|

| 2010 annual report highlights |

| Previous | Contents | Next |

I. Management’s Discussion and Analysis

The Year in Review

The year 2010 was relatively challenging for the FDIC. In addition to the normal course of business, the Corporation continued to resolve failed insured depository institutions (IDIs), increasing resources as needed. The FDIC also started initial steps in the implementation of the Dodd-Frank Act, continued its work on high-profile policy issues, and published numerous Notices of Proposed Rulemaking (NPRs) throughout the year, seeking comment from the public. The Corporation also continued to focus on a strong supervisory program. The FDIC made enhancements to several versions of the Money Smart education curriculum. The FDIC also sponsored and co-sponsored major conferences and participated in local and global outreach initiatives.

Highlighted in this section are the Corporation’s 2010 accomplishments in each of its three major business lines—Insurance, Supervision and Consumer Protection, and Receivership Management—as well as its program support areas.

Insurance

The FDIC insures bank and savings association deposits. As insurer, the FDIC must continually evaluate and effectively manage how changes in the economy, the financial markets, and the banking system affect the adequacy and the viability of the Deposit Insurance Fund (DIF).

State of the Deposit Insurance Fund

During 2009 and 2010, losses to the DIF were high. As of December 31, 2010, both the fund balance and the reserve ratio were negative after reserving for probable losses for anticipated bank failures. For the year, assessment revenue and lower-than-anticipated bank failures resulted in an increase in the reserve ratio to negative 0.12 percent as of December 31, 2010, up from negative 0.39 percent at the beginning of the year.

Long-Term Comprehensive Fund

Management Plan

As a result of the Dodd-Frank Act revisions, the FDIC developed a comprehensive, long-term management plan for the DIF designed to reduce the pro-cyclicality in the existing system and achieve moderate, steady assessment rates throughout economic and credit cycles while also maintaining a positive fund balance even during a banking crisis, by setting an appropriate target fund size and a strategy for assessment rates and dividends. The FDIC set out the plan in a proposed rulemaking adopted in October 2010. The plan was finalized in rulemakings adopted in December 2010 and February 2011.

New Restoration Plan

Pursuant to the comprehensive plan, in October 2010, the FDIC adopted a new Restoration Plan to ensure that the reserve ratio reaches 1.35 percent by September 30, 2020.

Setting the Designated Reserve Ratio

Pursuant to provisions in the Federal Deposit Insurance Act that require the FDIC Board to set the designated reserve ratio (DRR) for the DIF annually, the FDIC Board proposed in October 2010 to set the 2011 DRR at 2.0 percent of estimated insured deposits. The Board approved a final rule adopting this DRR on December 14, 2010. The FDIC views the 2.0 percent DRR as a long-term goal and the minimum level needed to withstand future crises of the magnitude of past crises.

Long-Term Assessment Rate Schedules and

Dividend Policies

Pursuant to its statutory authority to set assessments, in October 2010, the FDIC Board proposed a lower assessment rate schedule to take effect when the fund reserve ratio exceeds 1.15 percent. To increase the probability that the fund reserve ratio will reach a level sufficient to withstand a future crisis, the FDIC also proposed suspending dividends permanently when the fund reserve ratio exceeds 1.5 percent.

Change in the Deposit Insurance Assessment Base

The Dodd-Frank Act requires the FDIC to amend its regulations to define the assessment base as average consolidated total assets minus average tangible equity, rather than total domestic deposits (which, with minor adjustments, it has been since 1935). The Act allows the FDIC to modify the assessment base for banker’s banks and custodial banks. In November 2010, the FDIC approved a proposed rulemaking that would implement these changes to the assessment base. The FDIC finalized this rulemaking in February 2011.

The Dodd-Frank Act also requires that, for at least five years, the FDIC must make available to the public the reserve ratio and the DRR using both estimated insured deposits and the new assessment base. As of December 31, 2010, the FDIC estimates that the reserve ratio would have been negative 0.06 percent using the new assessment base (as opposed to negative 0.12 percent using estimated insured deposits) and that the 2.0 percent DRR using estimated insured deposits would have been 1.0 percent using the new assessment base.

Conforming Changes to Risk-Based Premium

Rate Adjustments

The changes to the assessment base necessitated changes to existing risk-based assessment rate adjustments. The current assessment rate schedule incorporates adjustments for types of funding that either pose heightened risk to the DIF or that help to offset risk to the DIF.

Conforming Changes to Assessment Rates

The new assessment base under the Dodd-Frank Act will be larger than the current assessment base. Applying the current rate schedule to the new assessment base would result in larger total assessments than are currently collected. Accordingly, the rule changing the assessment base also established new rates to take effect in the second quarter of 2011 that will result in collecting approximately the same amount of assessment revenue under the new base as under the current rate schedule using the existing (domestic deposit) base. These schedules also incorporate the changes from the proposed large bank pricing rule that was finalized in February 2011 along with the change in the assessment base. The initial base rates for all institutions will range from 5 to 35 basis points.

The initial base assessment rates, range of possible rate adjustments, and minimum and maximum total base rates are shown in the table below. Changes to the assessment base, assessment rate adjustments, and assessment rates took effect April 1, 2011. The rate schedules will decrease when the reserve ratio reaches 1.15, 2.0, and 2.5 percent.

Proposed Initial and Total Base Assessment Rates¹

|

Risk

Category I |

Risk

Category II |

Risk

Category III |

Risk

Category IV |

Large and Highly

Complex Institutions |

Initial base

assessment rate |

5–9 |

14 |

23 |

35 |

5-35 |

Unsecured debt

adjustment² |

(4.5)–0 |

(5)–0 |

(5)–0 |

(5)–0 |

(5)–0 |

Brokered deposit

adjustment |

…… |

0–10 |

0–10 |

0–10 |

0–10 |

Total Base

Assessment Rate |

2.5–9 |

9–24 |

18–33 |

30-45 |

2.5–45 |

|

Changes to the Large Bank Assessment System

The FDIC continued its efforts to reduce the pro-cyclicality of the deposit insurance assessment system by issuing a proposed rule in November 2010, that was finalized in February 2011, and revises the assessment system applicable to large IDIs to better reflect risk at the time a large institution assumes the risk, to better differentiate large institutions during periods of good economic conditions, and to better take into account the losses that the FDIC may incur if such an institution fails. The rule eliminates risk categories for large institutions.

Temporary Liquidity Guarantee Program

On October 14, 2008, the FDIC announced and implemented the Temporary Liquidity Guarantee Program (TLGP). The TLGP consists of two components: (1) the Debt Guarantee Program (DGP)—an FDIC guarantee of certain senior unsecured debt; and (2) the Transaction Account Guarantee Program (TAGP)—an FDIC guarantee in full of noninterest-bearing transaction accounts.

Under the DGP, the FDIC guaranteed in full, through maturity or June 30, 2012, whichever came first, the senior unsecured debt issued by a participating entity between October 14, 2008, and June 30, 2009, although in 2009 the issuance period was extended through October 31, 2009. The FDIC’s guarantee on each debt instrument also was extended in 2009 to the earlier of the stated maturity date of the debt or December 31, 2012.

Program Statistics

Institutions were initially required to elect whether to participate in one or both of the programs. More than half of the over 14,000 eligible entities elected to opt in to the DGP, while over 7,100 banks and thrifts, or 86 percent of FDIC-insured institutions, initially opted in to the TAGP. Most of the institutions that opted out of the DGP had less than $1 billion in assets and issued no appreciable amount of senior unsecured debt.

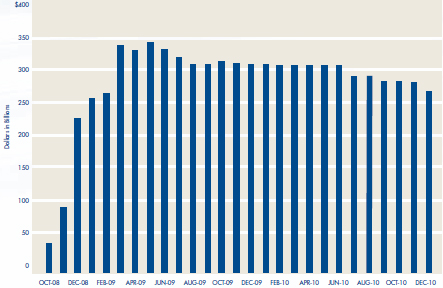

Over the course of the DGP’s existence, 121 entities issued TLGP debt. At its peak, the DGP guaranteed almost $350 billion of debt outstanding (see chart below). As of December 31, 2010, the total amount of remaining FDIC-guaranteed debt outstanding was $267 billion.

The FDIC collected $10.4 billion in fees and surcharges under the DGP. As of December 31, 2010, the FDIC paid $8 million on seven claims that were filed when four participating entities (all holding companies) defaulted on debt issued under the DGP. Further claims on notes issued by one entity are expected, since some of the notes issued by this entity have not yet matured. Losses through the end of the DGP guarantee period in 2012 are expected to be limited.

| OUTSTANDING TLGP DEBT BY MONTH |

|

|

|

Under the TAGP, the FDIC guaranteed an average of $114 billion of deposits during the fourth quarter of 2010. As of December 31, 2010, the last day of the program, over 5,100 FDIC-insured institutions reported having guaranteed deposits. As of December 31, 2010, the FDIC has collected $1.1 billion in fees under the TAGP.¹ Cumulative estimated TAGP losses on failures as of December 31, 2010, totaled $2.3 billion.

Overall, TLGP fees are expected to exceed the losses from the program. Remaining TLGP fees will be added to the DIF balance at the conclusion of the program. If fees are insufficient to cover the costs of the program, the difference will be made up through a systemic risk special assessment.

Complex Financial Institution Program

The FDIC’s Complex Financial Institution (CFI) Program addresses the unique challenges associated with the supervision, insurance, and potential resolution of large and complex insured institutions. The FDIC’s ability to analyze and respond to risks in these institutions is of particular importance, as they make up a significant share of the banking industry’s assets. The Program provides for a consistent approach to large-bank supervision nationwide, allows for the analysis of financial institution risks on an individual and comparative basis, and enables a quick response to risks identified at large institutions.

The Program expanded coverage of large and complex institutions from eight to ten in 2010 and increased its on-site presence, as designated by the FDIC Board, to assess risk, monitor liquidity, and participate in targeted reviews with the primary federal regulators. In July 2010, the FDIC entered into an interagency memorandum of understanding (MOU) which allows FDIC examiners to conduct special examinations of certain institutions covered by the MOU. The MOU should enhance the FDIC’s access to those institutions and encourage ongoing effective communication among the federal regulators.

Office of Complex Financial Institutions

The Office of Complex Financial Institutions (OCFI) was created in 2010 to focus on the expanded responsibilities of the FDIC by the Dodd-Frank Act for the assessment of risk in the largest, systemically important financial institutions. The OCFI is responsible for oversight and monitoring of large, systemically important financial institutions (SIFIs). Specifically, through both on-site and off-site monitoring, OCFI will develop an in-depth understanding of the operations and risk profiles of all IDIs and bank holding companies with assets over $100 billion and other companies designated as systemically important by the Financial Stability Oversight Council (FSOC).

Center for Financial Research

The Center for Financial Research (CFR) was founded by the Corporation in 2004 to encourage and support innovative research on topics important to the FDIC’s role as deposit insurer and bank supervisor. During 2010, the CFR co-sponsored three major conferences.

- The 20th Annual Derivatives Securities and Risk Management Conference, which the FDIC co-sponsored with Cornell University’s Johnson Graduate School of Management and the University of Houston’s Bauer College of Business, was held in April 2010 at the Seidman Center. The two-day conference attracted over 100 researchers from around the world. Conference presentations focused on issues such as credit risk measurement, equity option pricing, commodity market speculation, and risk management.

- In October 2010, the FDIC and the Federal Reserve hosted a two-day symposium on mortgages and the future of housing finance. Over 300 experts from the public, private, and academic sectors attended. Federal Reserve Chairman Ben Bernanke and FDIC Chairman Sheila Bair spoke at the symposium regarding the need for reform to restore stability to the housing finance system and to aggressively examine the incentives of the U.S. system of mortgage finance to ensure that the problems that contributed to the financial crisis are addressed.

- The CFR and the Journal for Financial Services

Research (JFSR) hosted the 10th Annual Bank

Research Conference: Finance and Sustainable Growth—with over 100 participants. The conference included the presentation of 17 papers, and focused on a range of topics that included the global financial crisis, credit derivatives and the default risk of large complex financial institutions, and bank capital adequacy.

International Outreach

The past year has been defined by broad international efforts to respond effectively to the causes of the global financial crisis. One of the important lessons of the crisis is that effective systems of deposit insurance are important not only for the protection of individual depositors but also for overall financial stability. Inadequate systems of deposit insurance place individual depositors at risk and can have a significant negative impact on public confidence in the financial system as a whole. The FDIC has provided leadership and support to international standard-setting organizations and international financial institutions, and has established bilateral agreements with other bank supervisory and deposit insurance governmental organizations, resulting in significant advancements in promoting sound financial systems.

In 2009, the International Association of Deposit Insurers (IADI) and the Basel Committee on Banking Supervision (BCBS) jointly published Core Principles for Effective Deposit Insurance Systems (Core Principles). The Core Principles were later adopted by the Financial Stability Board (FSB), which added them to its Compendium of Standards. Under the FDIC’s leadership, IADI, BCBS, the International Monetary Fund (IMF), the European Forum of Deposit Insurers (EFDI), the World Bank, and the European Commission collaborated in developing a methodology for assessing compliance with the Core Principles. The leadership of IADI under Martin J. Gruenberg, the Vice Chairman of the FDIC, has been instrumental in the advancing the establishment of the Core Principles as the standards for deposit insurance. Vice Chairman Gruenberg was re-elected to serve as President of IADI and Chair of the Executive Council in November 2010. During his tenure as President, the membership of IADI has grown from 48 to 62 deposit insurance members, including new members from Germany, Italy, Poland, Belgium, Switzerland, Australia, and Paraguay.

The FDIC is integrally involved with the FSB’s Cross Border Crisis Management Working Group (CBCM). The group has been tasked with evaluating options and making recommendations on how to address issues related with the too-big-to-fail issue. In particular, the CBCM has been focused on recovery and resolution (R&R) for SIFIs. The FDIC has been involved in R&R planning for the top five U.S. firms and has participated in Crisis Management Group meetings hosted by foreign regulators. The FDIC has also provided input and leadership to the CBCM’s development of technical work streams related to obstacles encountered in a SIFI resolution.

Throughout 2010, the FDIC participated in Governors and Heads of Supervision and BCBS meetings and contributed to the work streams, task forces, and the Policy Development Group that developed and refined regulatory forms to address a new definition of capital, treatment of counterparty credit risk, an international leverage ratio, capital conservation and countercyclical buffers, liquidity requirements, and surcharges on SIFIs.

The FDIC finalized a resolution and crisis management MOU with the China Banking Regulatory Commission (CBRC) in 2010. The FDIC is currently in the process of negotiating a similar MOU with the Swiss Financial Market Supervisory Authority (FINMA). The MOU with FINMA is expected to be finalized by the end of 2011. The FDIC has reached out to other strategic countries including India, and has been met with enthusiasm by Indian officials. In 2011, the FDIC will review its resolution MOU with the Bank of England to determine what, if any, changes need to be made in light of regulatory developments both in the U.S. and the United Kingdom.

|

| Previous | Contents | Next |

Last Updated 6/6/2011 |

communications@fdic.gov |

|