Section One:

Overview of privacy rule requirements

The privacy rule governs when and how banks may share nonpublic personal information about consumers with nonaffiliated third parties.

The rule embodies two principles - notice and opt out. In summary:

- All banks must develop initial and annual privacy notices. The notices must describe in general terms the bank's information sharing practices.

- Banks that share nonpublic personal information about consumers with nonaffiliated third parties (outside of opt out exceptions delineated in the privacy rule) must also provide consumers with:

- an opt out notice

- a reasonable period of time for the consumer to opt out

A few key terms used throughout the privacy rule are critical to understanding the rule's scope and application. Refer to Section Four of this guide for an explanation of:

- nonpublic personal information

- the distinction between consumers and customers

- nonaffiliated third party

Exceptions to opt out: A consumer cannot opt out of all information sharing. First, the privacy rule does not govern information sharing among affiliated parties. Second, the rule contains exceptions to allow transfers of nonpublic personal information to unaffiliated parties to process and service a consumer's transaction, and to facilitate other normal business transactions. For example, consumers cannot opt out when nonpublic personal information is shared with a nonaffiliated third party to:

- market the bank's own financial products or services

- market financial products or services offered by the bank and another financial institution (joint marketing)

- process and service transactions the consumer requests or authorizes

- protect against potential fraud or unauthorized transactions

- respond to judicial process

- comply with federal, state, or local legal requirements

Prohibition on sharing account numbers: The privacy rule prohibits a bank from disclosing an account number or access code for credit card, deposit, or transaction accounts to any nonaffiliated third party for use in marketing. The rule contains two narrow exceptions to this general prohibition. A bank may share account numbers in conjunction with marketing its own products as long as the service provider is not authorized to directly initiate charges to the accounts. A bank may also disclose account numbers to a participant in a private label or affinity credit card program when the participants are identified to the customer. An account number does not include a number or code in encrypted form as long as the bank does not also provide a means to decode the number.

Limits on reuse and redisclosure: The privacy rule limits reuse and redisclosure of nonpublic personal information received from a nonaffiliated financial institution or disclosed to a nonaffiliated third party. The specific limitations depend on whether the information was received pursuant to or outside of the notice and opt out exceptions.

State Law: A provision under a State law that provides greater consumer protection than provided under the GLBA privacy provisions will supercede the Federal privacy rule. The bank will be obligated to comply with the provisions of that State law to the extent those provisions provide greater consumer protection than the Federal privacy rule. The Federal Trade Commission determines whether a particular State law provides greater protection.

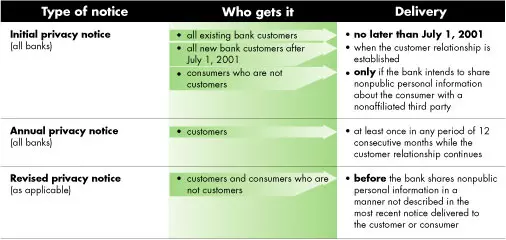

Content of notices: The initial, annual, and revised notices include, as applicable:

- categories of information a bank collects (all banks)

- categories of information a bank may disclose (all banks, except a bank that does not intend to make any disclosures or only makes disclosures under the exceptions may simply state that)

- categories of affiliates and nonaffiliates to whom a bank discloses nonpublic personal information (all banks sharing nonpublic personal information with an affiliate or with a nonaffiliated third party)

- information sharing practices about former customers (all banks)

- categories of information disclosed under the service provider/joint marketing exception (only those banks relying on this exception)

- consumer's right to opt out (only those banks that disclose outside of exceptions)

- disclosures made under the Fair Credit Reporting Act (only those banks providing the FCRA opt out notice)

- disclosures about confidentiality and security of information (all banks)

A revised notice may be required when a bank changes its information sharing practices.

The following table reflects the rule's requirements for delivering initial, annual, and revised notices to consumers and customers.

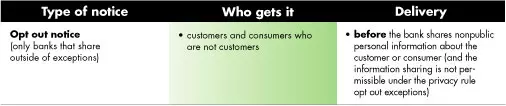

Opt Out Notice

The final rule provides that an opt out notice is adequate if it:

- identifies all the categories of nonpublic personal information the bank intends to disclose to nonaffiliated third parties

- states the consumer can opt out of the disclosure

- provides a reasonable method for the consumer to opt out, such as a toll-free telephone number

The table below summarizes the rule's requirements for delivering an opt out notice.

The opt out right: If a bank intends to share nonpublic personal information outside the exceptions, it must also:

- provide consumers with a reasonable opportunity to opt out. Examples in the privacy rule give consumers 30 days to respond to the opt out notice when the bank delivers the notice by mail or electronically

- comply with a consumer's opt out direction as soon as reasonably practicable when the direction is received after the initial opt out period elapses

- comply with the opt out direction until revoked in writing by the consumer

Delivering notices: The initial, annual, revised, and opt out notices may be delivered in writing or, if the consumer agrees, electronically. An oral description of the notice is not sufficient.

Section Two

Section Two has been rescinded. It related to preparations for the compliance deadline for privacy rules, which was July 1, 2001, and is therefore no longer relevant.

Section Three:

Maintaining Compliance Beyond

July 1, 2001

The following activities can help a bank achieve and maintain compliance with the privacy rule.

- Develop controls to monitor ongoing compliance. Consider mechanisms for monitoring:

- delivery of initial and annual notices to customers

- delivery of initial notice to consumers who are not customers, if applicable

- compliance with opt out directions, if applicable

- accuracy of privacy notices, including prior approval for:

- new marketing arrangements

- new or renewed vendor contracts

- disclosure of account numbers

- affiliate-referral programs

- reuse of consumer information received from another financial institution

- Train employees. All employees should understand the bank's policies and procedures for complying with the privacy rule. Some employees will need to be able to explain the bank's privacy policies to customers and to businesses providing services to the bank.

- Audit for compliance. Periodic audits will help management assess risk and verify the effectiveness of the compliance program. The Federal Financial Institutions Examination Council (FFIEC) will release interagency privacy examination procedures before July 1, 2001. The exam procedures will be a useful tool in developing a privacy audit program.

The interagency exam procedures will be mailed directly to insured depository institutions as soon as they are finalized. The procedures will also be available on the FDIC's Web site at www.fdic.gov when complete.

Section Four:

Learn the Lingo

Learning the lingo will help you understand and comply with the privacy rule. This section provides an explanation of key terminology.

Who must comply with the FDIC's privacy rule?

The FDIC's privacy rule refers to financial institutions that must comply with the rule as "you." For example, when the rule states that "you must provide a notice" it means all entities subject to this rule must provide a notice. The following definition of "you" explains the types of entities subject to the rule:

You: The banks that must comply with the FDIC's rule are -

- FDIC-supervised banks

- insured state branches of foreign banks

- subsidiaries of FDIC-supervised banks and insured state branches of foreign banks, with certain exceptions, such as insurance and securities or brokerage subsidiaries

Although the FDIC's rule only applies to certain banks and some of their subsidiaries, all financial institutions must comply with similar privacy rules adopted by their supervisory agencies. For example, although securities subsidiaries of FDIC-supervised banks do not have to comply with the FDIC's privacy rule, they do have to comply with a similar privacy rule adopted by the Securities and Exchange Commission.

Who is protected by the privacy rule?

The privacy rule protects "consumers." All consumers receive the same privacy protections.

However, a subset of consumers defined as customers must receive certain disclosures, such as an annual privacy notice, that need not be provided to consumers who are not customers.

Thus, it is important to know the distinction between consumers and customers to understand the different disclosure requirements under the privacy rule.

Consumer: Any individual who is seeking to obtain or has obtained a financial product or service from a bank for personal, family, or household purposes is a consumer of that bank. The definition of consumer includes individuals who:

- apply for a financial product or service (e.g., a loan or a deposit account) for personal, family, or household purposes

- actually obtain a financial product or service (e.g., a loan or a deposit account) for personal, family, or household purposes

Customer: As the following diagram reflects, customers are a subset of consumers. A customer is a consumer with whom a bank has a continuing relationship. Although the rule does not define "continuing relationship," it provides examples of transactions that are and are not considered continuing relationships. Consumers who have a deposit account, obtain a loan, or obtain an investment advisory service are considered customers. See Section 332.3(i).

Additional guidance regarding the customer relationship can be found in the Supplemental Information (the preamble) of the rule, which notes that a continuing relationship is established "where a consumer typically would receive some measure of continued service following, or in connection with, a transaction." See page 35168, Federal Register, Vol. 65, No. 106.

The next diagram depicts the relationship between all individuals who do business with a bank and those who meet the regulatory definitions for consumers and customers. As the diagram shows, only a portion of the individuals who conduct business with a bank are consumers under the privacy rule. For example, individuals are not considered consumers under this rule if they are commercial clients, grantors or beneficiaries of trusts for which the bank is trustee, or participants in an employee benefit plan that the banks sponsors.

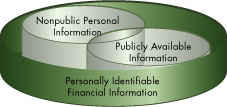

What type of information is protected by the privacy rule?

The rule identifies three primary categories of information:

- publicly available information

- personally identifiable financial information

- nonpublic personal information

Nonpublic personal information is the category of information protected by the privacy rule. The definitions for publicly available information and personally identifiable financial information work together to describe and define nonpublic personal information.

- Publicly available information is any information a bank reasonably believes is lawfully publicly available. The nature of the information, not the source of the information, determines whether it is publicly available information for purposes of the privacy rule. For example, even if a bank obtains customers' telephone numbers or the assessed value of their residences directly from the consumers, this information will be considered publicly available if the bank has a reasonable basis to believe the information could have been lawfully obtained from a public source. A reasonable belief exists if a bank has determined that (a) the information is of the type that is generally available to the public and (b) the individual has not blocked such information from public disclosure. This means, for example, that a bank can consider a customer's phone number to be publicly available, but only if the bank takes steps to determine the phone number is not unlisted.

- Personally identifiable financial information is any information a bank collects about a consumer in conjunction with providing a financial product or service. This includes:

- information provided by the consumer during the application process (e.g., name, phone number, address, income)

- information resulting from the financial product or service transaction (e.g., payment history, loan or deposit balances, credit card purchases)

- information from other sources about the consumer obtained in connection with providing the financial product or service (e.g., information from a consumer credit report or from court records)

Personally identifiable financial information also includes any information that "is disclosed in a manner that indicates that the individual is or has been your consumer." See Section 332.3(o)(2)(i)(D). Thus, the very fact that an individual is a consumer of a bank is personally identifiable financial information.

- Nonpublic personal information, the category of information protected by the privacy rule, consists of:

- Personally identifiable financial information that is not publicly available information; and

- Lists, descriptions, or other groupings of consumers that were either

- created using personally identifiable financial information that is not publicly available information, or

- contain personally identifiable financial information that is not publicly available information.

A list is considered nonpublic personal information if it is generated based on customer relationships, loan balances, or other personally identifiable financial information that is not publicly available. A list is also considered nonpublic personal information if it contains any nonpublic personal information.

For example, in jurisdictions where mortgage documents are public records, the names and address of all individuals for whom a bank held a mortgage would not be nonpublic personal information since it was generated using publicly available information and contained only publicly available information. The list would become nonpublic personal information, however, if it contained current loan balances or if it was generated using only those customers with current mortgage loan balances in excess of a certain amount.

The two categories of nonpublic personal information are depicted in the following diagram.

Who are nonaffiliated third parties?

The privacy rule restricts information sharing with nonaffiliated third parties. The rule defines nonaffiliated third parties as persons or entities except affiliates and persons jointly employed by a bank and a nonaffiliated third party. Affiliates generally include a bank's subsidiaries, its holding company, and any other subsidiaries of the holding company. See Section 332.3(a), Section 332.3(d), and Section 332.3(g).

The privacy rule does not impose limitations on information sharing with affiliates. It does, however, require disclosure of such information sharing policies and practices. (Note: The rules governing the sharing of information between a bank and its affiliates are set forth in the Fair Credit Reporting Act.)

Although the privacy rule most commonly uses the term "nonaffiliated third parties," there are some instances in which a distinction is made between nonaffiliated financial institutions and all other nonaffiliated third parties. Readers should pay particular attention to these distinctions. See Section 332.13.