|

Home > About FDIC > Financial Reports > 2000 Annual Report |

|||

|

2000 Annual Report |

||

Operations of the Corporation – The Year in Review |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The year 2000 may well be remembered as a watershed in the history of the FDIC. The Corporation undertook a comprehensive review of the deposit insurance system with an eye toward addressing its weaknesses. As part of that effort, the Corporation commissioned a national household survey, conducted by the Gallup Organization, to measure public understanding of–and support for– the deposit insurance program. Also, the FDIC sponsored global efforts to establish or improve deposit insurance systems. In May, for example, the Corporation and the Financial Stability Institute co-hosted a seminar on these issues in Basel, Switzerland – a seminar that drew approximately 150 people who represented more than 60 countries. And in June the Corporation hosted a meeting in Washington, DC, of the Financial Stability Forum’s (FSF) Working Group on Deposit Insurance. The FSF was created in 1999 by the finance ministers and other officials of the G-7 industrial nations as a way to promote international financial stability through information exchange and international cooperation.

In addition to deposit insurance, the year 2000 might be considered a watershed in other ways. Concerns began to grow about the condition of the industry, which had experienced unprecedented profitability during the 1990s. And, though industry conditions did not significantly affect the deposit insurance funds, the Corporation in 2000 undertook several safety and soundness initiatives to address emerging risks. It also developed contingency plans for the failure of a very large institution, or an institution that operates on the Internet. It addressed the effects of evolving technology, both internally and externally. The Corporation invested in its employees through its diversity program. And–working with other bank regulators–it dealt with many of the demands of the landmark financial modernization legislation enacted in 1999, the Gramm-Leach-Bliley Act. In summary, the FDIC spent the year 2000 responding to changes in the industry it insures and supervises, and in doing so prepared itself for the new financial world technology continues to create. Overview of the Industry and the Deposit

Insurance Funds Commercial banks’ eight consecutive years of record earnings came to an end in 2000, as net income of $71.2 billion fell $380 million (0.5 percent) short of 1999’s record total. The industry’s earnings decline was mostly attributable to problems at a few large banks. The average return on assets (ROA) of 1.19 percent was down from the record 1.31 percent registered in 1999. Even so, 2000 marks the eighth consecutive year that the industry had an ROA above one percent. The industry’s net interest margin of 3.95 percent was the lowest level since 1990. In 2000, securities sales produced net losses and provision expenses rose sharply with loan-loss provisions totaling $29.3 billion, an increase of $7.4 billion (34.1 percent) over 1999. Noninterest income growth was sluggish in 2000; however, this was aided by slower growth in noninterest expenses. From 1999 to 2000, the annualized net charge-off rate on commercial and industrial (C&I) loans rose to 1.15 percent, from 0.79 percent a year ago. Noncurrent loans during 2000 increased by $9.9 billion (30.0 percent), with C&I loans accounting for $6.1 billion (61.4 percent) of the increase. Insured savings institutions earned $10.7 billion in 2000, down $126 million from the record earnings of 1999. This was the third year in a row that industry earnings were over $10 billion. The average ROA was 0.92 percent, down from 1.00 percent in 1999. Increased noninterest expenses negated improvements in noninterest income, while an inverted yield curve continued to put downward pressure on thrifts’ net interest margins. Net charge-offs, at 0.20 percent of loans, were $349 million (29 percent) higher than in 1999, but provisions for loan losses exceeded these charges by over 30 percent in both years. The FDIC administers two deposit insurance funds–the Bank Insurance Fund (BIF) and the Savings Association Insurance Fund (SAIF)–and manages the FSLIC Resolution Fund (FRF), which fulfills the obligations of the former Federal Savings and Loan Insurance Corporation (FSLIC) and the former Resolution Trust Corporation (RTC). The following summarizes the condition of insured institutions and the FDIC’s insurance funds. Deposit insurance assessment rates remained unchanged from 1999 for both the BIF and the SAIF, ranging from 0 to 27 cents annually per $100 of assessable deposits. Under the assessment rate schedule, 92.7 percent of BIF-member institutions and 88.8 percent of SAIF-member institutions were in the lowest risk-assessment rate category and paid no deposit insurance assessments for the first semiannual period of 2001.

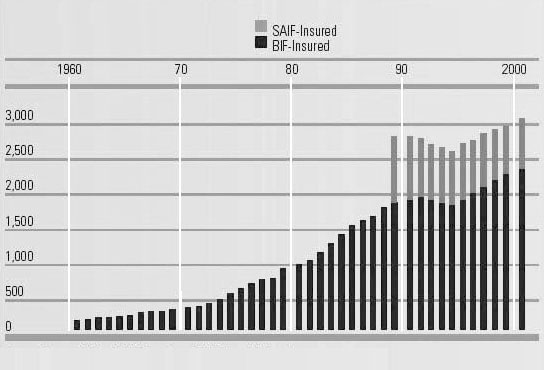

Deposits insured by the FDIC moved past the $3 trillion level in 2000, to $3.05 trillion, despite the number of insured institutions falling below the 10,000 mark for the first time. Insured deposits rose by 2.1 percent in the final three months of 2000, bringing the growth rate for 2000 to 6.5 percent. This annual growth rate for federally insured deposits is the highest since 1986, when deposits insured by the FDIC and the FSLIC increased by eight percent. Insured deposits reported by the 9,924 FDIC-insured institutions rose by $185 billion in 2000, including a $73 billion increase (81 percent) in insured brokered deposits. About half of the latter amount was attributable to two insured banks with brokerage affiliates that "sweep" cash management account balances into FDIC-insured bank accounts. By year-end 2000, deposits insured by the BIF grew at seven percent and reached $2.3 trillion. This annual growth rate for BIF-insured deposits was the highest since 1989. The BIF balance was $31 billion at year-end 2000, or 1.35 percent of estimated insured deposits. This was down from the year-end 1999 reserve ratio of 1.36 percent as the $1.6 billion growth of the fund’s balance during 2000 was more than offset by the growth of insured deposits.

The reserve ratio of the SAIF was 1.43 percent at year-end 2000, down slightly from 1.45 percent at year-end 1999. The balance of the SAIF was $10.8 billion on December 31, 2000. SAIF-insured deposits were $753 billion at year-end 2000, having grown 5.8 percent for the year. The annual growth rate was the highest since the inception of the SAIF in 1989. Despite the relatively rapid growth of insured deposits, insured institutions continued to rely increasingly on other funding alternatives. Insured deposits as a percentage of domestic liabilities continued a steady, nine-year decline, falling to 51.7 percent at the end of 2000, compared to 52.6 percent a year earlier and 70 percent in 1992. At year-end 2000, the ratio was 46.4 percent for institutions with total assets greater than $1 billion, and 74 percent for smaller institutions. During 2000, seven FDIC-insured institutions failed. Six of those institutions were insured by the BIF and one was insured by the SAIF. The failed institutions had combined assets of approximately $408 million. Losses for the seven failures are estimated at $40 million. In 1999, there were eight failures of insured institutions, with total assets of $1.5 billion and estimated losses of $839 million. The contingent liability for anticipated failures of BIF- and SAIF-insured institutions as of December 31, 2000, was $141 million and $234 million, respectively. Responding to Emerging Risks

New "screens," or models designed to flag outlier statistics and ratios, based on quarterly financial data, were added to the process for assigning assessment risk classifications. These screens identify institutions in the best-rated category with atypically high-risk profiles. The screens flag combinations of rapid loan growth, high-yielding loan portfolios, concentrations in high-risk assets, and recent changes in business mix. For the institutions identified, a supervisory review is conducted to determine if concerns exist regarding risk-management practices. If so, the institution is notified that unless actions are taken to address the concerns before the next semiannual assessment period, a higher premium may be assessed. During the year, the FDIC developed a training program to instruct examiners in methods of fraud detection and investigation, desirable skills when technology makes fraud ever easier to commit and harder to detect. The FDIC also participated in a number of local, state and national working groups relating to financial institution fraud and money laundering. These groups seek to improve information sharing and to develop uniform policies and approaches to deterring and detecting fraud.

In September 2000, the FDIC, along with the other banking and thrift agencies, proposed a revision to the capital treatment for residual interests in securitizations or other transfers of assets. Residual interests are typically the assets an institution retains in connection with its securitization activities. The proposed rule would require an institution to hold a dollar of capital for every dollar in residual interests, and would make related changes in Tier 1 capital. Lastly, to keep pace with the evolving banking industry, the FDIC continued its contingency planning for possible future failures. In light of the banking industry’s increasing consolidation and reliance on and use of the Internet and electronic commerce, the FDIC focused its planning in 2000 on the need to address possible technological failures and large insured depository institution failures. As a result, the FDIC began modifying its resolution procedures to address issues associated with larger, more complex, institutions and electronic banking and commerce. Additionally, the FDIC began implementing a core training program to cross-train personnel to maintain its readiness capacity.

Technology

Significant growth in electronic banking or "E-Banking" was evidenced by the 64 percent increase in the number of FDIC-insured banks offering transactional services over the Internet (1,850 institutions at year-end 2000 compared to 1,130 a year earlier), as well as the increasing sophistication of technology used in E-banking activities. The FDIC at year-end 2000 had 288 specially trained electronic banking examiners and similar specialists nationwide, and it established the Electronic Banking Branch in its Division of Supervision. This newly created branch will provide oversight of information systems and E-banking activities for all state nonmember banks. The FDIC also worked with the Federal Reserve to enhance the risk-focused examination module for electronic banking used in bank examinations. In addition, general electronic banking training also was provided to examiners. And, the FDIC continued to use technology to improve the failed-bank resolution and asset marketing processes. In 2000, the FDIC conducted its first teleconference with prospective acquirers for a failed bank at five locations across the country; established a secure Web site allowing for the rapid sharing of confidential information with prospective acquirers of a failed institution; and conducted its first sale of financial assets over the Internet, with approximately $12.3 million of loans at a recovery that was 16 percent higher than expected.

Gramm-Leach-Bliley Act For example, the Corporation began working with the National Association of Insurance Commissioners to explore ways that information can be shared among the banking and insurance regulators to improve regulation. Similar arrangements will be explored with securities regulators. The Corporation also revised its regulatory standards to reflect aspects of GLBA that require separate adequate capital for a bank and its securities subsidiary, and restrict financial dealings between the bank and its securities affiliate or subsidiary. GLBA also made Federal Home Loan Bank (FHLB) membership available to more institutions and permitted certain FHLB-member institutions to obtain more advance funding. In response to these changes, the FDIC issued supplemental examination guidance in August 2000. The guidance provides an overview of FHLB advance strategies and presents a framework for examining the effects of these strategies when determining the adequacy of an institution’s policies, practices and financial condition. Lastly, the FDIC and the other banking agencies implemented regulations protecting consumers purchasing insurance products and annuities through the bank. The new rules govern the sale and solicitation of insurance products and annuities made by the bank as well as by others selling on the bank’s behalf. These protections include customer disclosures, advertising requirements, standards regarding the physical location where sales may occur, and prohibitions against tying the purchase of insurance products to the use of any bank product.This regulation will go into effect late in 2001. Diversity Initiatives

Also in 2000, the Corporation:

Consumer Complaints and Inquiries In 2000, the FDIC received nearly 4,500 written consumer complaints against state-chartered nonmember banks. The agency tracks the volume and nature of complaints to monitor trends and identify emerging issues. Nearly two-thirds of these complaints concerned credit card accounts. The most frequent complaints involved billing disputes and account errors; loan denials; credit card fees and service charges; and collection practices. The FDIC also received over 2,000 written inquiries from consumers and over 200 written inquiries from bankers as to whether specific financial institutions are insured by the FDIC, or questions about FDIC deposit insurance coverage. Other common inquiries were requests for copies of FDIC consumer publications, questions about banking practices and consumers’ rights under federal consumer protection laws, and questions related to obtaining a personal credit report. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| PREVIOUS | NEXT | CONTENTS | FDIC HOME |

| Last Updated 03/27/2002 | communications@fdic.gov |