations or raise additional capital given lower forecast earnings. Another approach might be to assess whether reductions could be made to overhead expenses. If these actions would not be feasible, or would be feasible but not desirable in light of the bank’s overall strategic plan, then the board should consider tightening the policy limits, which may require formal risk mitigation strategies (e.g., initiating changes in the maturity and re-pricing characteristics of assets or liabilities) as discussed in further detail later in this article. This example highlights the benefit of expanding policy limit considerations into a broader financial context.

The Role of the ALCO

Most financial institutions form an ALCO to coordinate balance sheet strategies, manage liquidity, and monitor IRR exposures. The 2010 Advisory describes an optimal ALCO structure, which includes representation from major operational functions (e.g., lending, deposit gathering, investing). The advantage of this structure is that each member has an extensive knowledge of product, market, and competitive dynamics in relation to IRR. Members are typically senior or mid-level managers4 who can convene quickly during evolving or challenging market environments to evaluate, analyze, and recommend mitigating action to the board.

In addition to asset-liability management oversight, one important function the ALCO can fulfill is the formulation and periodic review of the key assumptions5 the bank uses when analyzing its exposure to changes in interest rates. Examiners have observed instances where the assumptions are formulated by a member of management, commonly a Chief Financial Officer (CFO), and are presented for review and approval by the ALCO. This process is acceptable and can achieve desired results. The ALCO sometimes plays a more active role by providing and reviewing the underlying information and supporting rationale as the basis for assumption formulation. ALCO members at well-rated institutions are readily familiar with deposit and loan pricing and customer behavior in the bank’s local market, which provides the foundation for the critical assumptions requiring sound judgment, such as non-maturity deposit sensitivity and loan prepayment activity. This is not to say, for example, that an ALCO member from the lending function will know exact historical prepayment metrics on residential mortgages, but the member should have sufficient experience to be able to reasonably question an assumption under consideration.

Internal Controls and Independent Review

As with any well-governed banking function, an adequate system of internal controls promotes the integrity of the IRR management process. Clear lines of responsibility and authority should be communicated and exercised to ensure consistent monitoring, transparent reporting, and data integrity. For institutions that conduct in-house analysis with purchased software, strong controls over the IRR measurement process are important to ensure the accuracy and integrity of reports presented to the board

and senior management. Institutions with strong controls generally have, at minimum, software access restrictions, data and assumption input review procedures, board reports that include changes to assumptions, and identified staff to serve in a backup role when needed. Backup personnel should have a basic understanding of IRR including the bank’s policies and limits, and the ability to use the bank’s particular IRR measurement tools so as to ensure IRR measurement and reporting processes continue without interruption.

The 1996 Policy Statement states that banks should conduct an independent review of IRR measurement and control systems along with an annual report to the board that summarizes its findings. The board or ALCO should consider two critical questions when discussing independent review findings:

- Does the IRR management process function according to policy guidelines and prudent risk management standards?

- Does the IRR measurement system reasonably estimate exposures to earnings and capital based on a logical and supported set of assumptions?

The 1996 Policy Statement also states that the scope and formality of an independent review should be scaled to the complexity of a bank’s activities. Additional perspectives regarding the independent review process are presented in “Developing an In-House Independent Review of Interest Rate Risk Management Systems” in this edition of Supervisory Insights.

A more advanced facet of the IRR independent review involves methodological and mathematical testing of vendor-designed IRR models. The FDIC does not require state nonmember institutions6 to conduct this type of test, as vendors typically engage a credible third party to validate the integrity and reliability of their modeling software. Most model vendors have a sufficiently large client base to justify the expense of a third-party validation; therefore, it should be readily available at the client institution’s request. If not, the board should seek other alternatives to validate the model or reconsider whether the vendor is suitable for its institution.

Although most community banks are not required to validate purchased IRR software, bank management is responsible for ensuring that the key assumptions entered into the software are reasonable, forward-looking, and appropriate to the bank’s operations. For example, in one case, bank management observed that its IRR software was forecasting interest expense from non-maturity deposits in a rising-rate environment at a level that was materially lower than the bank’s prior experience. Upon recognition of this difference, bank management determined that deposit pricing had increased at a greater rate than projected due to its decision to match a competitor’s aggressive marketing campaign to attract new depositors when short-term rates began to increase. Based on the likelihood of the competitor continuing the marketing strategy, the bank altered its non-maturity deposit rate sensitivity assumptions to better reflect its plan to retain valuable core depositors.

Risk Mitigation Strategies

Risk mitigation is an ongoing process to maintain exposures within board approved limits to ensure that earnings and capital are sufficient to allow the bank to withstand adverse interest rate changes. There are a range of strategies available should current exposures be outside comfort levels. Risk mitigation can be as simple as reducing the maturities of future purchases of investment securities or extending the duration of liabilities. Well-rated institutions use several methods to reduce IRR exposure, including repositioning the balance sheet and hedging. Strong capital levels or a new capital offering also can be a very effective tool for mitigating outsized IRR exposure.

The most common risk mitigation strategy is slowly repositioning the balance sheet over time to more consistently align an institution’s over-all re-pricing, maturity, and duration profile.7 When prudently conducted, this approach can help provide a “natural hedge,” whereby an institution that was previously mismatched with respect to cash-flow timing or valuation returns to a more neutral rate sensitivity position. For example, an institution exposed to rising interest rates may need to shorten the duration of assets or extend the duration of liabilities.

Before engaging in a balance sheet repositioning program, institutions should analyze the impact on prospective earnings and capital. Generally, the rapid sale of illiquid long-duration securities could result in significant losses and may not be an optimal method to reduce risk. When banks find they possess a higher level of IRR than desired, an appropriate action may be to purchase shorter-dated securities as funding becomes available or increase the duration of funding.

Reducing extension risk in the bond portfolio often involves accepting a lower level of current earnings. Accepting additional risk is typically rewarded through a higher return, and IRR is no different in this context. Therefore, some level of IRR can be beneficial, in moderation. However, banks that are working to reduce their IRR exposure will also likely see a reduction in their interest income as a result. The FDIC strongly supports banks’ efforts to control outsized exposure to interest rate volatility and will not criticize an institution for temporary adverse consequences to earnings resulting from a prudent rebalancing strategy.

A secondary, though more complex, IRR mitigation technique is offbalance sheet hedging. Hedging strategies for IRR typically involve the use of derivative instruments (e.g., forwards, swaps, caps, floors, swaptions, and collars)8 and can be effective in curtailing undue IRR if used in a safe and sound manner. As discussed in the 2010 Advisory, the primary caveat to consider before entering into a derivatives-based hedging strategy is determining whether the board and senior management can develop an appropriate understanding of the proposed hedging strategy and consider its relevant risks and benefits based on a comprehensive, reliable analysis. If derivatives hedging is determined to be an appropriate tool for a given institution, the board and senior management should develop a thorough set of policies and procedures covering allowable derivatives contracts, risk and maximum loss limitations in terms of capital,9 pre-purchase analysis (including modeling) and ongoing monitoring procedures, authorized transactional parties, and accounting standards.10

Importantly, hedging with derivatives involves a new set of IRR measurement considerations before and after entering into such a contract, as well as assumptions that would require sufficient modeling capabilities. As a general matter, community banks should carefully consider their ability to identify and manage the associated risks before embarking on a derivatives hedging program.

Consequences of Unexpected Market Volatility on IRR Sensitivity

Implementing the elements of a strong IRR governance and risk management framework enables banks to effectively manage exposures and prepare their business for the future. Nonetheless, even when risk is well managed, an institution could be negatively impacted by unexpected interest rate volatility or other adverse circumstances.

An institution that has extended the duration of its fixed-rate assets to generate additional income, for example, may experience a negative impact to earnings in a higher-interest rate environment as funding costs increase. While a strong retail deposit base can generally help mitigate the impact of such a situation, it is important to recognize that depositors may be more aggressive in seeking higher-yielding products than previous experience. Of particular note, traditionally stable deposits could behave with greater rate sensitivity as a result of structural, technological, and preferential changes that were not present the last time rates increased after a sustained low-rate environment. Furthermore, to the extent an institution has experienced significant deposit growth over the last several years, some deposit balances may be withdrawn from the institution altogether and need to be replaced with higher-cost deposits or wholesale funding.

Institutions that have lengthened the duration of their investment portfolios could experience liquidity constraints if rapidly rising interest rates cause significant depreciation in the value of those securities. For example, liquidity could be severely constrained if an institution relies on marketable securities as a primary or secondary source of funding. Moreover, existing secured borrowings may require a pledge of additional collateral to address the reduction in the securities’ value. An institution could likely borrow against unencumbered depreciated securities at an increased margin, but only if lenders are willing to extend credit on reasonable terms. This liquidity stress could accelerate if deposit balances were to leave the institution altogether or creditors were to reduce or eliminate lines of credit.

While regulatory capital measures (for Prompt Corrective Action purposes) for most community banks will generally be unaffected by securities depreciation,11 equity capital under U.S. generally accepted accounting principles (GAAP) can be compromised. Low or negative equity capital can produce negative perceptions of an institution’s financial strength in the eyes of depositors, shareholders, correspondents, and the general public, which could ultimately affect the bank in many areas. If significant depreciation in securities portfolios diminished equity capital to low or negative levels, correspondents and other counterparties could resist requests for credit or require onerous terms. Furthermore, depositors, deposit listing services, and deposit brokers would need to decide how the bank’s GAAP equity position should affect their willingness to continue placing deposits. Accordingly, contingency funding plans should fully and realistically address the potential for reduced borrowing capacity that may be caused by depreciation in long-duration securities and present strategies which ensure prudent levels of liquidity. To avoid the consequences of rising interest rates on long-duration securities portfolios, it may be advisable for certain institutions to rebalance their holdings to a more appropriate position before rate volatility occurs.

Banks should understand these and other implications when establishing their desired level of IRR and have plans for dealing with unexpected market volatility and funding issues that can arise.

Conclusion

An effective governance process for IRR is a fundamental aspect of a strong risk management framework. A board and senior management team that administer effective policies and are well informed can better position their bank to sustain profitability and preserve capital as the interest rate environment changes.

Lucas McKibben

Senior Financial Institution Examiner

Lexington, KY Field Office

Division of Risk Management Supervision

lmckibben@fdic.gov

The author thanks Frank Hughes, Senior Examination Specialist, for his contributions to this article.

1 Managing Sensitivity to Market Risk in a Challenging Interest Rate Environment, FDIC Financial Institution Letter FIL-46-2013, October 8, 2013, http://www.fdic.gov/news/news/financial/2013/fil13046.html.

2 Joint Agency Policy Statement on Interest Rate Risk, FDIC, Board of Governors of the Federal Reserve Board, and the Office of the Comptroller of the Currency, May 14, 1996, http://www.fdic.gov/regulations/laws/rules/5000-4200.html and the Advisory on Interest Rate Risk Management, FFIEC, January 7, 2010, http://www.ffiec.gov/press/pr010710.htm.

3 According to the 1996 Policy Statement, senior management and the board or board committee should review reports on the bank’s IRR profile at least quarterly. More frequent reporting is often warranted.

4 Examiners also have observed ALCO membership that includes directors, which provides the board with practical insight into the bank’s risk-taking practices and mitigation strategies.

5 The 1996 Policy Statement recommends, as part of the independent review, the identification of critical assumptions, an analysis of the assumption process, and an assessment of the impact of chosen assumptions. However, fulfilling this requirement should not preclude the ALCO from conducting periodic reviews, which can reasonably assure the model generates exposures based on current and relevant assumptions. The 2010 Advisory states that proper measurement of IRR requires regularly assessing the reasonableness of assumptions that underlie an institution’s IRR exposure estimates. At well-rated institutions, examiners have generally observed that assumption reviews are conducted quarterly before each model run.

6 According to the 2010 Advisory, large and complex institutions may need to conduct in-depth analysis of a model’s underlying mathematics. Such analysis could take the form of constructing an identical model to test assumptions and outcomes or using an existing, well-validated “benchmark” model, which is typically a less costly alternative. Underpinning methodologies in a benchmark model should be closely aligned to those of the model being validated.

7 Duration is a measure of a financial instrument’s value sensitivity to changes in interest rates. Variations of this approach are common to the measurement of EVE in many IRR models.

8 As described in the 2010 Advisory, hedging with derivative instruments to mitigate IRR may be appropriate for institutions with the requisite knowledge and expertise, as it is a potentially complex activity that can have unintended consequences, including compounding losses.

9 Risk limitations commonly include, at a minimum, position limits, maturity parameters and counterparty credit guidelines. Counterparty credit guidance becomes more critical for those institutions with over-the-counter contracts given the increased credit risk associated with these instruments.

10 Accounting standards for derivatives and hedging are set forth in Accounting Standards Codification Topic 815 – “Derivatives and Hedging.”

11 Under the current general risk-based capital rules, most components of accumulated other comprehensive income (AOCI) are not reflected in a banking organization’s regulatory capital. Under the Basel III capital rules, all banking organizations must recognize in regulatory capital all components of AOCI, excluding accumulated net gains and losses on cash-flow hedges that relate to the hedging of items that are not recognized at fair value on the balance sheet. Banking organizations, other than advanced approaches banking organizations, will be ableto make a one-time election to opt out of this treatment and continue to neutralize changes in AOCI, as is done under the current capital rules. Institutions are reminded that the one-time election provided to non-advanced approaches banking organizations must be made with the filing of the March 31, 2015 Call Report. Recognition of changes to AOCI within capital calculations will start in 2015 for non-advanced approaches banking organizations that did not opt out of the Basel III treatment.