I. Management's Discussion and Analysis

The Year in Review

The year 2010 was relatively challenging for

the FDIC. In addition to the normal course of

business, the Corporation continued to resolve

failed insured depository institutions (IDIs),

increasing resources as needed. The FDIC also

started initial steps in the implementation of the

Dodd-Frank Act, continued its work on highprofile

policy issues, and published numerous

Notices of Proposed Rulemaking (NPRs)

throughout the year, seeking comment from the

public. The Corporation also continued to focus

on a strong supervisory program. The FDIC made

enhancements to several versions of the Money

Smart education curriculum. The FDIC also

sponsored and co-sponsored major conferences

and participated in local and global outreach

initiatives.

Highlighted in this section are the Corporation’s

2010 accomplishments in each of its three

major business lines—Insurance, Supervision

and Consumer Protection, and Receivership

Management—as well as its program

support areas.

Insurance

The FDIC insures bank and savings association

deposits. As insurer, the FDIC must continually

evaluate and effectively manage how changes

in the economy, the financial markets, and the

banking system affect the adequacy and the

viability of the Deposit Insurance Fund (DIF).

State of the Deposit Insurance Fund

During 2009 and 2010, losses to the DIF were

high. As of December 31, 2010, both the fund

balance and the reserve ratio were negative after

reserving for probable losses for anticipated bank

failures. For the year, assessment revenue and

lower-than-anticipated bank failures resulted

in an increase in the reserve ratio to negative

0.12 percent as of December 31, 2010, up from

negative 0.39 percent at the beginning of the year.

Long-Term Comprehensive Fund

Management Plan

As a result of the Dodd-Frank Act revisions,

the FDIC developed a comprehensive, long-term

management plan for the DIF designed to reduce the pro-cyclicality in

the existing system

and achieve moderate, steady assessment rates

throughout economic and credit cycles while

also maintaining a positive fund balance even

during a banking crisis, by setting an appropriate

target fund size and a strategy for assessment rates

and dividends. The FDIC set out the plan in a

proposed rulemaking adopted in October 2010.

The plan was finalized in rulemakings adopted in

December 2010 and February 2011.

New Restoration Plan

Pursuant to the comprehensive plan, in October

2010, the FDIC adopted a new Restoration

Plan to ensure that the reserve ratio reaches 1.35

percent by September 30, 2020. Because of

lower expected losses over the next five years than

previously anticipated, and the additional time

provided by the Dodd-Frank Act to meet the

minimum (albeit higher) required reserve ratio,

the new Restoration Plan elected to forego the

uniform 3 basis point increase in assessment rates

scheduled to go into effect on January 1, 2011.

Setting the Designated Reserve Ratio

Using historical fund loss and simulated income

data from 1950 to the present, the FDIC

undertook an analysis to determine how high the

reserve ratio would have had to have been before

the onset of the two crises that occurred since the

late 1980s to have maintained both a positive fund

balance and stable assessment rates throughout

the period. The analysis concluded that a

moderate, long-term average industry assessment

rate, combined with an appropriate dividend

or assessment rate reduction policy, would have

been sufficient to have prevented the fund from

becoming negative during the crises, though the

fund reserve ratio would have had to exceed 2.0

percent before the onset of the crises.

Therefore, pursuant to provisions in the Federal

Deposit Insurance Act that require the FDIC

Board to set the DRR for the DIF annually, the

FDIC Board proposed in October 2010 to set

the 2011 Designated Reserve Ratio (DRR) at

2.0 percent of estimated insured deposits. The

Board approved a final rule adopting this DRR

on December 14, 2010. The FDIC views the

2.0 percent DRR as a long-term goal and the

minimum level needed to withstand future crises

of the magnitude of past crises. However, the

FDIC’s analysis shows that a reserve ratio higher

than 2.0 percent would increase the chance that

the fund will remain positive during a future

economic and banking downturn similar to or

more severe than past crises. Thus, the 2.0 percent

DRR should not be viewed as a cap on the fund.

Long-Term Assessment Rate Schedules and

Dividend Policies

Once the reserve ratio reaches 1.15 percent,

the FDIC believes that assessment rates can be

reduced to a moderate level. Therefore, pursuant

to its statutory authority to set assessments, in

October 2010, the FDIC Board proposed a lower

assessment rate schedule to take effect when

the fund reserve ratio exceeds 1.15 percent. To

increase the probability that the fund reserve

ratio will reach a level sufficient to withstand a

future crisis, the FDIC also proposed suspending

dividends permanently when the fund reserve

ratio exceeds 1.5 percent. In lieu of dividends,

the FDIC Board proposed to adopt progressively

lower assessment rate schedules when the reserve

ratio exceeds 2.0 percent and 2.5 percent.

These lower assessment rate schedules will serve

much the same function as dividends, but will

provide more stable and predictable effective

assessment rates. The FDIC finalized these long-term

assessment rate and dividend changes in

February 2011 in concert with the changes to the

assessment base and large-bank pricing system

described below.

Change in the Deposit Insurance Assessment Base

Change in the Assessment Base

The Dodd-Frank Act requires the FDIC to amend

its regulations to define the assessment base as

average consolidated total assets minus average

tangible equity, rather than total domestic deposits

(which, with minor adjustments, it has been since

1935). The Act allows the FDIC to modify the

assessment base for banker’s banks and custodial

banks. In November 2010, the FDIC approved a proposed rulemaking that

would implement

these changes to the assessment base. The FDIC

finalized this rulemaking in February 2011.

The Dodd-Frank Act also requires that, for at

least five years, the FDIC must make available

to the public the reserve ratio and the DRR

using both estimated insured deposits and the

new assessment base. As of December 31, 2010,

the FDIC estimates that the reserve ratio would

have been negative 0.06 percent using the new

assessment base (as opposed to negative 0.12

percent using estimated insured deposits) and

that the 2.0 percent DRR using estimated insured

deposits would have been 1.0 percent using the

new assessment base.

Conforming Changes to Risk-Based Premium

Rate Adjustments

The changes to the assessment base necessitated

changes to existing risk-based assessment rate

adjustments. The current assessment rate schedule

incorporates adjustments for types of funding that

either pose heightened risk to the DIF or that help

to offset risk to the DIF. Because the magnitude of

these adjustments and the cap on the adjustments

have been calibrated to a domestic deposit assessment

base, the rule changing the assessment base

also recalibrates the unsecured debt and brokered

deposit adjustments. Since secured liabilities

will be included in the assessment base, the rule

eliminates the secured liability adjustment.

The assessment rate of an institution would also

increase if it holds unsecured debt issued by other

IDIs. The issuance of unsecured debt by an IDI

lessens the potential loss to the DIF in the event of

the institution’s failure; however, when the debt is

held by other IDIs, the overall risk in the system is

not reduced.

Conforming Changes to Assessment Rates

The new assessment base under the Dodd-Frank

Act will be larger than the current assessment

base. Applying the current rate schedule to

the new assessment base would result in larger

total assessments than are currently collected.

Accordingly, the rule changing the assessment

base also established new rates to take effect in

the second quarter of 2011 that will result in

collecting approximately the same amount of

assessment revenue under the new base as under

the current rate schedule using the existing

(domestic deposit) base. These schedules also

incorporate the changes from the proposed large

bank pricing rule that was finalized in February

2011 along with the change in the assessment

base. The initial base rates for all institutions will

range from 5 to 35 basis points.

The initial base assessment rates, range of possible

rate adjustments, and minimum and maximum

total base rates are shown in the table below.

Changes to the assessment base, assessment

rate adjustments, and assessment rates will take

effect April 1, 2011. As explained above, the rate

schedules will decrease when the reserve ratio

reaches 1.15, 2.0, and 2.5 percent.

Proposed Initial and Total Base Assessment Rates¹

|

Risk

Category I |

Risk

Category II |

Risk

Category III |

Risk

Category IV |

Large and Highly

Complex Institutions |

Initial base

assessment rate |

5–9 |

14 |

23 |

35 |

5-35 |

Unsecured debt

adjustment² |

(4.5)–0 |

(5)–0 |

(5)–0 |

(5)–0 |

(5)–0 |

Brokered deposit

adjustment |

…… |

0–10 |

0–10 |

0–10 |

0–10 |

Total Base

Assessment Rate |

2.5–9 |

9–24 |

18–33 |

30-45 |

2.5–45 |

|

Changes to the Large Bank Assessment System

The FDIC continued its efforts to reduce the

pro-cyclicality of the deposit insurance assessment

system by issuing a proposed rule in November

2010, that was finalized in February 2011, and

revises the assessment system applicable to large

IDIs to better reflect risk at the time a large

institution assumes the risk, to better differentiate

large institutions during periods of good economic

conditions, and to better take into account

the losses that the FDIC may incur if such an

institution fails.

The rule eliminates risk categories for large

institutions. As required by the Dodd-Frank Act,

under the rule, the FDIC will no longer use long-term

debt issuer ratings to calculate assessment

rates for large institutions. The rule combines

CAMELS¹ ratings and financial measures into two

scorecards—one for most large institutions and

another for the remaining very large institutions

that are structurally and operationally complex or

that pose unique challenges and risks in case of

failure (highly complex institutions). In general, a

highly complex institution is an institution (other

than a credit card bank) with more than $50

billion in total assets that is controlled by a parent

or intermediate parent company with more than

$500 billion in total assets, or a processing bank

or trust company with at least $10 billion in

total assets.

Both scorecards use quantitative measures that

are readily available and useful in predicting an

institution’s long-term performance to produce

two scores—a performance score and a loss

severity score—that will be combined and

converted to an initial assessment rate. The

performance score measures an institution’s

financial performance and its ability to withstand

stress. The loss severity score quantifies the relative

magnitude of potential losses to the FDIC in the

event of the institution’s failure. The rule will take

effect in the second quarter of 2011.

Temporary Liquidity Guarantee Program

On October 14, 2008, the FDIC announced

and implemented the Temporary Liquidity

Guarantee Program (TLGP). The TLGP consists

of two components: (1) the Debt Guarantee

Program (DGP)—an FDIC guarantee of certain

newly issued senior unsecured debt; and (2)

the Transaction Account Guarantee Program

(TAGP)—an FDIC guarantee in full of

noninterest-bearing transaction accounts.

Under the DGP, the FDIC initially guaranteed

in full, through maturity or June 30, 2012,

whichever came first, the senior unsecured debt

issued by a participating entity between October

14, 2008, and June 30, 2009, although in 2009

the issuance period was extended through October

31, 2009. The FDIC’s guarantee on each debt

instrument also was extended in 2009 to the

earlier of the stated maturity date of the debt or

December 31, 2012.

The FDIC charged a fee based on the amount

and term of the debt issued. Fees ranged from 50

basis points on an annualized basis for debt with

a maturity of 180 days or less, increasing to 75

basis points on an annualized basis for debt with a

maturity of 181 to 364 days and 100 basis points

on an annualized basis for debt with maturities

of 365 days or greater. In conjunction with the

program extension in 2009, the FDIC assessed

an additional surcharge on debt with a maturity

of one year or greater issued after April 1, 2009.

Unlike the other TLGP fees, which were reserved

for possible TLGP losses and not generally

available for DIF purposes, the surcharge was

deposited into the DIF and used by the FDIC

when calculating the reserve ratio of the Fund.

The surcharge varied depending on the type of

institution issuing the debt, with IDIs paying the

lower fees.

The TAGP initially guaranteed in full all domestic

noninterest-bearing transaction deposits held at

participating banks and thrifts through December

31, 2009. This deadline was extended twice and expired on December 31,

2010. The

guarantee also covered negotiable order of

withdrawal (NOW) accounts at participating

institutions—provided the institution initially

committed to maintain interest rates on the

accounts of no more than 0.50 percent (later

reduced to 0.25 percent) for the duration of

the program—and Interest on Lawyers Trust

Accounts (IOLTAs) and functional equivalents.

Participating institutions were initially assessed a

10 basis point surcharge on the portion of covered

accounts that were not otherwise insured. The fees

for the TAGP were increased at the first extension

to either 15 basis points, 20 basis points, or 25

basis points, depending on the institution’s deposit

insurance assessment category.

Program Statistics

Institutions were initially required to elect whether

to participate in one or both of the programs.

More than half of the over 14,000 eligible entities

elected to opt in to the DGP, while over 7,100

banks and thrifts, or 86 percent of FDIC-insured

institutions, initially opted in to the TAGP. Most

of the institutions that opted out of the DGP

had less than $1 billion in assets and issued no

appreciable amount of senior unsecured debt.

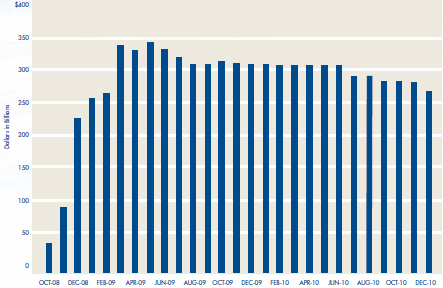

Over the course of the DGP’s existence, 121

entities issued TLGP debt. At its peak, the

DGP guaranteed almost $350 billion of debt

outstanding (see chart below). As of December

31, 2010, the total amount of remaining FDIC-guaranteed

debt outstanding was $267 billion.

The FDIC collected $10.4 billion in fees and

surcharges under the DGP. As of December 31,

2010, the FDIC paid $8 million on seven claims

that were filed when four participating entities

(all holding companies) defaulted on debt issued

under the DGP. Further claims on notes issued by

one entity are expected, since some of the notes

issued by this entity have not yet matured. Losses

through the end of the DGP guarantee period in

2012 are expected to be limited.

| OUTSTANDING TLGP DEBT BY MONTH |

|

|

Transaction Account Guarantee

Program Phase-Out

The TAGP was designed to eliminate potentially

disruptive shifts in deposit funding and thus

preserve bank lending capacity. The program

proved effective. However, because bank failures

continued to grow during 2009 and 2010, the

FDIC remained concerned that terminating the

TAGP too quickly could reverse the progress made

in restoring financial markets to more normal

conditions. To help transition institutions out of

the TAGP, therefore, the FDIC Board, on August

26, 2009, approved a final rule that extended

the TAGP for an additional six months, through

June 30, 2010, with higher assessment fees for

institutions participating in the extension period.

The final rule also provided an opportunity for

participating entities to opt out of the TAGP

extension. Over 6,400 institutions (or 93 percent

of institutions participating at year-end) elected to

continue in the TAGP.

In June 2010, the FDIC remained concerned that,

because of the lingering effects of the financial

crisis and recession, terminating the TAGP too

quickly could lead to liquidity problems for a

number of community banks. The Board therefore

approved a final rule authorizing another six-month

extension, until December 31, 2010, of

the TAGP. The FDIC did not increase assessment

fees with the second extension, but the final rule

reduced the permissible interest rate for the NOW

accounts covered by the guarantee to no higher

than 0.25 percent in order to better align the

program with prevailing market rates. The FDIC

provided institutions still participating in the

TAGP in the second quarter of 2010 with a one-time

opportunity to opt out of the second TAGP

extension, effective July 1, 2010. Almost 6,000

institutions (or 93 percent of those institutions

that were participating at the time) remained in

the TAGP. The final rule authorizing the second

extension also gave the FDIC Board the authority

to further extend the TAGP, without further

rulemaking, should economic conditions warrant

an additional extension, for a period of time not

to extend beyond December 31, 2011. However,

the passage of the Dodd-Frank Act eliminated the

need for such an extension of the TAGP.

Temporary Unlimited Coverage for

Noninterest-Bearing Transaction Accounts

under the Dodd-Frank Act

The Dodd-Frank Act provides temporary

unlimited deposit insurance coverage for

noninterest-bearing transaction accounts from

December 31, 2010 through December 31, 2012,

regardless of the balance in the account and the

ownership capacity of the funds. The unlimited

coverage is available to all depositors, including

consumers, businesses, and government entities.

The coverage is separate from, and in addition

to, the standard insurance coverage provided for

a depositor’s other accounts held at an FDIC-insured

bank.

A noninterest-bearing transaction account is a

deposit account where:

- Interest is neither accrued nor paid;

- Depositors are permitted to make transfers

and withdrawals; and

- The bank does not reserve the right to require

advance notice of an intended withdrawal.

The Act’s temporary unlimited coverage also

includes trust accounts established by an attorney

or law firm on behalf of clients, commonly known

as IOLTAs, or functionally equivalent accounts.

Money market deposit accounts (MMDAs) and

NOW accounts are not eligible for this temporary

unlimited insurance coverage, regardless of the

interest rate, even if no interest is paid.

Complex Financial Institution Program

The FDIC’s Complex Financial Institution

(CFI) Program addresses the unique challenges

associated with the supervision, insurance,

and potential resolution of large and complex

insured institutions. The FDIC’s ability to

analyze and respond to risks in these institutions

is of particular importance, as they make up a

significant share of the banking industry’s assets.

The Program provides for a consistent approach

to large-bank supervision nationwide, allows

for the analysis of financial institution risks

on an individual and comparative basis, and

enables a quick response to risks identified at

large institutions. The Program’s objectives are

achieved through extensive cooperation with the

FDIC’s regional offices, other FDIC divisions and

offices, and the other bank and thrift regulators.

Given the heightened risk levels stemming

from continued adverse economic and market

conditions, the FDIC has expanded its presence at

the nation’s largest and most complex institutions

through additional and enhanced on-site and off-site

monitoring.

The Program expanded coverage at large and

complex institutions from eight to ten in 2010

and increased its on-site presence, as designated

by the FDIC Board, to assess risk, monitor

liquidity, and participate in targeted reviews with

the primary federal regulators. In July 2010, the

FDIC entered into an interagency memorandum

of understanding (MOU) which allows FDIC

examiners to conduct special examinations of

certain institutions covered by the MOU. The

MOU should enhance the FDIC’s access to those

institutions and encourage ongoing effective

communication among the federal regulators.

The Large Insured Depository Institution (LIDI)

Program remains the primary instrument for

off-site monitoring of IDIs with $10 billion or

more in total assets, or under this threshold at

regional discretion. The LIDI Program provides a

comprehensive process to standardize data capture

and reporting through nationwide quantitative

and qualitative risk analysis of large and complex

institutions. As of June 30, 2010, the LIDI

Program encompassed 110 institutions with

total assets of $10.3 trillion. The LIDI Program

was refined again in 2010 to better quantify risk

to the insurance fund in all large banks. This

was accomplished, in collaboration with other

divisions and offices, through a revision to the

LIDI Scorecard, which better aligns with and

supports the FDIC’s large-bank deposit insurance

pricing responsibilities. The LIDI Scorecard is

designed to weigh key risk areas and provide a risk

ranking and measurement system that compares

IDIs on the basis of both the probability of failure

and exposure to loss at failure. The comprehensive

LIDI Program is essential to effective large bank

supervision by capturing information on the risks

and utilizing that information to best deploy

resources to high-risk areas, determine the need

for supervisory action, and support insurance

assessments and resolution planning.

Office of Complex Financial Institutions

The Office of Complex Financial Institutions

(OCFI) was created in 2010 to focus on the

expanded responsibilities of the FDIC by the

Dodd-Frank Act for the assessment of risk in

the largest, systemically important financial

institutions. The OCFI is responsible for oversight

and monitoring of large, systemically important

financial institutions (SIFIs). Specifically, through

both on-site and off-site monitoring, OCFI

will develop an in-depth understanding of the

operations and risk profiles of all IDIs and bank

holding companies with assets over $100 billion

and other companies designated as systemically

important by the Financial Stability Oversight

Council (FSOC).

Additionally, in conjunction with the Federal

Reserve, OCFI will develop regulations governing

the preparation, approval, and monitoring of resolution and recovery

plans developed by SIFIs

commonly referred to as “living wills.” OCFI will

be responsible for developing detailed resolutions

plans and strategies for assigned institutions.

OCFI will also identify and manage international

and cross-border issues that might complicate the

resolution process, and, accordingly, will build

and maintain relationships with key international

stakeholders.

In 2010, OCFI focused on creating and staffing

senior management positions. Work also began

on developing resolution strategies for specific

SIFIs and more broadly scoping a process,

strategies, and data needs for ongoing risk

assessment at SIFIs.

Center for Financial Research

The Center for Financial Research (CFR) was

founded by the Corporation in 2004 to encourage

and support innovative research on topics

important to the FDIC’s role as deposit insurer

and bank supervisor. During 2010, the CFR co-sponsored

three major conferences.

The 20th Annual Derivatives Securities and

Risk

Management Conference, which the FDIC

co-sponsored with Cornell University’s Johnson

Graduate School of Management and the

University of Houston’s Bauer College of Business,

was held in April 2010 at the Seidman Center.

The two-day conference attracted over 100

researchers from around the world. Conference

presentations focused on issues such as credit risk

measurement, equity option pricing, commodity

market speculation, and risk management.

In October 2010, the FDIC and the Federal

Reserve hosted a two-day symposium on

mortgages and the future of housing finance.

Over 300 experts from the public, private, and

academic sectors participated in discussions of

mortgage finance, foreclosures, loan modifications,

and securitizations. Federal Reserve Chairman Ben

Bernanke and FDIC Chairman Sheila Bair spoke

at the symposium regarding the need for reform

to restore stability to the housing finance system

and to aggressively examine the incentives of the

U.S. system of mortgage finance to ensure that the

problems that contributed to the financial crisis

are addressed.

The CFR and the Journal for Financial Services

Research (JFSR) hosted the 10th Annual Bank

Research Conference: Finance and Sustainable

Growth in October. The two-day conference

included the presentation of 17 papers and

was attended by over 100 participants. Experts

discussed a range of topics, including the global

financial crisis, credit derivatives and the default

risk of large complex financial institutions, and

bank capital adequacy.

International Outreach

The past year has been defined by broad

international efforts to respond effectively to the

causes of the global financial crisis. One of the

important lessons of the crisis is that effective

systems of deposit insurance are important not

only for the protection of individual depositors

but also for overall financial stability. Inadequate

systems of deposit insurance place individual

depositors at risk and can have a significant

negative impact on public confidence in the

financial system as a whole. The FDIC has

provided leadership and support to international

standard-setting organizations and international

financial institutions, and has established bilateral

agreements with other bank supervisory and

deposit insurance governmental organizations,

resulting in significant advancements in

promoting sound financial systems.

In 2009, the International Association of Deposit

Insurers (IADI) and the Basel Committee on

Banking Supervision (BCBS) jointly published

Core Principles for Effective Deposit Insurance

Systems (Core Principles). The Core Principles were

later adopted by the Financial Stability Board

(FSB), which added them to its Compendium of

Standards. Under the FDIC’s leadership, IADI,

BCBS, the International Monetary Fund (IMF),

the European Forum of Deposit Insurers (EFDI),

the World Bank, and the European Commission

collaborated in developing a methodology for

assessing compliance with the Core Principles.

The methodology was submitted for approval by the executive governing boards of IADI,

EFDI, and BCBS and presented to the FSB in

December 2010. Together, the Core Principles

and the methodology will be considered for

inclusion among the FSB’s 12 Key Standards

for Sound Financial Systems. Once adopted,

the Core Principles methodology is expected

to be used to assess deposit insurance systems

by the IMF in its Financial Sector Assessment

Program, and by the FSB in its peer review of

deposit insurance systems, which is scheduled for

2011. The leadership of IADI under Martin J.

Gruenberg, the Vice Chairman of the FDIC, has

been instrumental in advancing the establishment

of the Core Principles as the standards for deposit

insurance. Vice Chairman Gruenberg was re-elected

to serve as President of IADI and Chair

of the Executive Council in November 2010.

During his tenure as President, the membership

of IADI has grown from 48 to 62 deposit

insurance members, including new members from

Germany, Italy, Poland, Belgium, Switzerland,

Australia, and Paraguay.

The FDIC is integrally involved with the FSB’s

Cross Border Crisis Management Working

Group (CBCM). The group has been tasked with

evaluating options and making recommendations

on how to address issues related with the too-big-to-fail issue. In particular, the CBCM has been

focused on recovery and resolution (R&R) for

SIFIs. FSB member countries have been working

on preparing R&R plans for SIFIs domiciled in

their jurisdictions. The FDIC has been involved

in R&R planning for the top five U.S. firms and

has participated in Crisis Management Group

meetings hosted by foreign regulators. The

FDIC has also provided input and leadership

to the CBCM’s development of technical work

streams related to obstacles encountered in a

SIFI resolution. These work streams are focused

on booking practices, intragroup guarantees,

payments and settlement systems and legal

entities/management information systems.

Since January 2009, international regulators have

been meeting periodically to exchange views and

share information on developments related to

central counterparties (CCPs) for over-the-counter

(OTC) credit derivatives. Based on the success of

this cooperation, the OTC Derivatives Regulators’

Forum was formed to provide regulators with a

means to cooperate, exchange views, and share

information related to OTC derivatives, CCPs,

and trade repositories. FDIC staff has an active

role in the OTC Derivatives Regulators’ Forum

and the OTC Derivative Supervisors’ Group.

Work streams of particular interest include

collateral safekeeping practices, dispute resolution,

and the build out of the central clearing platforms.

Additionally, staff is completing a data access/user

agreement MOU to assure ready access to data in

trade repositories.

Throughout 2010, the FDIC participated in

Governors and Heads of Supervision and BCBS

meetings and contributed to the work streams,

task forces, and the Policy Development Group

that developed and refined regulatory forms to

address a new definition of capital, treatment of

counterparty credit risk, an international leverage

ratio, capital conservation and countercyclical

buffers, liquidity requirements, and surcharges

on SIFIs. The BCBS published the final capital

and liquidity reforms in December 2010,

along with the results of the comprehensive

quantitative impact study and an assessment of

the macroeconomic impact of the transition to

stronger capital and liquidity requirements. In

addition to these capital and liquidity reforms,

the FDIC also participated in BCBS initiatives

related to surveillance standards, remuneration,

supervisory colleges, operational risk, accounting

issues for consistency, and corporate governance.

The FDIC finalized a resolution and crisis

management MOU with the China Banking

Regulatory Commission (CBRC) in 2010. The

FDIC is currently in the process of negotiating

a similar MOU with the Swiss Financial Market

Supervisory Authority (FINMA). The MOU

with FINMA is expected to be finalized by the

end of 2011. The FDIC has reached out to other

strategic countries including India, and has been

met with enthusiasm by Indian officials. In 2011,

the FDIC will review its resolution MOU with

the Bank of England to determine what, if any, changes need to be made

in light of regulatory

developments both in the U.S. and the United

Kingdom.

The 2010 Strategic and Economic Dialogue

(S&ED) was held in Beijing, China, in May and

was the second such event held under President

Obama’s administration. President Barack Obama

and Chinese President Hu Jintao agreed to the

S&ED in April 2009 to deepen and promote

mutually beneficial cooperation between the U.S.

and China in key economic and strategic areas.

Chairman Bair and staff participated in this year’s

S&ED and also met with leaders of the People’s

Bank of China and the CBRC in side meetings to

further strengthen the FDIC’s relationship with

these bank regulatory agencies. During the

meeting with the CBRC, CBRC Chairman Liu

and Chairman Bair signed an MOU enhancing

cooperation in times of financial instability and in

cases of cross-border resolution.

Chairman Bair and staff visited New Delhi and

Mumbai, India, in June to meet with senior

representatives of public and private sector

organizations, including the Ministry of Finance,

the Reserve Bank of India (RBI), the Deposit

Insurance and Credit Guarantee Corporation,

and the National Bank for Agriculture and Rural

Development to discuss financial inclusion efforts

in the U.S. and India and to explore possible areas

of future cooperation between the two countries.

Chairman Bair was the keynote speaker at an

event hosted by the RBI, which was attended

by senior RBI officials, bankers, and financial

industry representatives. The Chairman’s speech

addressed U.S. financial regulatory reform, the

importance of promoting financial inclusion and

education, and the efforts made by both the U.S.

and India to reach their unbanked population.

Chairman Bair also announced plans to translate

the FDIC’s Money Smart program into Hindi for

use in India.

The FDIC continued to provide technical

assistance through training, consultations, and

briefings to foreign bank supervisors, deposit

insurance authorities, and other governmental

officials.

- The FDIC, on behalf of IADI, provided the

content and technical subject matter expertise

in the development of four tutorials released

through the Financial Stability Institute’s FSI

Connect: Premiums and Fund Management,

Deposit Insurance – Reimbursing Depositors

– Parts I and II, and Liquidation of Failed

Bank Assets. FDIC hosted two IADI executive

training seminars: Resolution of Problem

Banks (April) and Claims Management:

Reimbursement to Insured Depositors

(July). Over 125 deposit insurance and

bank regulatory officials from more than 35

countries attended the training programs. The

FDIC developed the IADI Capacity Building

Program website for organizations to use

for identifying available technical expertise

resources from IADI members. The website

was released in the fall of 2010.

- The FDIC hosted 87 visits with 580 visitors

from approximately 60 countries in 2010.

In July, Chairman Bair met with members

of the European Parliament’s Committee on

Economic and Monetary Affairs to discuss

U.S. financial regulatory reform and the

FDIC’s new authorities, SIFIs, and Basel II

reform. FDIC staff met with representatives

of Chinese authorities and banks on multiple

occasions throughout the year. Topics of

these meetings included discussions about

the health of the U.S. banking industry,

financial reform, FDIC supervision of banks,

the bank resolution process, and the FDIC’s

management of the distressed assets of failed

banks. The FDIC hosted a multi-day study

tour for the Board of Directors of the Nigeria

Deposit Insurance Corporation (NDIC) in

October. NDIC guests also traveled to the

New York Regional Office to learn about

the role of the regional offices and their

relationship with headquarters. The FDIC

hosted secondees, one from each of the

following organizations during 2010: the

Korea Deposit Insurance Corporation, the

Financial Services Commission in Korea, and

the Savings Deposit Insurance Fund of Turkey.

- June marked the three-year anniversary of the

secondment program agreed upon between the

Financial Services Volunteer Corps (FSVC)

and the FDIC to place one or more FDIC

employees full-time in FSVC’s Washington,

DC, office. Between September 2009 and

August 2010, FSVC hosted four secondees

who participated in 20 projects that took place

in Albania, Algeria, Egypt, Jordan, Malawi,

and Morocco. Additionally, the secondees

provided services for their counterparts in

Albania, Egypt, Libya, and Malawi from

Washington, DC, and completed a project

for the Central Bank of Iraq in Jordan. The

secondees worked directly with eight overseas

regulatory counterparts and trained almost

440 individuals. In these efforts, they spent

over 1,850 hours providing direct technical

assistance.

- The FDIC continues to support the work and

mission of the Association of Supervisors of

Banks of the Americas (ASBA). In furtherance

of the FDIC’s commitment to ASBA

leadership and strategic development, in July

2010, FDIC staff participated in ASBA’s

board of directors and technical committee

meetings. To facilitate ASBA’s research and

guidance initiatives, a senior bank examiner

will participate in ASBA’s Stress Testing

Working Group, and FDIC staff is responding

to ASBA’s review of the implementation of

International Financial Reporting Standards.

These research and guidance efforts are

intended to promote sound bank supervisory

practices among ASBA members.

|