SCROLL

June 16, 2023

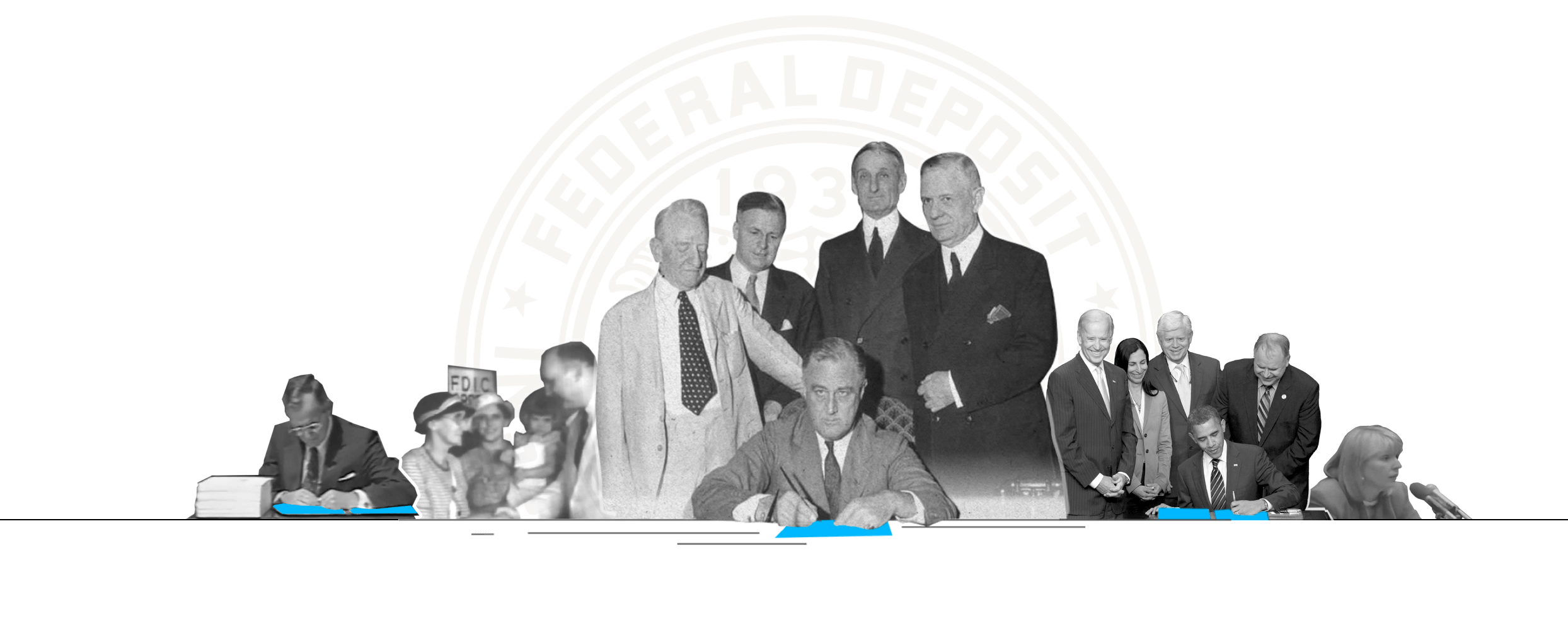

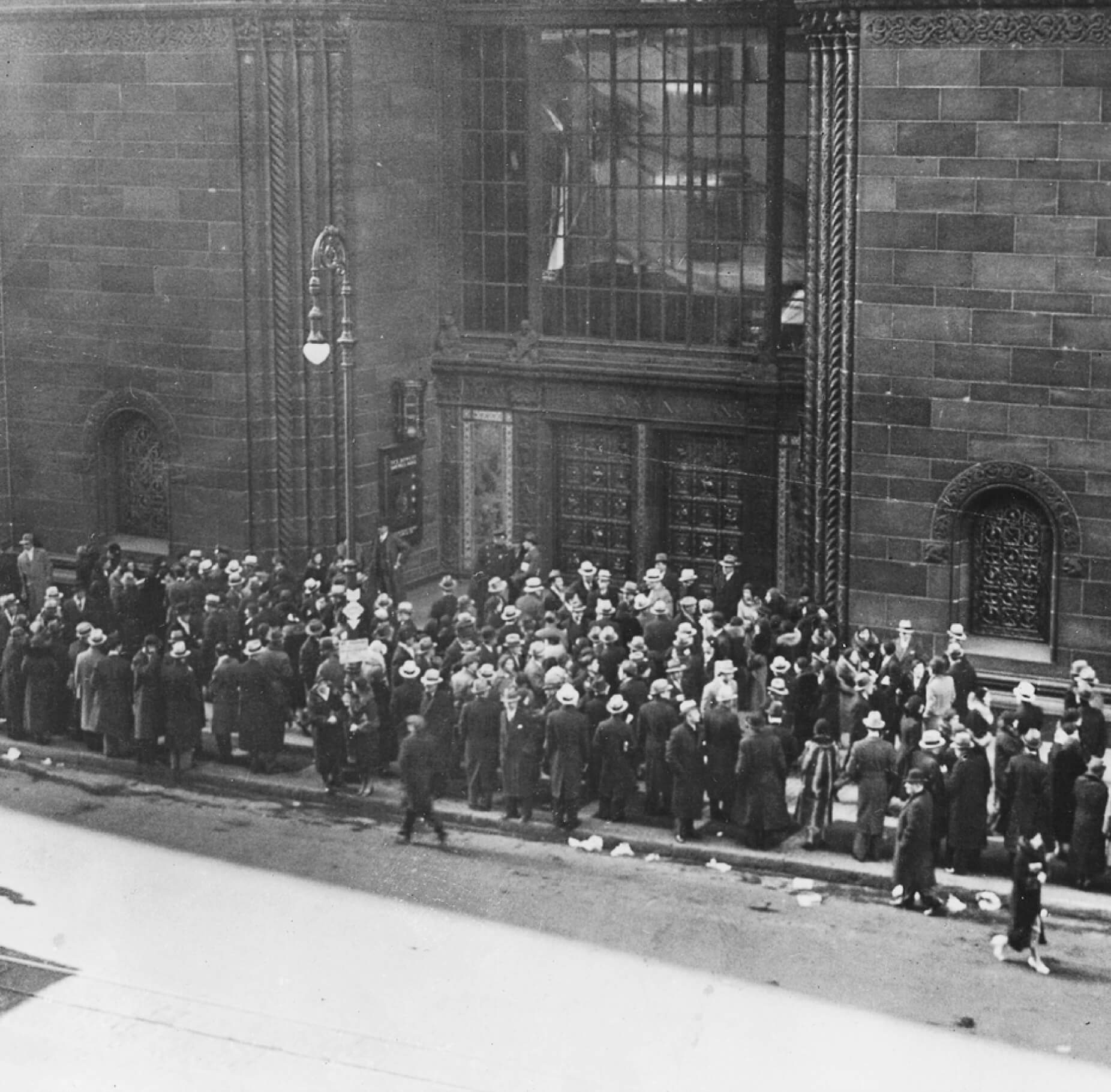

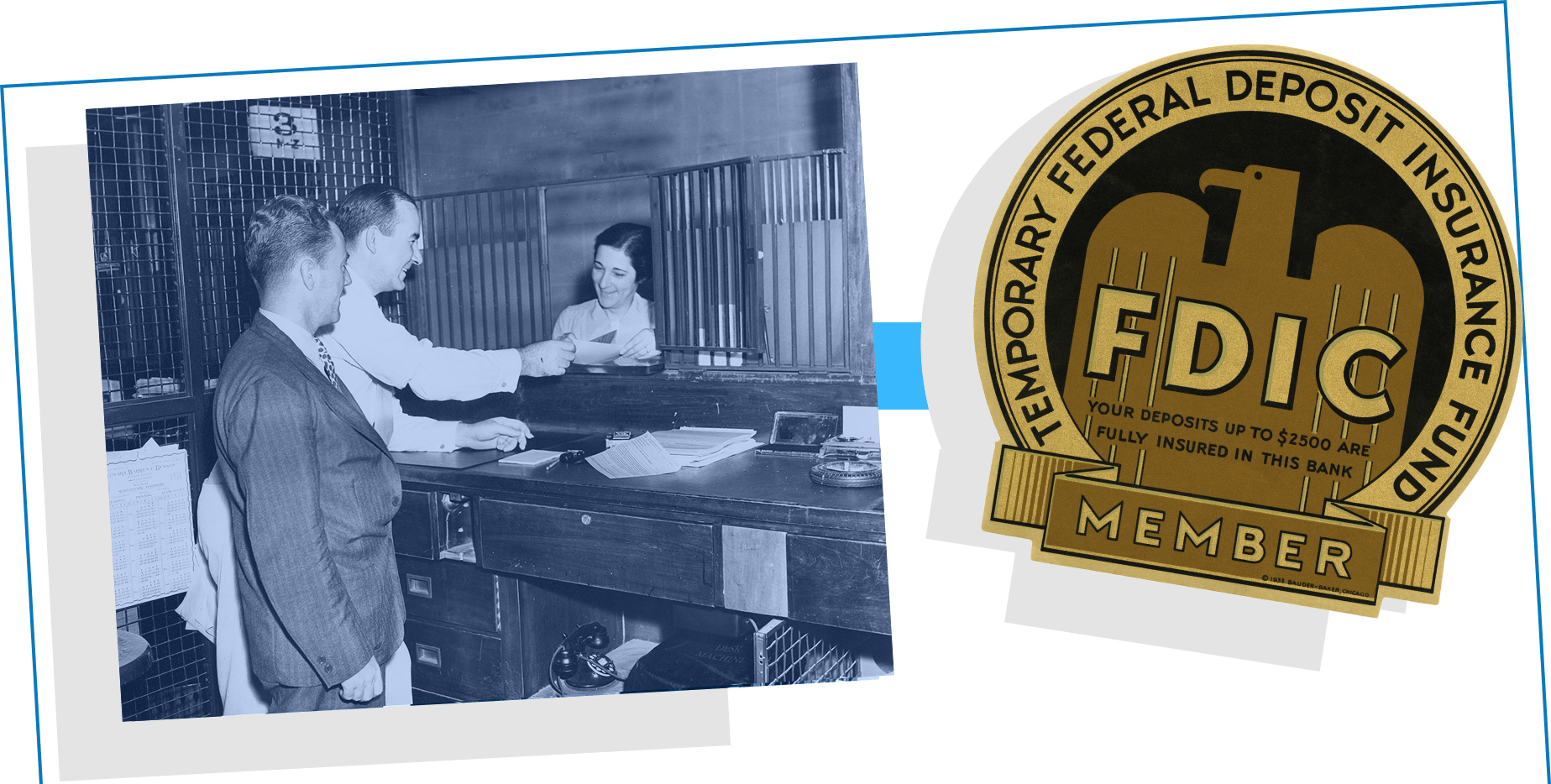

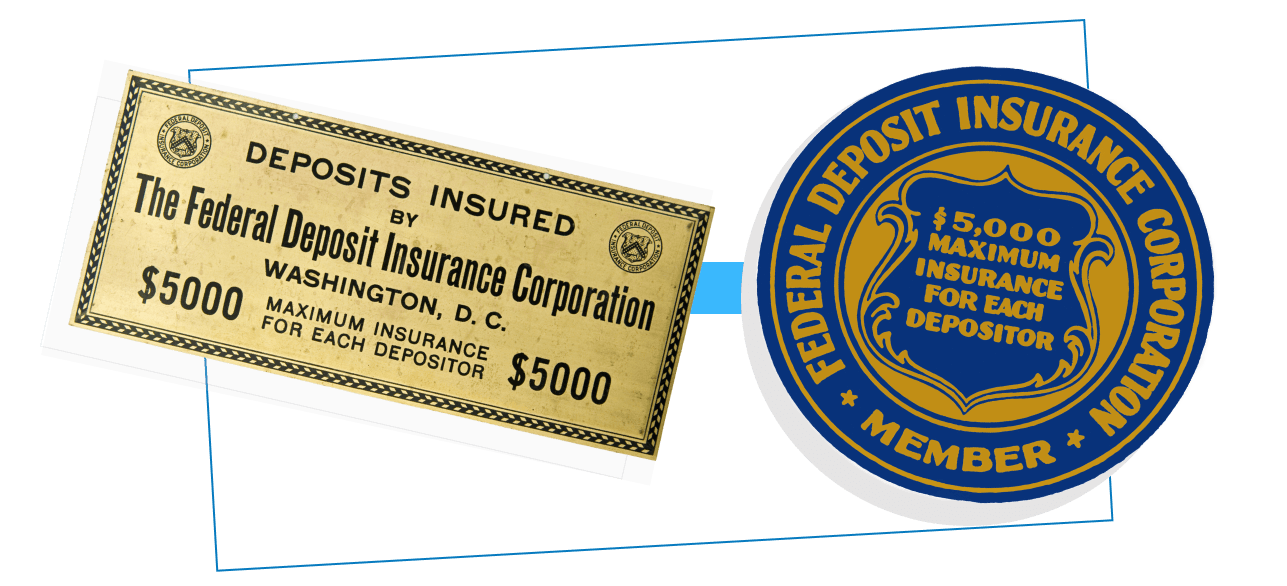

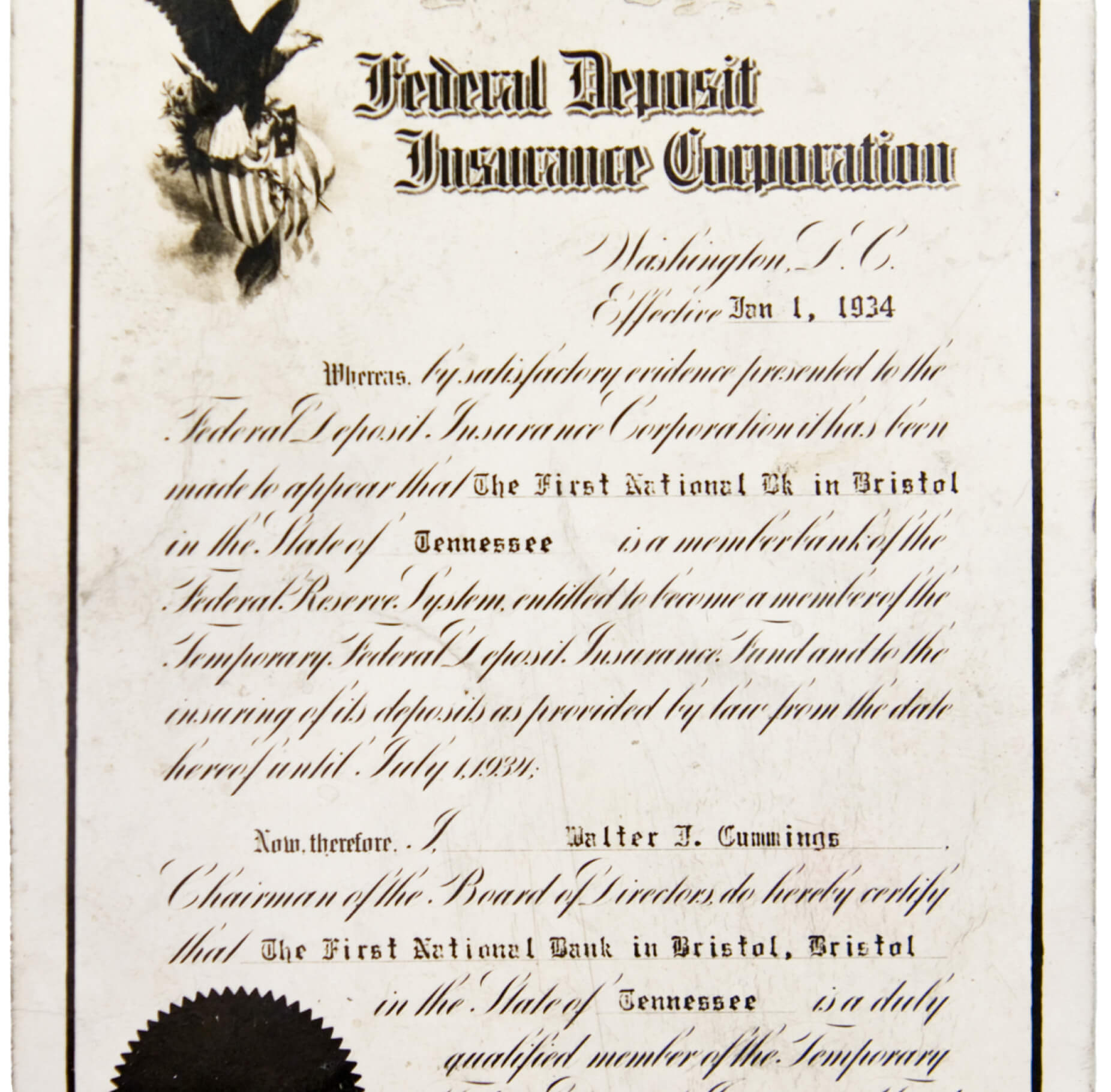

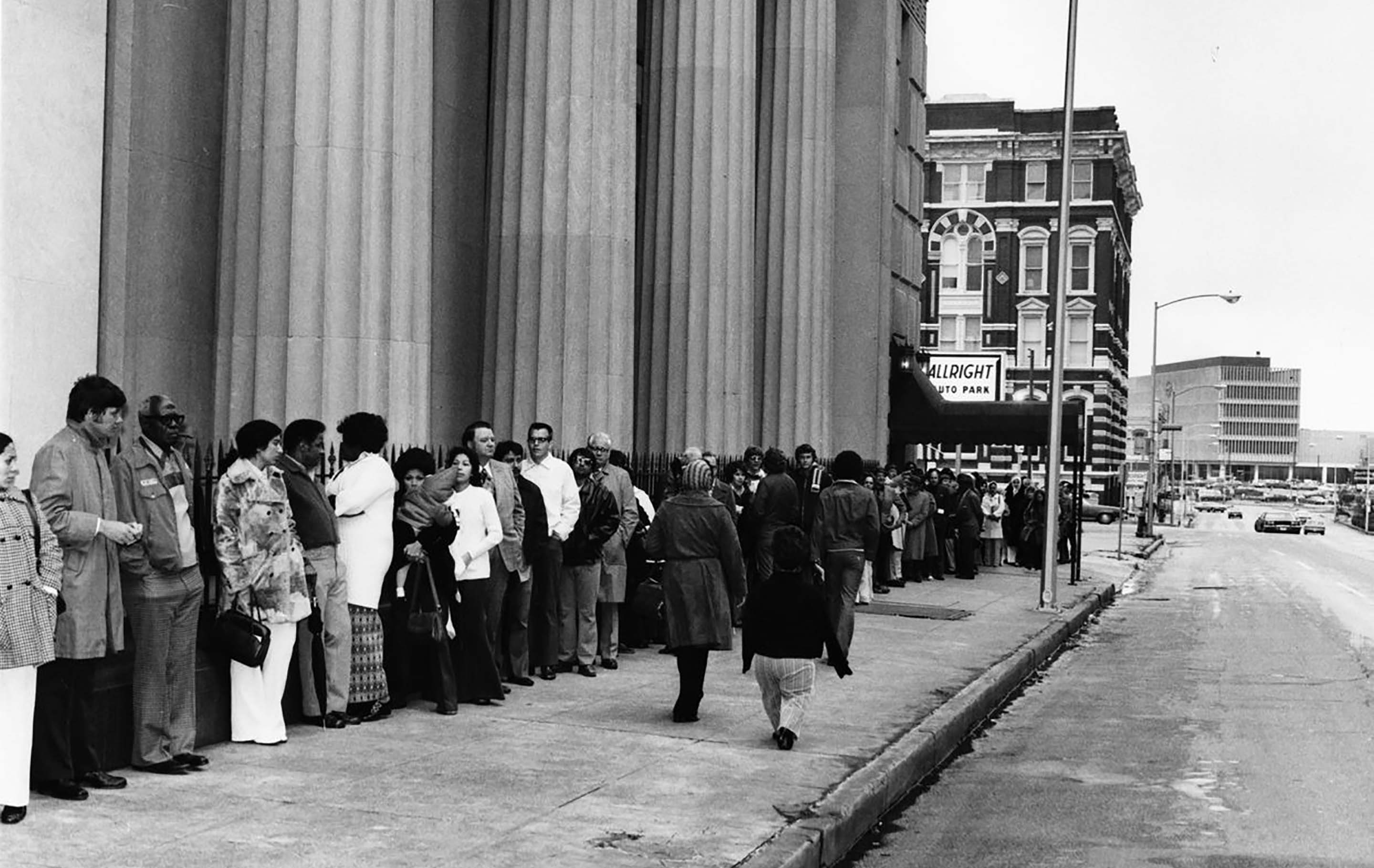

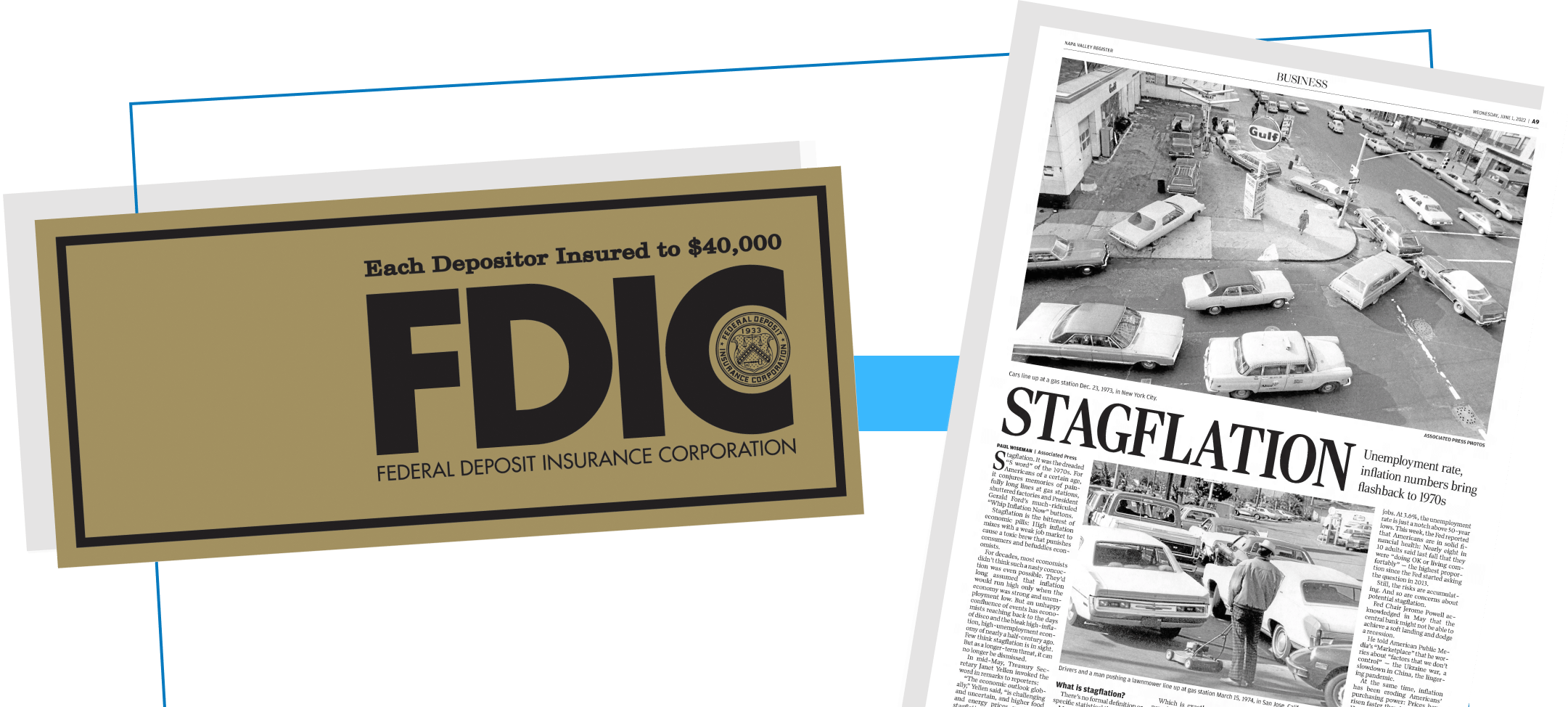

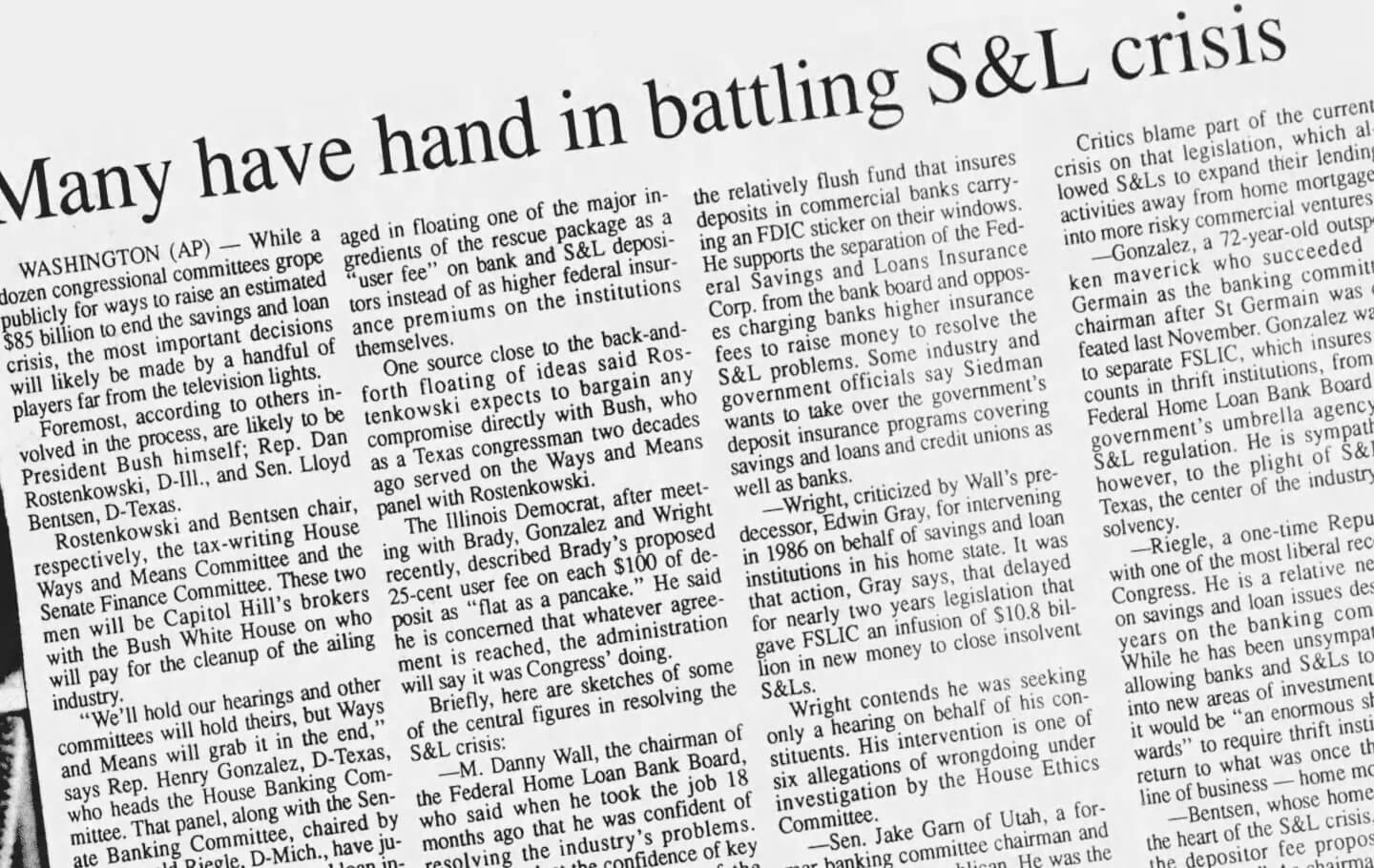

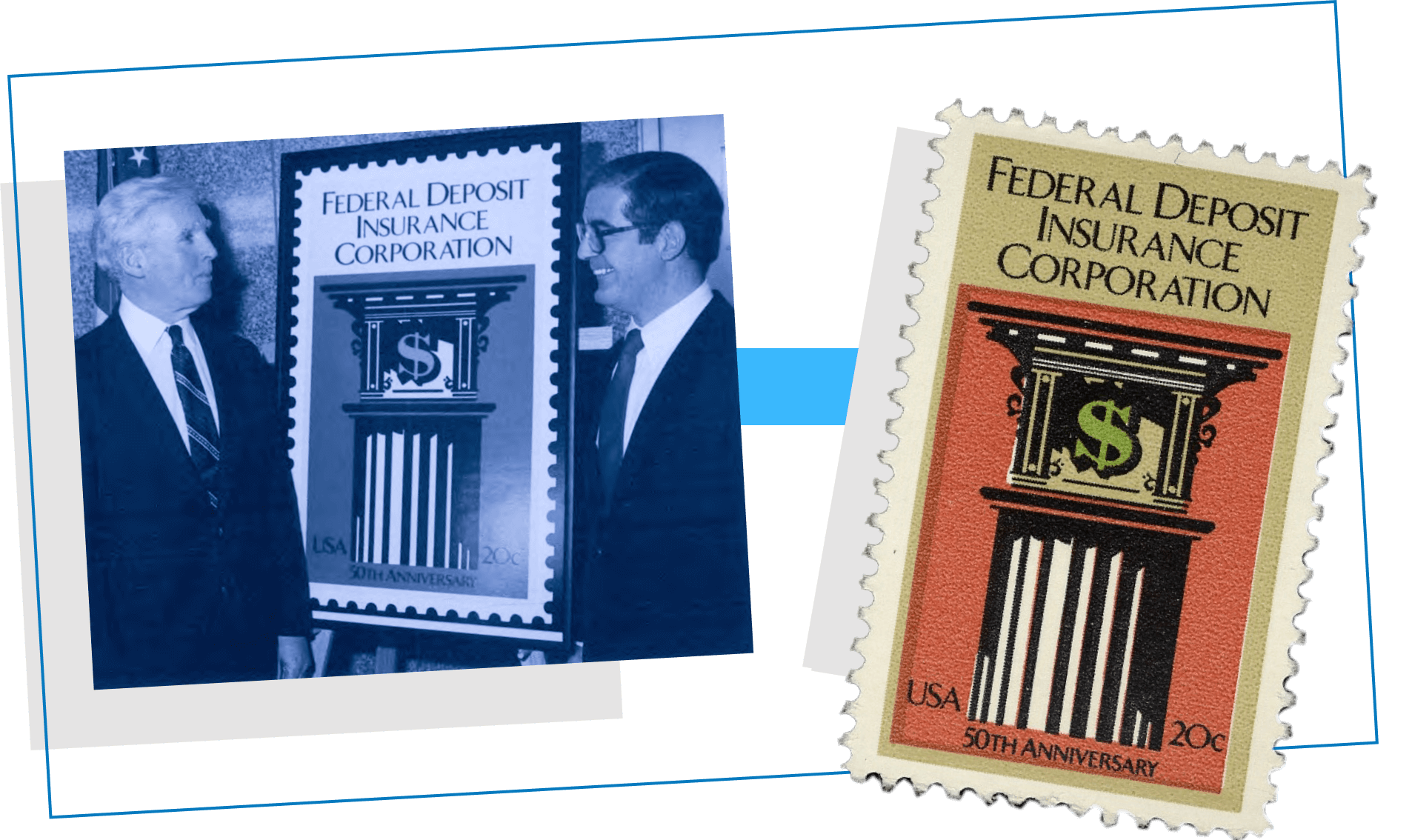

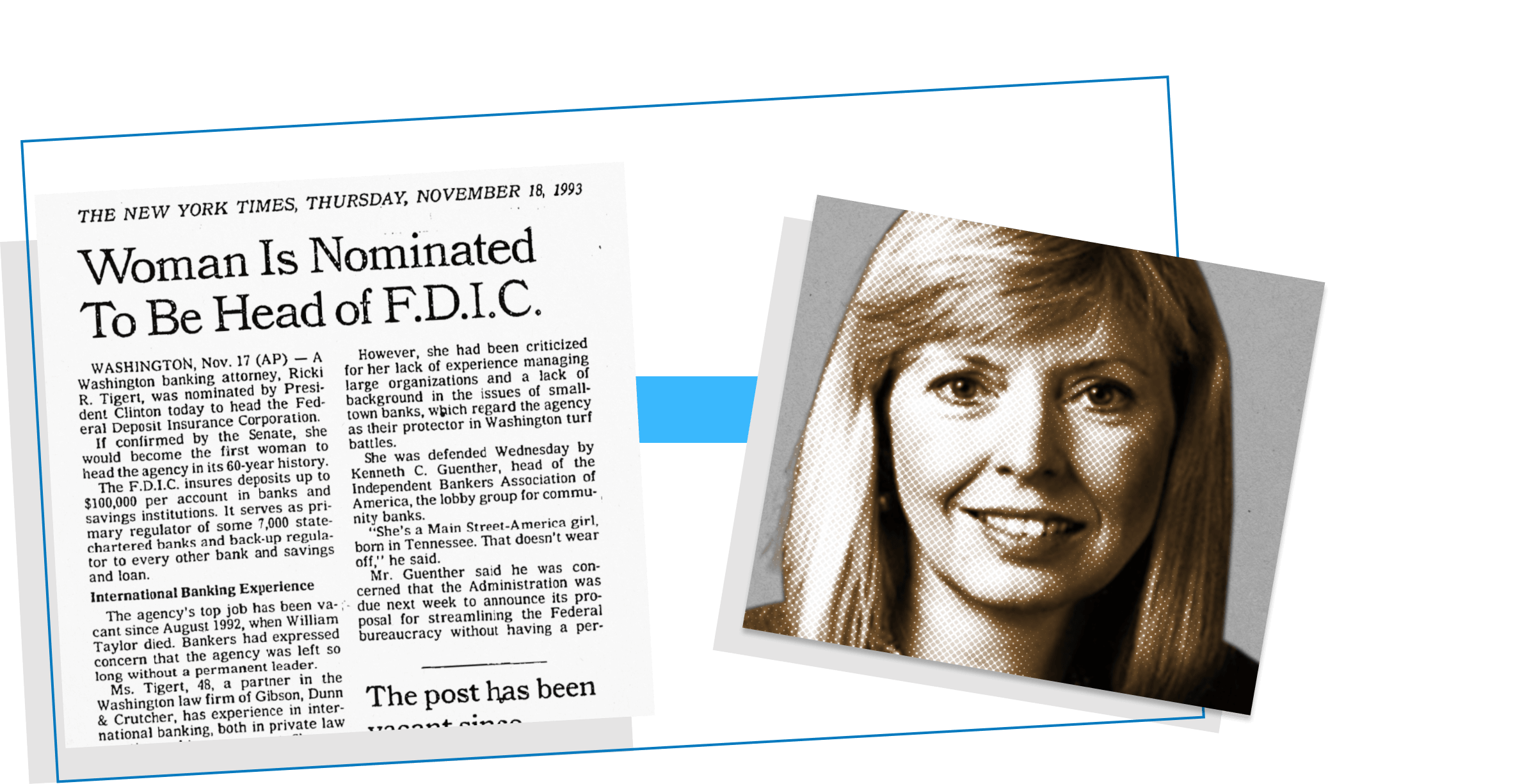

The FDIC celebrates its 90th anniversary.