II. Financial Highlights

Deposit Insurance Fund Performance

The FDIC administers the Deposit Insurance

Fund (DIF) and the FSLIC Resolution Fund

(FRF), which fulfills the obligations of the former

Federal Savings and Loan Insurance Corporation

(FSLIC) and the former Resolution Trust

Corporation (RTC). The following summarizes

the condition of the DIF.

For 2010, the DIF’s comprehensive income was

$13.5 billion compared to a comprehensive loss

of $38.1 billion during 2009. This year-over-year

change of $51.6 billion was primarily due

to a $58.6 billion decline in the provision for

insurance losses, partially offset by a $4.1 billion

decrease in assessments earned (largely attributable

to the 2009 special assessment).

The provision for insurance losses was negative

$848 million for 2010, compared to positive

$57.7 billion for 2009. The 2009 provision

reflected the significant losses estimated to be

incurred by the DIF from the 2009 and future

failures. In contrast, the 2010 negative provision

is primarily impacted by a reduction in the

contingent loss reserve due to the improvement

in the financial condition of institutions that were

previously identified to fail and adjustments to the

estimated losses for banks that have failed.

The DIF’s total liquidity declined by $19.9

billion, or 30 percent, to $46.2 billion during

2010. The decrease was primarily the result

of disbursing $28.8 billion to fund 157 bank

failures during 2010, although it should be noted

that 130 of these failures were resolved as cash-conserving

loss-share transactions (in which the

acquirers purchased substantially all of the failed

institutions’ assets and the FDIC and the acquirers

entered into loss-share agreements) requiring

lower initial resolution funding. Moreover, during

2010, the DIF received $13.6 billion in dividends

and other payments from its receiverships, which

helped to mitigate the DIF liquidity’s decline.

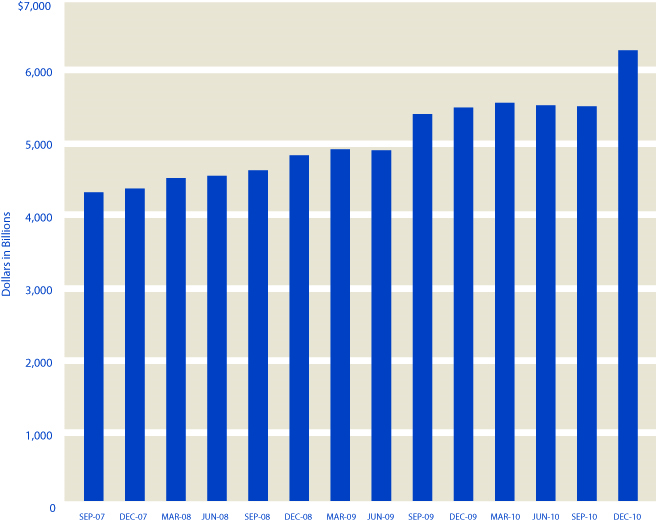

| ESTIMATED DIF INSURED DEPOSITS |

|

SOURCE: Commercial Bank

Call and Thrift Financial Reports

Note: Beginning in the fourth quarter of 2010,

estimated insured deposits include the entire balance of

noninterest-bearing transaction accounts.

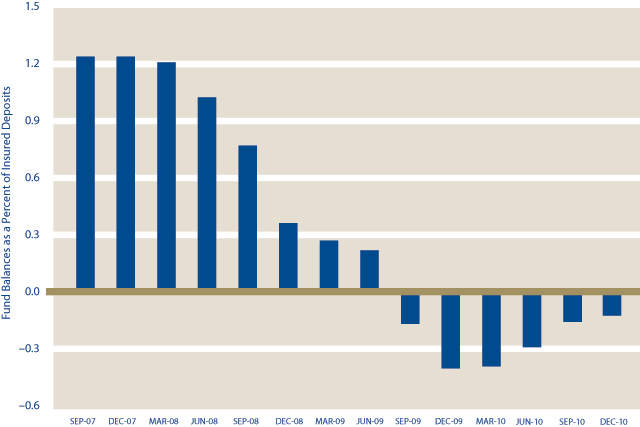

| DEPOSIT INSURANCE FUND RESERVE RATIOS |

|

Deposit Insurance Fund Selected Statistics

|

For the years ended December 31 |

| Dollars in Millions |

| |

2010 |

2009 |

2008 |

| Financial Results |

| Revenue |

$13,380 |

$24,706 |

$7,306 |

| Operating Expenses |

1,593 |

1,271 |

1,033 |

Insurance and Other Expenses

(includes provision for loss) |

(1,518) |

59,438 |

43,306 |

| Net Income (Loss) |

13,305 |

(36,003) |

(37,033) |

| Comprehensive Income (Loss) |

13,510 |

(38,138) |

(35,137) |

| Fund Balance |

$(7,352) |

$(20,862) |

$17,276 |

| Reserve Ratio |

(0.12) % |

(0.39) % |

0.36 % |

| Selected Statistics |

| Total DIF-Member Institutions¹ |

7,657 |

8,012 |

8,305 |

| Problem Institutions |

884 |

702 |

252 |

| Total Assets of Problem Institutions |

$390,017 |

$402,782 |

$159,405 |

| Institution Failures |

157 |

140 |

25 |

| Total Assets of Failed Institutions in Year² |

$92,085 |

$169,709 |

$371,945 |

| Number of Active Failed Institution Receiverships |

336 |

179 |

41 |

|