Table of Contents

FDIC Contracting: Inclusion of Minority- and Women-Owned Businesses (MWOBs)

Employment at the FDIC: Increasing Representation of Minorities and Women

Introduction

Under the provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA) section 342, the Federal Deposit Insurance Corporation (FDIC) Office of Minority and Women Inclusion (OMWI) is required to submit to Congress an annual report regarding the actions taken by the agency toward hiring qualified minority and women employees and contracting with qualified minority- and women-owned businesses.

The FDIC is pleased to submit this 2017 Report to Congress. The report describes the FDIC’s activities relating to the inclusion of minorities and women in contracting and hiring for the year, as well as other relevant information, including the agency’s activities supporting financial access, economic inclusion, and financial literacy. Consistent with the provisions of section 342 of the DFA, the FDIC continues to enhance its long-standing commitment to promote diversity and inclusion in employment opportunities and all business areas of the FDIC. This report outlines both successes and challenges in contracting and hiring as the agency works to ensure that these efforts are reflected in its operations.

Commitment to Diversity and Inclusion

The mission of the FDIC is to preserve and promote public confidence in the U.S. financial system by insuring deposits, examining and supervising financial institutions for safety and soundness and consumer protection, making large and complex financial institutions resolvable, and managing receiverships. In 1999, the FDIC published its first Diversity Strategic Plan, which outlined its commitment to recruiting and retaining the most qualified, talented, and motivated employees in the labor market. OMWI is an important component in these efforts and supports the FDIC’s mission through the pursuit of equal employment opportunity, affirmative employment initiatives, diversity and inclusion, and outreach efforts to ensure the fair inclusion and utilization of minority- and women-owned businesses, law firms, and investors in contracting and investment opportunities.

In 2012, the FDIC Chairman established performance goals to update the Diversity Strategic Plan and asked each division and major office to develop strategic plans that identify steps to promote increased diversity through the FDIC’s recruiting and hiring processes. Since 2013, the FDIC has annually updated the Diversity and Inclusion Strategic Plan to ensure the plan remains current and relevant. The Diversity and Inclusion Strategic Plan was updated in 2016 to continue the FDIC’s efforts in this important area and to address the FDIC’s goals to develop and implement a more comprehensive, integrated, and strategic focus on diversity and inclusion. The 2017 Diversity and Inclusion Strategic Plan was disseminated to the FDIC workforce and posted externally to the public on www.fdic.gov.

The Diversity and Inclusion Strategic Plan continues to outline a course for promoting workforce diversity by recruiting from a diverse, qualified group of potential applicants, and cultivating workplace inclusion through collaboration, flexibility, and fairness. The plan also ensures the sustainability of the FDIC’s diversity and inclusion efforts by equipping leaders with the ability to manage diversity, monitor results, and refine approaches on the basis of actionable data. There are specific steps outlined in the plan that continue to enhance diversity and inclusion at the FDIC in the areas of leadership engagement, analytics and reporting, training, communications, strategic planning, and program enhancement.

When the FDIC Board of Directors created OMWI in 2011, the Board also established an OMWI Steering Committee to ensure and promote coordination of OMWI programs. In 2013, the OMWI Steering Committee was renamed the FDIC Diversity and Inclusion Executive Advisory Council (EAC). The EAC is chaired by the FDIC Deputy to the Chairman and Chief Operating Officer/Chief of Staff and includes the OMWI Director, FDIC division and office directors, and other key FDIC senior staff. The EAC provides leadership on diversity and inclusion initiatives throughout the FDIC. The EAC also reviews the Diversity and Inclusion Strategic Plan annually, and updates it as needed to improve the agency’s efforts in promoting diversity and inclusion on an ongoing basis.

2017 Diversity and Inclusion Initiatives

Annually, the FDIC Chairman issues a number of performance goals designed to further promote diversity, inclusion, and equal employment opportunity at the agency. One of these goals required the agency’s division and major office directors to develop customized strategic plans for their organizations to identify steps to promote increased diversity throughout the FDIC. Again in 2017, each division and major office assessed available workforce data and produced plans with strategies to further their diversity progress and address noted issues. The division and office level plans were consolidated into an FDIC Plan to Promote Increased Diversity through Division/Office Engagement and have been integrated into the agency’s annual strategic planning efforts. In May 2017, the progress made by divisions and major offices was reported and discussed at the monthly EAC meeting. This process keeps the division and major offices engaged in the FDIC’s diversity and inclusion efforts and will continue in 2018.

The FDIC is committed to continually providing all employees with a work environment that promotes excellence and acknowledges and honors the diversity of its employees. The Diversity and Inclusion Strategic Plan was revised during 2017 and will be disseminated to the FDIC workforce and posted on the FDIC website in 2018. The revised Diversity and Inclusion Strategic Plan is designed to continue the FDIC’s success in ensuring all employees are valued members of the workplace and active participants in carrying out the FDIC mission.

In recognition of the FDIC’s 2017 diversity and inclusion progress, the following initiatives are highlighted:

The FDIC supported the establishment of an additional Employee Resource Group, the Corporate Advocacy Network for Disability Opportunities (CAN DO), and continued to support and encourage collaboration with the five existing ERGs: Veterans Employee Resource Group; Emerging Leaders; Hispanic Organization for Leadership and Advancement; PRIDE; and Partnership of Women in the Workplace. ERGs are networks of FDIC employees with similar interests.

OMWI awarded a contract to provide diversity and inclusion training for employees in an online environment. OMWI continued administering manager and supervisor training on equal employment opportunity and diversity and inclusion, the No FEAR Act biennial training, and a webinar on retaliation

The FDIC continued to implement innovative procurement strategies on several contracts to foster increased minority- and women-owned business participation in contracting opportunities.

- The FDIC’s Workplace Excellence (WE) program, composed of a national WE

Steering Committee and division/office WE Councils, continued the focus on

maintaining, enhancing and institutionalizing a positive workplace environment

throughout the agency. OMWI worked closely with WE to develop and provide

recommendations related to fairness, diversity and inclusion, to include:

Conducting and presenting a trend analysis of Federal Employee Viewpoint Survey results and trends delineated by FDIC dimension and minority, gender, ethnicity, and disability status; and

Participating in a joint Fairness, Diversity and Inclusion Working Group composed of WE Steering Committee, Council, and Chairman’s Diversity Advisory Council members to conduct focus groups and further evaluate available information in an effort to better understand how employees in different demographic groups view the FDIC workplace.

-

The FDIC continued to develop and implement the Workforce Development Initiative (WDI) designed to address comprehensive succession planning needs and workforce development challenges and opportunities, and to develop future FDIC leaders. As a part of the initiative, OMWI:

Continued to track succession planning review results by race, ethnicity, and gender – and provide the results to WDI program management;

Provided guidance as needed about potential diversity and inclusion issues in other WDI programs (e.g., career paths, external details, learning, development and training, leadership mentoring, administrative career paths; manager rotations, and onboarding); and,

Expanded the succession planning review to additional grade levels.

FDIC Contracting: Inclusion of Minority- and Women-Owned Businesses (MWOBs)

The FDIC places a high priority on achieving diversity in contracting and asset sales, and OMWI is an integral part of the contractor solicitation, education, and evaluation process. During 2017, the FDIC implemented new contracting initiatives and conducted focused outreach which improved MWOB participation in its contracting activities. However, the FDIC continued to face challenges in increasing the utilization and growth rates for MWOB contractors because new contract awards by the FDIC have been declining since the height of the financial crisis and non-financial goods and services contracts for recurring needs represent a larger percentage of FDIC contracts. The FDIC will analyze future contracting needs to determine where MWOB opportunities may exist and if new procurement strategies can be used to maximize MWOB participation. The following sections provide detailed information on the agency’s 2017 contracting activities and successes; contracting initiatives, programs, and outreach; and challenges the FDIC faces in increasing MWOB participation in its contracting activities.

Contracting Activities and Successes

FDIC Procurement Policies

The FDIC’s contracts are typically awarded through a competitive, best-value solicitation process that involves consideration of both the offeror’s technical and price proposals. The solicitations describe what offerors must include in their proposals and the proposal evaluation criteria specific to the good or service being procured. Proposals are evaluated and rated by a panel of FDIC subject matter experts and include an OMWI representative. Awards are made to the offeror that provides the best value to the FDIC.

For any contract over $100,000, OMWI review is required to identify competitive minority- and women-owned businesses to include in contract solicitations. As part of this process, OMWI uses the FDIC’s Contractor Resource List (CRL) that includes registered MWOBs. The CRL is the principal database for vendors interested in doing business with the FDIC. OMWI also identifies qualified MWOBs through the System for Award Management and the Minority Business Development Agency. This process helps ensure that a diverse pool of contractors is solicited and considered for each major contract.

The FDIC’s website1 provides information, announcements, and technical assistance for minority- and women-owned businesses, law firms, and investors seeking to do business with the FDIC. The FDIC also has a small business resource page that contains more than 40 learning modules2 and is a technical assistance aid and selfassessment for businesses interested in competing for contract opportunities.

1. See www.fdic.gov/mwop/.

2. See www.fdic.gov/about/diversity/sbrp/index.html.

Contract Payments with MWOBs

The FDIC paid $414.0 million to contractors in 2017 under 1,537 contracts, of which $109.6 million (26.5 percent) was paid to MWOBs under 354 contracts. [See Figure 1.] By comparison, the FDIC paid $415.2 million to contractors under 1,786 contracts in 2016; $507.2 million to contractors under 2,029 contracts in 2015; $491.6 million to contractors under 1,962 contracts in 2014; and $553.7 million to contractors under 1,982 contracts in 2013. The 2017 total payments (i.e., spend) to contractors included payments for contracts awarded in 2017 and payments for active contracts awarded prior to 2017.

| Figure 1 Contracting Payments (in millions) | |||||

|---|---|---|---|---|---|

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| Total | $553.7 | $491.6 | $507.2 | $415.2 | $414.0 |

| 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | |

| MWOB | $140.6 | $128.2 | $142.5 | $111.5 | $109.6 |

| 25.4% | 26.1% | 28.1% | 26.8% | 26.5% | |

| Minority Owned (MO) | $102.9 | $89.3 | $89.3 | $56.0 | $54.6 |

| 18.6% | 18.2% | 17.6% | 13.5% | 13.2% | |

| Women Owned (WO) | $63.7 | $63.6 | $83.2 | $66.8 | $66.9 |

| 11.5% | 12.9% | 16.4% | 16.1% | 16.2% | |

| Overlap (Both MO & WO) | $26.0 | $24.7 | $30.0 | $11.3 | $11.9 |

| 4.7% | 5.0% | 5.9% | 2.8% | 2.9% | |

| Asian American | $50.3 | $38.5 | $39.9 | $33.5 | $30.1 |

| 9.1% | 7.9% | 7.9% | 8.1% | 7.2% | |

| Black American | $19.8 | $15.9 | $13.3 | $11.5 | $14.2 |

| 3.6% | 3.2% | 2.6% | 2.8% | 3.4% | |

| Hispanic American | $26.0 | $26.7 | $25.1 | $10.3 | $9.5 |

| 4.7% | 5.4% | 5.0% | 2.5% | 2.3% | |

| Native American | $1.2 | $0.3 | $0.1 | $0.1 | $0.2 |

| 0.2% | 0.1% | 0.0% | 0.0% | 0.1% | |

For purposes of contract payment information, the FDIC considers an active contract one in which payments were made or credits applied in 2017. In 2017, minority-owned firms were paid $ 54.6 million of the total dollars paid to contractors (13.2 percent). Women-owned firms were paid $66.9 million of the total dollars paid to contractors (16.2 percent). These two categories – minorities and women – are not mutually exclusive since $11.9 million (2.9 percent) was paid in 2017 to businesses classified as both minority-owned and women-owned. By contrast, the FDIC paid MWOBs $111.5 million (26.8 percent) of the total paid to all contractors in 2016 under 461 contracts; $142.5 million (28.1 percent) of the total paid to all contractors in 2015 under 591 contracts; $128.2 million (26.1 percent) to MWOBs in 2014 under 533 contracts; and $140.6 million (25.4 percent) to MWOBs in 2013 under 608 contracts.

In 2017, the FDIC awarded 210 contracts to MWOBs out of a total of 737 issued (28.5 percent). [See Figure 2.] By comparison, the FDIC awarded 287 contracts (24.3 percent) to MWOBs out of a total of 1,181 issued in 2016; 346 contracts (29.9 percent) to MWOBs out of a total of 1,159 issued in 2015; 288 contracts (26.9 percent) to MWOBs out of a total of 1,072 issued in 2014; and 282 contracts (28.3 percent) to MWOBs out of a total of 995 issued in 2013.

| Figure 2 Contracting Actions | |||||

|---|---|---|---|---|---|

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| Total | 995 | 1072 | 1159 | 1181 | 737 |

| 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | |

| MWOB | 282 | 288 | 346 | 287 | 210 |

| 28.3% | 26.9% | 29.9% | 24.3% | 28.5% | |

| Minority Owned (MO) | 161 | 170 | 148 | 142 | 100 |

| 16.2% | 15.9% | 12.8% | 12.0% | 13.6% | |

| Women Owned (WO) | 162 | 167 | 243 | 187 | 151 |

| 16.3% | 15.6% | 21.0% | 15.8% | 20.5% | |

| Overlap (Both MO & WO) | 41 | 49 | 45 | 42 | 41 |

| 4.1% | 4.6% | 3.9% | 3.5% | 5.6% | |

| Asian American | 39 | 54 | 56 | 62 | 63 |

| 3.9% | 5.1% | 4.8% | 5.2% | 8.6% | |

| Black American | 50 | 45 | 35 | 24 | 22 |

| 5.0% | 4.2% | 3.0% | 2.0% | 3.0% | |

| Hispanic American | 61 | 59 | 39 | 48 | 4 |

| 6.2% | 5.5% | 3.4% | 4.1% | 0.5% | |

| Native American | 0 | 2 | 1 | 2 | 7 |

| 0.0% | 0.2% | 0.1% | 0.2% | 1.0% | |

| Other | 11 | 10 | 17 | 6 | 4 |

| 1.1% | 0.9% | 1.5% | 0.5% | 0.5% | |

As of December 31, 2017, the FDIC had 269 (17.3 percent) active contracts with MWOBs out of a total of 1,552 active contracts. The active contracts to MWOB firms by category were as follows: Asian American (87), Black American (41), Hispanic American (20), Native American (8), and Women (162). These include contracts awarded to firms that were both minority-owned and women-owned.

Contract Awards with MWOBs

The FDIC awarded contracts with a combined value of $523.7 million in 2017, of which $96.7 million (18.5 percent) were awarded to MWOBs. By comparison, the FDIC awarded contracts with a combined value of $508.8 million in 2016, with $93.9 million (18.5 percent) awarded to MWOBs; awarded $858.4 million in 2015, with $211.6 million (24.7 percent) awarded to MWOBs; awarded contracts with a combined value of $686.8 million in 2014, with $239.9 million (34.9 percent) awarded to MWOBs; and awarded contracts with a combined value of $572.8 million in 2013, with $198.7 million (34.7 percent) awarded to MWOBs. [See Figure 3.]

| Figure 3 Total Contract Dollar Awards | |||||

|---|---|---|---|---|---|

| 2013 | 2014 | 2015 | 2016 | 2017b | |

| Total | $572.8 | $686.8 | $858.4 | $508.8 | $523.7 |

| 100.0% | 100.0% | 100.0% | 100.0% | 100% | |

| MWOB | $198.7 | $239.9 | $211.6 | $93.9 | $96.7 |

| 34.7% | 34.9% | 24.7% | 18.5% | 18.5% | |

| Minority Owned (MO) | $158.5 | $143.7 | $145.2 | $56.5 | $66.7 |

| 27.7% | 20.9% | 16.9% | 11.1% | 12.7% | |

| Women Owned (WO) | $66.1 | $132.6 | $104.2 | $47.4 | $46.2 |

| 11.5% | 19.3% | 12.1% | 9.3% | 8.8% | |

| Overlap (Both MO & WO) | $25.9 | $36.4 | $37.8 | $10.0 | $16.2 |

| 4.5% | 5.3% | 4.3% | 1.9% | 3.0% | |

| Asian American | $38.0 | $27.1 | $51.8 | $25.0 | $31.2 |

| 6.7% | 4.0% | 6.0% | 4.9% | 6.0% | |

| Black American | $32.2 | $21.3 | $30.7 | $9.4 | $32.7 |

| 5.6% | 3.1% | 3.6% | 1.9% | 6.2% | |

| Hispanic American | $85.3 | $66.1 | $43.2 | $20.6 | $1.6 |

| 14.9% | 9.6% | 5.0% | 4.0% | 0.3% | |

| Native American | $- | $0.8 | $- | $0.1 | $0.9 |

| 0.0% | 0.1% | 0.0% | 0.0% | 0.2% | |

| Other | $3.0 | $28.4 | $19.5 | $1.4 | $0.3 |

| 0.5% | 4.1% | 2.3% | 0.3% | 0.0% | |

The FDIC’s five-year trend from 2013-2017 of contract awards and payments can be found at Appendix A.

Contract Awards by North American Industry Classification System

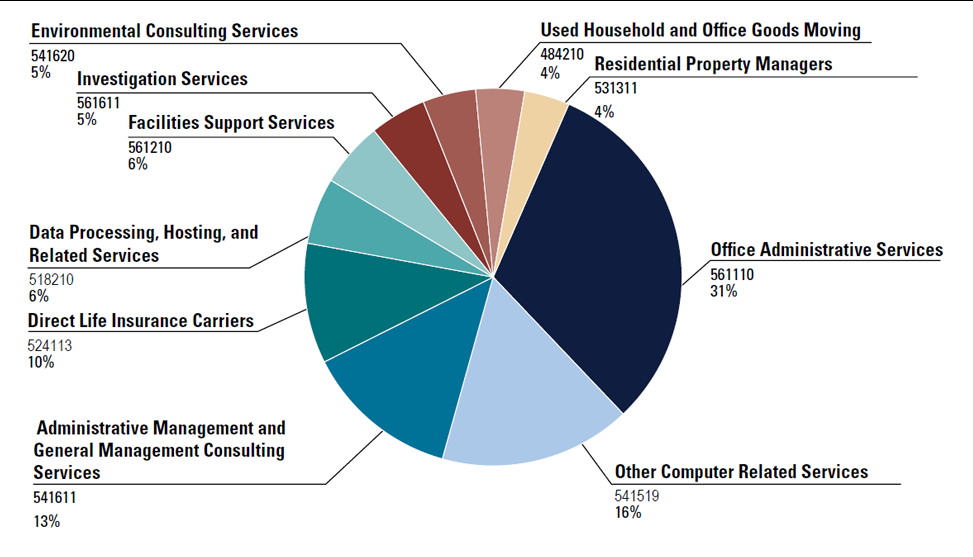

The North American Industry Classification System (NAICS) was developed by the Office of Management and Budget (OMB) and is the standard used by federal statistical agencies in classifying business establishments for the purpose of collecting, analyzing, and publishing statistical data related to the U.S. business economy. The FDIC awarded contracts in 2017 under 62 different NAICS codes. Figure 4 depicts the distribution of the FDIC’s 2017 contracts categorized for the top ten NAICS codes.

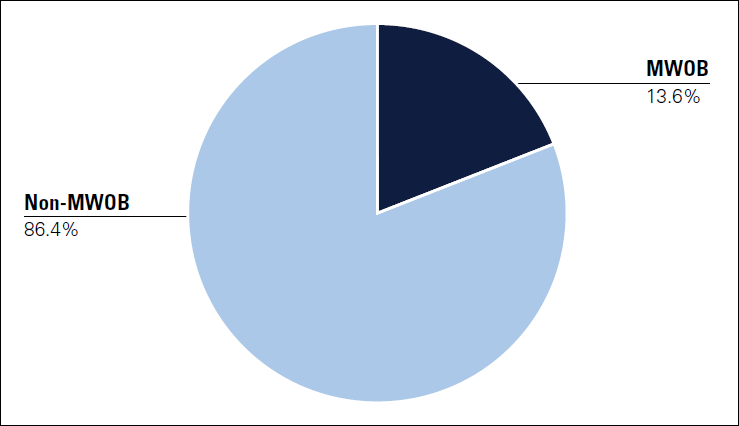

In 2017, these awards consisted of the following: 31 percent for office administrative services; 16 percent for other computer related services; 13 percent for administrative management and general management consulting services; and 10 percent for direct life insurance carriers. The remaining 30 percent – each six percent or under – were awarded in the areas of data processing, hosting, and related services (six percent); facilities support services (six percent); investigation services (five percent); environmental consulting services (five percent); used household and office goods moving (four percent); and residential property managers (four percent). Collectively, 13.6 percent of the top ten NAICS code contracts were awarded to MWOBs. [See Figure 5.]

The 2017 FDIC contract awards associated with the top ten NAICS codes can be found in Appendix B.

Referrals to Law Firms

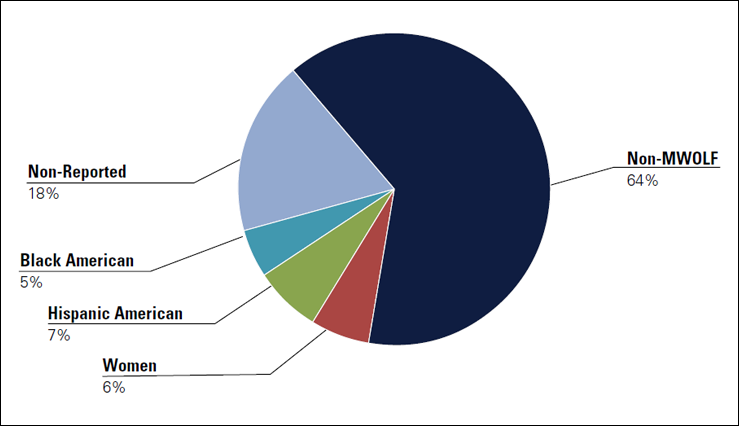

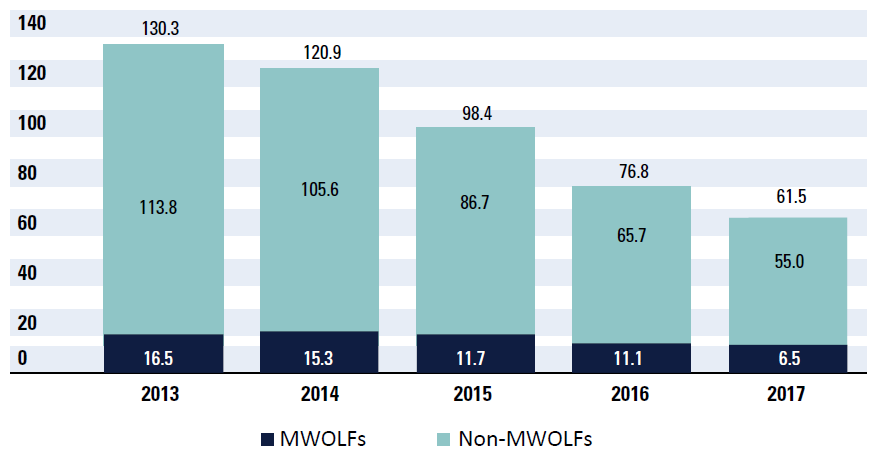

Referrals to law firms are typically made on a competitive basis. Price, expertise, capacity, and status are among the criteria considered in making the selections. The FDIC made 363 referrals to outside counsel in 2017, of which 67 (18.0 percent) were minority- and women-owned law firms (MWOLFs), compared to a total of 342 referrals, of which 151 (44.2 percent) were to MWOLFs in 2016. Referrals to MWOLFs in 2017, by category, were as follows: Black American – 17(5.0 percent), Hispanic American – 26 (7 percent), Native American – 1 (<1 percent), Asian American – 1 (<1 percent), and Women – 22 (6 percent). [See Figure 6]

The FDIC paid $61.5 million to outside counsel in 2017, as compared to $76.8 million in 2016. [See Figure 7.] The FDIC paid $6.5 million to MWOLFs in 2017, which represents 10.6 percent of the total paid to all law firms. This percentage is below that of 2016, during which the FDIC paid a total of $11.1 million to MWOLFs, which was 14.5 percent of the total paid to all law firms that year.

As noted above, there was a decline in referrals to outside counsel in 2017. Bank resolution activities, which are a major source of outside counsel work, decreased from 2016 to 2017. This decrease is consistent with the overall decline in FDIC fees spent on outside counsel since the peak levels in 2013. The FDIC remains committed to seeking ways to increase the level of referrals to MWOLFs in 2018.

Outreach to MWOLFs

Anticipating a decline in legal referrals in 2017, the Legal Division tailored its outreach strategy to focus on the substantive areas of the FDIC’s legal work that posed the greatest opportunities for MWOLF participation. The most important source of legal contracting opportunities lies with the FDIC in house counsel. To that end, the Legal Division continued to work closely with in-house attorneys in areas that account for a substantial dollar amount of legal referrals. The Legal Division continued to emphasize the importance of diverse staffing of legal contracts. For example, the Legal Division held an MWOLF Outreach Workshop in the Dallas Regional Office for those in house FDIC attorneys who assign work to outside counsel. The purpose of the workshop was to highlight the importance the Dallas Regional Office referrals are to MWOLFs in enhancing participation in legal contracting. The event included a roundtable discussion about successes and challenges in the use of MWOLF firms.

Another critical element of the Legal Division MWOLF outreach is the FDIC’s partnerships with minority bar associations and stakeholder organizations. In 2017, Legal Division staff attended seven bar association conferences as well as, two stakeholder events sponsored by the National Association of Minority and Women Owned Law Firms (NAMWOLF) in support of maximizing MWOLF participation in FDIC legal contracting. At many of these events, the Legal Division counsels MWOLFs on how those firms can make strategic decisions in their pursuit of FDIC legal work, and works with other large corporate clients. At one stakeholder event, the Legal Division participated in a panel designed to teach MWOLF firms how to make presentations to prospective clients. Also, in September 2017, the Legal Division as well as the Acting Director, OMWI, attended the National NAMWOLF annual meeting where NAMWOLF awarded the Legal Division its prestigious Diversity Initiative Achievement Award recognizing the FDIC’s long-term efforts in maximizing the participation of MWOLFs in legal contracting. The FDIC was selected from five finalists, including JPMorgan Chase, Shell, and Walmart – all Fortune 500 companies.

Pursuant to Section 342 of the Dodd-Frank Act, which requires an assessment of legal contractors’ internal workforce diversity practices, the Legal Division refined and continued to implement a system of compliance reviews of the top ten billing law firms (both majority-owned and MWOLFs). This program provides the Legal Division another means to address diversity and inclusion and provides opportunities for women and minority attorneys seeking to provide services. These on-site visits are designed to engage firms in discussions about best practices, diversity staffing concepts, metrics and the FDIC’s MWOLF program. The results continue to be positive. The Legal Division collected baseline diversity metrics, reviewed best practices on staffing of client matters, and reached a commitment with various firms to increase diversity concerning FDIC activities.

In addition to the outreach efforts noted above, the Legal Division continues to provide technical assistance to the National Association of Credit Unions and other related government agencies on developing MWOLF outreach programs that mirror FDIC’s program. The Legal Division evaluated and approved nine (9) new MWOLF applications in 2017. Firms from various geographic areas were added to the FDIC List of Counsel Available in order to be eligible to receive legal contracting work.

Contracting Initiatives, Programs and Outreach

FDIC awarded 737 new contracts with a combined value of $523.7 million in 2017. These totals represent the fewest number of awarded contracts by the FDIC since 2008, and the second lowest total contract dollars awarded since 2007. As stated in prior year reports, the FDIC annual contract awards and total contract dollars awarded have fallen since the height of the financial crisis due to a significant reduction in annual bank failures. During the financial crisis, contracts related to services required to resolve failed banks represented up to 85 percent of all FDIC contract dollars awarded in a given year. In 2017, only 33.5 percent of FDIC total contract dollars awarded supported the FDIC’s Division of Resolutions and Receiverships in their mission to resolve failed banks.

As a result, the FDIC continued to identify contracting opportunities for MWOBs in non-financial goods and services requirements. For example, contracts were awarded to MWOBs in the following areas: IT software development and maintenance services; IT security services; IT hardware and software licenses; training services; contracting support services; leadership and mentoring services; facilities management services; physical security support services; translation services; and audit services.

However, despite the continuation of fewer annual bank failures since the height of the financial crisis, the FDIC continued to include MWOBs in the procurement process for the financial services contract opportunities that arose. Several of the contracts used to perform failed bank resolution services during the financial crisis expired in 2017. The FDIC’s strategy is to re-bid these contracts as they expire to ensure contractor resources are in place when needs arise. MWOB contractors were instrumental to the FDIC’s success during the financial crisis. As a result, the FDIC focused on ensuring continued MWOB participation in the re-competition of these expiring contracts. MWOB firms were awarded new contracts in 2017 for mortgage servicing rights services, financial advisory services for complex securities, and temporary staffing services. Additional existing failed bank resolution contracts will expire in 2018 and beyond. The FDIC will continue to look for opportunities to include MWOBs in the recompetition of these mission critical services.

Lastly, FDIC continued to discuss procurement strategies and MWOB contracting issues at monthly EAC meetings attended by senior managers from FDIC divisions and offices. The FDIC also continued to implement the recommendation to hold pre-proposal conferences to ensure businesses understand the FDIC’s requirements before a solicitation is issued and to give smaller businesses opportunities to find partners and develop teams before submitting bids.

Information Technology Contracting

The FDIC recognized in 2012 that the declining number of bank failures would result in a significant shift in new contract award opportunities from bank resolution contracts to contracts for daily operations (e.g., IT software development and maintenance, facilities management, etc.). The FDIC conducted focused market research in 2012 to ensure significant MWOB participation in the then upcoming $546.8 million competitive Basic Ordering Agreement (BOA) for the second generation Information Technology Application Services (ITAS II) contract. This focused market research led to six MWOB firms being awarded an ITAS II BOA out of 11 total firms awarded the BOA (55 percent). The six BOA awards to MWOBs represented a significant increase in MWOB awards from the ITAS I BOA where only one MWOB firm was awarded the BOA out of four total firms (25 percent). In 2016, the FDIC conducted a competition to add additional firms to the ITAS II BOA to increase the number of vendors under the contract. Once again, significant market research was conducted to ensure MWOB participation in the competitive process. The end result was three additional firms were added to the ITAS II BOA with two of the firms being MWOB firms. This increased the total number of firms under the ITAS II BOA from 11 to 14 and the total number of MWOB firms under the ITAS II BOA from six to eight. As a result, the percentage of MWOB firms under the BOA increased from 55 to 57 percent. The assignment of work to contractors under the ITAS II BOA is accomplished through the award of task orders that are competed among the contractors awarded the BOA. A significant number of multi-year task order awards were made under ITAS II between 2013 and 2015 resulting in fewer requirements for new task orders in 2017. However, three of the six new task orders awarded in 2017 under ITAS II were awarded to MWOB firms with a combined value of $2.6 million. This represented 50 percent of the total task orders awarded in 2017 and 46.5 percent of the total dollars awarded under ITAS II during 2017.

ITAS II is not the only contract that supports the FDIC’s Information Technology program. One of the three BOAs awarded in 2017 under the FDIC’s $4 million cyber security support services program was awarded to an MWOB firm. In addition, two new contracts with a combined value of $964,180 were awarded to MWOBs in 2017 to provide Enterprise File Integrity Manager Support and IT services for a legal hold project.

Lastly, the FDIC also recognizes that IT hardware and software can often be provided by resellers certified by the manufacturer or by MWOB manufacturers. As a result, the FDIC continued with the strategic decision to solicit MWOBs for hardware and software purchases when possible. This strategy resulted in 78 contract awards to MWOBs with a combined value of $15.0 million.

Facilities Management and Security Support Services

Significant awards to MWOBs in facilities management and security support services included contracts valued at $18 million for physical security support services; $1.5 million for janitorial services; $49,676 for davit repair services; $44,900 for electrical maintenance services; $41,263 for hardware; and $24,700 for lease audit services.

In addition, the FDIC continued to provide opportunities to MWOBs for both new and replacement furniture. In total, four contracts with a combined value of $596,425 were awarded to MWOBs to provide furniture for FDIC locations nationwide.

Human Resources Management

A $323,937 contract to provide important leadership training, mentoring training, and program support services was awarded to an MWOB in 2017.

Contracting Support Services

A $556,418 contract was awarded to an MWOB firm to provide and maintain the Contractor Resource List (CRL) system. The CRL is an on-line tool where vendors provide information on the types of goods and services they offer, and it is used by FDIC staff to identify potential sources for competitive procurements.

Bank Resolution Contracts

There were only eight bank failures of financial institutions in 2017, which was far below the annual number of bank failures that occurred during the financial crisis between 2008 and 2013 when failures ranged from 24 to 157 per year. However, there are still hundreds of active failed bank receiverships from prior year failures. The FDIC continued to award contracts to MWOBs to provide required services to resolve new 2017 bank failures and to support on-going work required from prior year bank failures. In 2017, 105 contracts with a combined value of $55.0 million were awarded to MWOBs to provide the required financial services to assist the FDIC in resolving failed banks. Contracts awarded to MWOBs included, but were not limited to, financial and management reporting services; IT development services; independent thirdparty security assessment services; mortgage servicing rights services; financial advisory services for complex securities; temporary staffing services; profit sharing plan audit services; receivership assistance services; loss share agreement monitoring services; asset valuation services; appraisal management services; environmental support services; tax return preparation services; accounting services; and translation/ transcreation/interpreter services. Of note was a procurement strategy change for the re-bid of the IT development, financial management, and reporting services contract. Previously these services were provided by a single contract. In order to increase competition and opportunities for MWOB firms to participate, the FDIC split these services and re-bid them as two stand-alone contracts. Both new contracts were awarded to MWOBs.

Other Significant MWOB Contract Awards

Recognizing the need to expand MWOB contract awards beyond services for bank resolutions, information technology, human resources, and facilities management, the FDIC looked for MWOB opportunities in other program areas. The FDIC’s Corporate University awarded three contracts with a combined value of $1.1 million to MWOB firms to provide training to FDIC employees on a variety of subjects. The FDIC’s Division of Depositor and Consumer Protection awarded a contract with a value of $509,136 to an MWOB firm to provide Money Smart computer based training services, and a $275,000 contract to an MWOB firm to provide translation/transcreation/ interpreter services. The Office of Minority and Women Inclusion awarded a $66,175 contract to an MWOB firm to provide diversity and inclusion training.

Outreach to MWOBs

IIn 2017, the FDIC participated in a combined total of 35 business expos, one-on-one matchmaking sessions, and panel presentations. At these events, the FDIC staff provided information and responded to inquiries regarding the FDIC’s business opportunities for minorities and women. In addition to targeting MWOBs, Minority and Women Owned Investors, and MWOLFs, these efforts also targeted veteran-owned and small disadvantaged businesses. Vendors were also encouraged to register through the FDIC’s CRL.

OMWI co-hosted two Technical Assistance Events with the Office of the Comptroller of the Currency (OCC) and the National Credit Union Administration (NCUA). The Cybersecurity Awareness and Preparedness for Your Business event discussed cybersecurity intrusions in small businesses and what to do when a business is compromised. Cybersecurity requirements for financial institutions were discussed as well as vendors’ expectations and requirements. One-hundred five (105) individuals attended the event.

The FDIC, NCUA, and OCC in collaboration with the Virginia Procurement Technical Assistance Program hosted the Proposal to Pricing – Developing a Winning Strategy technical assistance event. The presenters shared information on developing winning proposals and pricing strategies. The sponsoring agencies and various procurement trade organizations also exhibited at the event. One-hundred thirty-five (135) individuals attended the event.

FDIC Asset Sales

During 2017, OMWI and the Division of Resolutions and Receiverships (DRR) collaborated to present two FDIC-sponsored asset purchaser workshops that were marketed extensively to minority- and women-owned investors and companies interested in learning about DRR’s sales processes. DRR speakers with strong backgrounds in their respective programs provided details on the various tools used by DRR to market assets and presented information to attendees on how to participate in the transactions and bid on assets offered for sale.

The outreach events were held in 2017, in New Orleans, Louisiana to support asset sales resulting from the failure of First NBC Bank. The first event was an investor workshop which included discussions of cash loan sales, structured transactions, real estate liquidations and other forms of FDIC dispositions. The investor workshop attracted 104 attendees.

The second event was conducted by Owned Real Estate (ORE) staff and was targeted to first-time homebuyers, tenants occupying non-owner occupied ORE, and other prospective purchasers of ORE in the New Orleans area. Housing counselors and lenders specialized in lower-priced home loans were available to help the 79 event attendees. Information regarding the Minority and Women Outreach Program can be found on the FDIC’s website at www.fdic.gov/mwop/.

The FDIC’s Homeownership Outreach Workshop focused on attendees receiving information on how and why the FDIC acquires properties, the types of properties, and where the properties are listed. At the conclusion of the workshop, the agency hosted a Housing Fair session where attendees met with representatives of financial institutions and non-profit organizations.

Challenges

As noted, the FDIC’s annual number of new contracts awarded and total contract dollars awarded has declined significantly since the height of the financial crisis due to the significant reduction in the number of bank failures. From 2009 to 2012, the FDIC’s annual contract awards ranged between $1 billion and $2.6 billion. The total combined value of the FDIC’s 2017 contract awards of $523.7 million represents the second lowest combined total of new contract dollars awarded since 2007. The 737 new contracts awarded in 2017 represents the fewest number of contract awards by FDIC since 2008. Non-financial goods and services contracts for supporting daily operations are continuing to represent a larger percentage of the FDIC’s annual contract awards. In years when there are few bank failures, these non-financial often recurring goods and services contracts represent the majority of FDIC contract awards. Typical contract awards for non-financial goods and services (e.g., dental, life, and vision insurance for employees; subscription services; office supplies; security guard services; facilities management services; and IT services) may range from $300 million to $500 million annually.

With a reduced annual contract award value, large dollar recurring contracts can significantly impact the overall contract award value to MWOBs. To demonstrate this challenge, the FDIC awarded 737 contracts in 2017. However, four contracts (less than one percent of the total new contracts awarded) represented $186.5 million of the 2017 total contract dollars awarded (35.6 percent of the total dollars awarded). These contracts were for facilities management of the FDIC’s headquarters buildings, operation of the FDIC’s headquarters student residence center and cafeterias, nationwide employee relocation services, and life insurance services for FDIC employees. The FDIC performed extensive market research for these requirements to identify MWOB firms, explore alternative strategies for how these services could be procured, and determine how the services could be provided to increase MWOB participation. Unfortunately, none of these strategies were successful in awarding contracts for these services to MWOBs. However, although the percentage of total contract dollars awarded to MWOBs in 2017 remained the same as that in 2016, the percentage of contracts awarded to MWOBs increased from 24.3 in 2016 to 28.5 in 2017.

While smaller firms that are not national in scope are capable of providing some of the FDIC’s required recurring services, there are significant administrative advantages to having fewer contractors provide these services to ensure consistent implementation of FDIC programs throughout the FDIC’s 80 plus offices nationwide.

An additional challenge the FDIC will face is the unknown impact on new contract awards that the implementation of updated National Institute of Standards and Technology (NIST) security standards will have on future FDIC contracts where the FDIC provides confidential, sensitive, or personally identifiable information to a contractor who hosts the information on a third party system that is not directly owned by the federal government or FDIC. These updated standards include additional information technology security controls that are not currently included in FDIC contracts. The FDIC will monitor the impact very closely and make adjustments where possible.

Despite the decline in the overall contract dollars, the FDIC through its aggressive outreach program continues to educate and equip MWOBs with the tools they need to compete for contracting opportunities. The FDIC will continue to assess and analyze future contracting needs to determine where MWOB opportunities may exist or if new methods of service delivery are feasible.

Employment at the FDIC: Increasing Representation of Minorities and Women

The FDIC is strongly committed to diversity and inclusion at all levels of the agency’s workforce. The following sections provide information on the agency’s diversity in employment and hiring, initiatives to promote diversity in employment, and challenges the agency faces in promoting diversity in employment and hiring.

Diversity in Employment and Hiring

As of December 31, 2017, minorities accounted for 28.7 percent (1,748) of the FDIC’s total workforce (permanent and non-permanent) of 6,093 employees, and women accounted for 44.8 percent (2,730). [See Figure 8.] More specifically, the representation percentages in the total workforce for various minority groups at the end of December 2017 were as follows: 1.3 percent for people of two or more races, 0.5 percent American Indian and Alaska Native (AIAN), 5.5 percent Asian American, 17.5 percent Black American, and 3.9 percent Hispanic American.

Figure 8 Diversity in Total – (Permanent and Non-Permanent) Employment as of 12/31/2017

| Minority | Non-Minority | Total | |

|---|---|---|---|

| Number | 1748 | 4345 | 6093 |

| Percent | 28.7 | 71.3 | 100% |

| Men | Women | Total | |

|---|---|---|---|

| Number | 3363 | 2730 | 6093 |

| Percent | 55.2 | 44.8 | 100% |

| 2 or More | AIAN | Asian | Black | Hispanic | White | Total | |

|---|---|---|---|---|---|---|---|

| Number | 79 | 31 | 333 | 1069 | 236 | 4345 | 6093 |

| Percent | 1.3% | 0.5% | 5.5% | 17.5% | 3.9% | 71.3% | 100% |

The racial, ethnic, and gender diversity of the FDIC’s workforce overall has improved slightly since the passage of DFA section 342. Minorities accounted for 26.2 percent of the FDIC’s permanent workforce as of July 31, 2010, and 29.0 percent as of December 31, 2017. The percentage of women in the FDIC’s permanent workforce was 43.6 percent as of July 31, 2010, and 44.9 percent as of December 31, 2017. [See Appendix C.]

As of December 31, 2017, minorities accounted for 18.3 percent (24) of the FDIC’s total Executive Manager (EM) workforce of 131 employees, and women accounted for 38.9 percent (51). [See Figure 9.]

Figure 9 Diversity in Total (Permanent and Non-Permanent) Employment – Executive Manager Workforce as of 12/31/2017

| Minority | Non-Minority | Total | |

|---|---|---|---|

| Number | 24 | 107 | 131 |

| Percent | 18.3 | 81.7 | 100% |

| Men | Women | Total | |

|---|---|---|---|

| Number | 80 | 51 | 131 |

| Percent | 61.1 | 38.9 | 100% |

| 2 or More | AIAN | Asian | Black | Hispanic | White | Total | |

|---|---|---|---|---|---|---|---|

| Number | 0 | 1 | 2 | 18 | 3 | 107 | 131 |

| Percent | 0 | 0.8 | 1.5 | 13.7 | 2.3 | 81.7 | 100% |

Of the FDIC’s total EM workforce, minorities accounted for 15.7 percent as of July 31, 2010, and 18.3 percent as of December 31, 2017. The percentage of women in the FDIC’s EM workforce was 25.0 percent as of July 31, 2010, and 38.9 percent as of December 31, 2017. The racial, ethnic, and gender diversity of the EM workforce overall has increased since the passage of DFA section 342.

Appendix C depicts the FDIC’s five-year trends for the total, permanent, and EM workforce for 2013 through 2017.

Initiatives to Promote Diversity in Employment

The FDIC promotes its commitment to a diverse workforce through a wide variety of methods aimed at attracting, recruiting, hiring, and retaining high-performing individuals who reflect all segments of society. The recruitment of examiners, the FDIC’s largest occupational group, is conducted primarily through the FDIC’s Corporate Employee Program (CEP). The CEP recruits and trains the FDIC’s workforce of Financial Institution Specialists (FISs), beginning examiners-in-training, in many areas.

To help with recruitment throughout 2017, OMWI tracked and informed FDIC leadership about the representation and attrition rates for CEP participants based on race, ethnicity, and gender. Reports on participation rates were prepared following each incoming class of CEP hires, and each report included the total CEP participants from the inception of the program, FISs currently onboard, and voluntary and involuntary attrition information.

For the years from the inception of the CEP in 2005, several racial, ethnic and gender groups, as well as employees with disabilities, had very low representation rates in the FDIC’s examiner workforce. To help address these issues, the FDIC has engaged in a proactive recruitment effort and used recruiting strategies that have been successful in addressing the initially low representation rates of many racial, ethnic, and gender groups. That progress is especially apparent with respect to the overall percentage of women in the examiner workforce, which increased from 33.5 percent as of December 31, 2004, to 38.8 percent as of December 31, 2017. In addition, the percentages of Black American men and women, Hispanic American women, Asian American men and women, American Indian and Alaska Native men, and White women in the overall examiner workforce all have increased since the beginning of the CEP. Despite the positive progress in those areas, the representation rates of Hispanic American women and Asian American men and women, and women of two or more races in the FDIC’s examiner workforce remain low.

Also, since the inception of the CEP, hiring rates have been at or above the percentages in the Civilian Labor Force (CLF) for American Indian and Alaska Native men and women, Black American men and women, and men of two or more races, but lower than the CLF for Asian American men and women, Hispanic American men and women, White women, and women of two or more races. The overall minority hiring rate since the inception of the CEP has been 27.6 percent, compared to the CLF of 27.7 percent; and the overall hiring rate for women is 38.3 percent, compared to the CLF of 45.3 percent. [See Figure 10.]

| Figure 10 CEP Hires Since Inception | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 or More | AIAN | Asian | Black | Hispanic | White | Total | |||||||

| Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | ||

| CEP | 14 | 17 | 4 | 11 | 36 | 55 | 173 | 112 | 33 | 44 | 434 | 878 | 1811 |

| % | 0.8 | 0.9 | 0.2 | 0.6 | 2.0 | 3.0 | 9.6 | 6.2 | 1.8 | 2.4 | 24.0 | 48.5 | 100% |

| CLF | 1.0 | 0.6 | 0.2 | 0.1 | 3.7 | 3.5 | 8.4 | 3.4 | 3.7 | 3.1 | 28.3 | 44.1 | 100% |

During 2017, the CEP hiring rates were above the CLF percentages for Asian American women, Black American women, and men and women of two or more races, and were below the CLF for American Indian and Alaska Native women and men, Asian American men, Black American men, and Hispanic American men and women. While the hiring rates appear to be normal annual fluctuation in most cases, additional targeted recruitment is needed to reach Black American men and Hispanic American women and men. [See Figure 11.] The overall hiring rate in 2017 for minorities and women was positive with both groups having little statistical disparity from the CLF.

| Figure 11 CEP Hires in 2016 (Classes 53-57) | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 or More | AIAN | Asian | Black | Hispanic | White | Total | |||||||

| Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | ||

| CEP | 3 | 2 | 0 | 0 | 7 | 3 | 14 | 2 | 3 | 1 | 35 | 76 | 146 |

| % | 2.1 | 1.4 | 0.0 | 0.0 | 4.8 | 2.1 | 9.6 | 1.4 | 2.1 | 0.7 | 24.0 | 52.1 | 100% |

| CLF | 1.0 | 0.6 | 0.2 | 0.1 | 3.7 | 3.5 | 8.4 | 3.4 | 3.7 | 3.1 | 28.3 | 44.1 | 100% |

As a significant component of the recruitment strategy for the CEP, FDIC recruiters maintained ongoing relationships with a wide range of colleges and universities. This includes 110 institutions designated as members of the Hispanic Association of Colleges and Universities, Historically Black Colleges and Universities, and other minority-serving institutions, tribal colleges and universities, and institutions with significant student populations of Asian Americans, Hispanic Americans, and women.

The FDIC corporate recruiters participated in 152 college career fairs, information sessions, and other recruitment-related campus activities throughout the United States to brand the FDIC and attract the best qualified candidates. In 2017, FDIC recruiters attended 19 national diversity outreach events and one regional outreach event to increase awareness of the FDIC as an employer of choice to professionals and students. Recruitment efforts during 2017 also included the following:

Met with key leaders in Hispanic American, Black American, Asian American, women’s, and veterans’ organizations to create awareness of FDIC careers and identify opportunities to expand outreach to their members.

Participated in the 2017 Association of Latino Professionals For America (ALPFA) National Convention where a FDIC corporate recruiter hosted a workshop entitled Money Management and Wealth Building Skills: College and Beyond to educate students on advanced money management skills that will assist them in achieving their financial goals.

Participated at the Adelante 2017 National Leadership Institute where a senior FDIC representative provided the keynote address to participants that focused on leadership and career success. A FDIC recruitment representative also conducted a plenary workshop entitled Unite for a Purpose – Why Working Together Makes Sense.

Hosted a student workshop at the 2017 Hispanic Association of Colleges and Universities (HACU) Annual Conference entitled Make Your Resume Count: Effective Skills for Developing a Resume Without Rival. The workshop provided details on how to apply critical writing techniques to enhance ones marketability to compete in today’s job market.

Hosted a workshop at the 2017 Thurgood Marshall Leadership Institute on Financial Education for students from Historically Black Colleges and Universities. The FDIC representatives also conducted informational interviews for the Corporate Employee Program (CEP) and Internship opportunities during the Leadership Institute.

Diversity and Inclusion Analytics Dashboard

Included in the FDIC’s Diversity and Inclusion Strategic Plan is the goal to develop structures and strategies to equip FDIC leaders with the ability to manage diversity, measure results, refine approaches on the basis of available data, and institutionalize a culture of inclusion. In addition, after reviewing several financial services industry regulators in 2013, the U.S. Government Accountability Office (GAO) recommended that the agencies report on efforts to measure the progress of their employment diversity and inclusion practices, including measurement outcomes as appropriate, to indicate areas for improvement as part of their annual reports to Congress.3.

3. Trends and Practices in the Financial Services Industry and Agencies after the Recent Financial Crisis, GAO-13-238, April 16, 2013

To implement its strategic plan and address the GAO recommendation, the FDIC developed a workforce analytics dashboard to provide actionable data to senior leadership on the FDIC workforce by gender and minority status, and by division/office, region, race, ethnicity, occupation, grade level, and employment type (permanent and non-permanent). The analytics dashboard has been an important management tool for diversity and inclusion since being launched on June 20, 2013. It allows FDIC senior leaders to support diversity and inclusion efforts in hiring, promotion and retention, and to identify ways to make improvements over time.

The dashboard was used during 2017 by FDIC divisions and offices to target recruitment activities to increase the pool of minority and women applicants; assess the inclusion of minorities and women at the entry, mid, and senior levels; and evaluate diversity-related issues reported in the Federal Employee Viewpoint Survey. Senior leaders have access to workforce data that are updated quarterly and give them the ability to measure progress and adjust strategies where needed. The FDIC will continue to identify additional enhancements to the dashboard that will permit senior leaders to continue understanding and advancing diversity and inclusion within their organizations.

Workforce Development Initiative

Like many other federal agencies, the FDIC faces potential succession management challenges as many of its long-term, experienced employees consider retirement. Introduced in 2014, the FDIC’s Workforce Development Initiative seeks to prepare employees to fulfill current and future workforce capability and leadership roles. This focus will help to ensure that the FDIC has a workforce positioned to meet today’s core responsibilities while preparing to fulfill its mission in the years ahead.

During 2017, the FDIC continued to develop and implement the WDI to address comprehensive succession planning needs and workforce development challenges and opportunities. The WDI is focused on four broad objectives: (1) to attract and develop talented employees across the agency; (2) to enhance the capabilities of employees through training and diverse work experiences; (3) to encourage employees to engage in active career development planning and seek leadership roles in the FDIC; and (4) to build on and strengthen the FDIC’s operations to support these efforts. Also in 2017, the succession planning survey of the WDI was expanded to include the aspirations of employees at the CG-12 through CG-15 grade levels.

In 2018, the FDIC will continue to develop and implement the strategies, programs, and infrastructure to support the attainment of these objectives in meeting its longterm workforce needs. As a member of the WDI workgroup, OMWI helps ensure that minorities and women have an equal opportunity to participate.

Challenges

A key challenge for the FDIC in promoting diversity at all levels of its workforce continues to be the ability to attract and retain minorities and women in its bank examiner workforce. The examiner occupation represents the largest occupational group at the FDIC and accounts for 45.2 percent (2,756) of the FDIC total workforce (6,093). Individuals who began their FDIC careers as examiners tend to occupy a significant percentage of executive and managerial leadership positions at the agency, as well as other non-examiner positions in the FDIC. Thus, representation rates within the examiner workforce are key elements to achieving satisfactory representation rates within the broader FDIC workforce.

Despite the overall success of the CEP in increasing the percentage of women and minorities in the examiner workforce, those percentages still remain significantly below the CLF, such as for Asian American men and women, Hispanic American women, and women of two of more races. The attrition data will continue to be monitored and strategies will be developed to improve retention. [See Figure 12.]

| Figure 12 CEP Attrition Rates | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Total | 2 or More | AIAN | Asian | Black | Hispanic | White | |||||||

| Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | Women | Men | ||

| Hired | 1811 | 14 | 17 | 4 | 11 | 36 | 55 | 173 | 112 | 33 | 44 | 434 | 878 |

| Involuntary Departures |

36 | 0 | 0 | 0 | 0 | 1 | 1 | 7 | 9 | 1 | 2 | 4 | 11 |

| Involuntary Attrition Rate+(%) |

2.0 | 0.0 | 0.0 | 0.0 | 0.0 | 2.8 | 1.8 | 4.0 | 8.0 | 3.0 | 4.5 | 0.9 | 1.3 |

| Subtotal | 1775 | 14 | 17 | 4 | 11 | 35 | 54 | 166 | 103 | 32 | 42 | 430 | 867 |

| Transfers (Mid-Career/ Other) |

36 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 3 | 2 | 1 | 13 | 13 |

| Voluntary Departures |

587 | 2 | 2 | 1 | 5 | 11 | 29 | 60 | 47 | 11 | 15 | 140 | 264 |

| Voluntary Attrition Rate *(%) |

33.1 | 14.3% | 11.8% | 25.0% | 45.5% | 31.4% | 53.7% | 36.1% | 45.6% | 34.4% | 35.7% | 32.6% | 30.4% |

| Number Retained |

1152 | 12 | 15 | 3 | 6 | 24 | 25 | 102 | 53 | 19 | 26 | 277 | 590 |

| + “Involuntary Attrition Rate” is the Involuntary Departures divided by the total hired. * “Voluntary Attrition Rate” is the Voluntary Departures divided by the subtotal. | |||||||||||||

In the non-examiner occupations of economists, financial administration, accountant/ auditors, attorneys, and general business and industry, the FDIC faces challenges in attracting and recruiting minorities and women, primarily due to low representation rates for minority groups and women in these occupations. [See Appendix D.]

Overall, minorities fall below the relevant CLF in the economist occupation, with Hispanic American men, Black American men, and Asian American men having low participation rates and Hispanic American women, American Indian and Alaska Native men and women, and men and women of two or more races being absent.

In the financial administration and program occupation, Women, Hispanic American men and women, White women, and American Indian or Alaska Native men fall below the CLF. Women of two or more races are absent. Women, Hispanic American men and women, White women, Black American women, Asian American women, American Indian or Alaska Native women, and women of two or more races fall below the CLF in the general business and industry occupation. Men, White men, Black American men, Asian American men, American Indian and Alaska Native men, and men of two or more races all exceed the relevant CLF for this occupation.

For the accountant/auditor occupations, Hispanic American men and women and American Indian and Alaskan Native men and women, and women of two or more races are absent. White women and Asian American men have a low representation compared to the relevant CLF for the accountant/auditor occupation.

In the attorney occupation, the level of representation for some groups is not as pronounced as it is in other occupations. Hispanic American men and women, Asian American men, and women of two or more races have participation rates slightly below the relevant CLF in the attorney occupation.

In the general business and industry occupation, the low participation rates appear to be concentrated among women, with women overall and in each separate group being below the relevant CLF. Hispanic American men are represented at a rate slightly below the relevant CLF, while men in all other groups have rates above the relevant CLF.

To address the participation rates of the groups noted above in the non-examiner occupations, the FDIC recruitment plan includes strategies intended to increase outreach to prospective applicants in underrepresented groups at the entry, mid, and senior levels in these occupations throughout the agency. The plan includes reaching out to professional organizations, colleges and universities, and affinity groups.

In 2017, the FDIC continued monitoring race, ethnicity, gender, and grade levels by FDIC divisions and offices. As a result, the FDIC continues expanding outreach and recruitment more broadly to increase minority and women representation at senior levels within the FDIC. Also, the FDIC updated and continued implementing its Diversity and Inclusion Strategic Plan, which is designed to develop an integrated view of diversity and inclusion, strategically monitor and manage the employment life cycle (hire to retire), and address challenges at the FDIC.

Other Activities

Status of DFA Section 342 Regulated Entity Requirements

The FDIC OMWI continued to work closely with the OMWI Directors of the Office of the Comptroller of the Currency (OCC), the National Credit Union Administration (NCUA), the Federal Reserve Board (FRB), the Consumer Financial Protection Bureau (CFPB), and the Securities and Exchange Commission (SEC) to further implement Section 342(b)(2)(C) of the Dodd-Frank Act, which required regulatory agencies to develop standards to assess the diversity policies and practices of the entities they regulate. After publishing the final Interagency Policy Statement Establishing Joint Standards for Assessing the Diversity Policies and Practices of Regulated Entities (Policy Statement) in the Federal Register in June 2015, the FDIC sought approval from OMB to collect assessment information from their regulated entities.

In October 2016, the Acting Director, OMWI, distributed a letter to Presidents and Chief Executive Officers of FDIC-regulated financial institutions identified as having 100 or more employees. The letter informed the institutions about the Policy Statement, OMB’s approval for the FDIC to voluntarily collect information from its regulated institutions, and encouraged the institutions to make their assessment information public.

To facilitate the uniform and systematic collection of assessment information, the FDIC developed a self-assessment template. The Diversity Self-Assessment of FDIC Regulated Financial Institutions (Diversity Self-Assessment) instrument was designed to assist financial institutions with conducting assessments of their diversity policies and practices using the standards identified in the Policy Statement.

In March 2017, the Acting Director, OMWI, distributed a reminder letter to financial institutions encouraging them to conduct voluntary self-assessments. The letter not only encouraged institutions to submit a self-assessment, it served to inform institutions about the Diversity Self-Assessment instrument and the availability of other resources on the FDIC web site.

The FDIC received 95 of 805 (11.8 percent) self-assessments from its regulated financial institutions for the 2016 reporting period. Most of the financial institutions used the instrument to assess their diversity program.

While the FDIC is pleased with the participation of financial institutions for this initial effort, it will take steps to increase voluntary participation rates. The FDIC OMWI will continue to raise awareness amongst FDIC-regulated financial institutions by identifying leading trends and practices, and establishing benchmarks designed to build a strong culture in diversity and inclusion.

The FDIC will emphasize to its regulated institutions the value of conducting voluntary self-assessments, annually submitting assessment results to the OMWI Director, and making diversity information transparent to the public. Moreover, the FDIC may use the information received to monitor progress and trends in the financial services industry with regard to diversity and inclusion in employment and contracting activities.

The Diversity Self-Assessment instrument, the associated guidance for completing and submitting the assessment, and other resources are available on the FDIC’s website at www.fdic.gov/about/diversity.

Contractor Workforce

Section 342(c) of the DFA requires that OMWI ensure, to the maximum extent possible, the fair inclusion of minorities, women, and minority- and women-owned businesses in all business activities of the agency, including procurement. Following passage of the DFA, OMWI worked with FDIC’s Acquisition Services Branch (ASB) and Legal Division to develop a “Fair Inclusion” contract clause for all awards over $100,000. This award amount is the agency threshold for contracts that must follow formal contract award procedures. The clause notifies contractors of the responsibility to include minorities and women in their workforce and advises of remediation action the FDIC may take if it is determined the contractor has failed to do so. OMWI developed the Contractor Workforce Review Process (CWRP) in collaboration with ASB and the Legal Division to assess a contractor’s good faith efforts. The CWRP encompasses existing FDIC procurement policies and practices that support the requirements of section 342(c) of DFA.

Good faith efforts are defined as actions contractors undertake to identify, and, if present, remove barriers to employment or expansion of employment opportunities for minorities and women. Contractors that seek to do business with the FDIC must provide a written statement, known as the Fair Inclusion Certification, stating their commitment to making a good faith effort. To verify their commitment, agency contractors, upon written request from the FDIC, are asked to provide documentation that supports the actions they have undertaken to demonstrate their good faith effort to ensure the fair inclusion of minorities and women in their workforce.

In 2017, OMWI continued implementation of the CWRP in collaboration with ASB and the Legal Division. Fifty contractors, currently doing business with the FDIC, were selected to provide information on their good faith efforts to ensure the fair inclusion of minorities and women in their workforce, and, if applicable, subcontractors.

Contractors were selected from all active FDIC awards issued after September 1, 2011, and valued over $100,000. These were contractors subject to the Fair Inclusion clause requirements. The fifty contractors represented approximately 22 percent of eligible awards and covered a wide range of sectors as defined under the NAICS Codes. The size of the contractors ranged from small companies that employed less than fifty people up to large corporations that employed thousands.

The selected contractors were asked to provide a copy of their plan that outlines their good faith efforts to include women and minorities in the workforce; demographic data; and other documentation that demonstrated their commitment. Many contractors leveraged information already prepared to comply with Federal Equal Employment Opportunity (EEO) and Affirmative Action (AA) requirements. For those contractors not subject to mandatory EEO or AA recordkeeping and reporting requirements, the FDIC met with representatives to discuss what other readily available information existed such as, outreach activities, diversity training, partnerships with professional organizations, etc. The FDIC followed up as needed to obtain clarification on good faith effort activities. At the conclusion of the review, it was determined all contractors reviewed had made, were making, or had a plan in place to make good faith efforts to include women and minorities in their workforce.

Promoting Financial Access and Financial Literacy

Financial education helps consumers understand and use bank products effectively and sustain a banking relationship over time. The FDIC continued to be a leader in developing high-quality, free financial educational resources and pursuing collaborations to use those tools to educate the public. In particular, the FDIC designed strategies to reach two particular segments of the population that the National Survey of Unbanked and Underbanked Consumers revealed are disproportionately unbanked and underbanked: low- and moderate-income (LMI) young people and people with disabilities. The FDIC’s work during 2017 focusing on young people was also consistent with the Financial Literacy and Education Commission’s (FLEC) focus on Starting Early for Financial Success.

Youth Financial Education

Recognizing the promise of hands-on learning approaches, the FDIC’s youth work centered on helping banks understand strategies to connect financial education to savings accounts. In 2017, the FDIC released the Youth Savings Pilot report which examines the experiences of 21 diverse banks in designing and implementing youth savings programs. The report describes promising practices banks can use to develop or expand their own youth savings programs. The report is accessible through the new Youth Banking Resource Center that had more than 8,200 page views between its launch in late March to the end of December. The release of the report was followed by a webinar to communicate to financial institutions key practices identified during the Pilot.

FDIC launched the Youth Banking Network to support banks as they work with school and nonprofit partners to develop youth savings programs using the knowledge gained from the Pilot. The FDIC convened three Network conference calls that focused on topics of interest, including program design and financial education delivery. Bankers and other experts shared their experiences and promising practices. The FDIC provided periodic assistance to members in response to specific questions.

The FDIC also shared key lessons learned from the Youth Savings Pilot during two national webinars focused on Money Smart resources for teaching youth. Both webinars featured experts and practitioners discussing the delivery of effective financial education including how the Money Smart for Young People curriculum can be used. The Teacher Online Resource Center was also redesigned to allow educators to easily find Money Smart for Young People and other relevant resources. Other enhancements to the site include new videos that provide a quick overview of the curriculum tools and links to relevant resources that can support the delivery of financial education in the classroom. The site had more than 9,000 visits during 2017.

The FDIC pursued strategies to improve financial education and access to mainstream financial services for youth participating in youth employment programs, including those funded through the Workforce Innovation and Opportunity Act (WIOA). For workforce providers and their partners teaching financial education, the FDIC developed a tool to map Money Smart to WIOA’s financial education element. The FDIC also released a supplement to Money Smart designed to help prepare youth to open their first savings or transactional accounts. As a member of the FLEC, the FDIC helped develop two resource guides for financial institutions and youth employment program providers to discuss opportunities of mutual benefit.

The FDIC also led three webinars in collaboration with the Department of Labor to increase awareness of Money Smart among organizations that receive federal funding for youth employment. In addition, the FDIC participated in three regional events in collaboration with the Department of Labor and Federal Reserve Banks to strengthen the capacity of workforce development organizations to work with financial institutions on financial capability initiatives. The FDIC was selected to hold a “quick shop” and a panel presentation at two national workforce association events.

The FDIC Money Smart Alliance is a network of diverse organizations that use Money Smart to provide financial education training to organizations, consumers, and small businesses. Money Smart is available in nine languages plus large print and Braille. The FDIC hosted a national webinar on February 28, 2017, to discuss the Money Smart Alliance and opportunities to join the Alliance. The FDIC web site also now features a searchable database of Alliance members to help facilitate collaborations among organizations to use Money Smart and to help consumers find training. The FDIC also continued to provide technical assistance to Alliance members to support their implementation of Money Smart. For example, a ‘peer-to-peer’ learning webinar for Alliance members featured representatives of a financial institution and a nonprofit organization discussing how they use Money Smart.

During 2017, 287 organizations joined the Money Smart Alliance. Moreover, 545 organizations have renewed membership or joined the Alliance since the inception of the new enrollment process in early 2016; and 272 of the Alliance members report using Money Smart for Small Business.

Financial Education for Adults Including Persons with Disabilities

The FDIC emphasized strategies to promote economic inclusion for people with disabilities given this population is disproportionally unbanked and underbanked. As one element of these strategies, the FDIC expanded efforts with local partners through 14 community events to bring banks and organizations representing people with disabilities together at both the state and local levels.

Together with the CFPB, the FDIC hosted organizations that support people with disabilities at Gallaudet University in May. The organizations are part of CFPB’s Focus on Disabilities cohort and together they learned about CFPB’s Your Money, Your Goals toolkit and the FDIC’s Money Smart financial education program. The event was followed by two in-person training sessions and two webinars to further assist members of the cohort advance financial capability for persons with disabilities.

The FDIC also revised the Guide to Presenting Money Smart for Adults that includes updated information to help instructors support participants with disabilities, including additional tips about reasonable accommodations and sample language to include on registration forms. The FDIC also produced the Instructor’s Guide Supplement the have four scenarios featuring individuals with disabilities dealing with a financial situation in their lives.

In 2017, the FDIC began to revise and update the instructor-led Money Smart for Adults curriculum to ensure accuracy and relevance. Five organizations, including two banks, tested three of the redeveloped draft modules that provide education to their clients. The feedback from these organizations provided valuable information that helped form the redevelopment of the remaining modules. All of the modules in the redeveloped curriculum will be tested and released in 2018.

Money Smart for Small Business

The FDIC continues to highlight the Money Smart for Small Business curriculum with a focus on informational events for bankers, community organizations, and entrepreneurs – and on increasing partnerships at the state and local levels for small business access to credit resources. In collaboration with diverse partners, particularly the Small Business Administration and its partner network (i.e., Small Business Development Centers, Women’s Business Centers and SCORE chapters), the FDIC convened forums and roundtables featuring safe small business products and services and provided information and technical assistance to support initiatives geared to increase access to capital for small businesses. In 2017, the Community Affairs Branch completed 82 events and activities primarily focused on small business.

The FDIC supported community development and economic inclusion partnerships at the local level by providing technical assistance and information resources throughout the country, with a focus on unbanked and underbanked households and low- and moderate-income communities. The Community Affairs staff supports economic inclusion initiatives through work with the Alliances for Economic Inclusion (AEI), Bank On initiatives, and other coalitions originated by local and state governments, and through collaboration with federal partners and many local and national non-profit organizations. The FDIC also partnered with other financial regulatory agencies to provide information and community development technical assistance to banks and community leaders across the country.

In the 12 AEI communities, the FDIC helped working groups of bankers and community leaders develop responses to the financial capability and services needs in their communities. To integrate financial capability into community services more effectively, the FDIC supported the following activities: seminars and training sessions for community service providers and asset building organizations; workshops for financial coaches and counselors; promotion of savings opportunities for LMI individuals and communities; initiatives to expand access to savings accounts for all ages; outreach to bring numerous people to tax preparation assistance sites; and education for business owners to help them become bankable.

The FDIC worked in ten Bank On communities to convene 15 forums and roundtables that helped advance strategies to expand access to safe and affordable deposit accounts and engage unbanked and underbanked consumers. In collaboration with Cities for Financial Empowerment Fund, the FDIC provided technical assistance to bankers, coalition leaders, and others interested in understanding opportunities for banking services designed to meet the needs of the unbanked and underbanked.

Also, the FDIC’s Advisory Committee on Economic Inclusion held meetings in 2017. The Committee continued to provide the FDIC with advice and recommendations on important initiatives focusing on expanding access to banking services for underserved populations. The April meeting summarized highlights of the FDIC’s Economic Inclusion Summit, discussed access to neighborhood bank branches, and described how banks can better access affordable mortgage lending resources. The October meeting featured panel discussions on safe accounts, the 2016 FDIC Bank Survey results, and economic inclusion for persons with disabilities. An update on access to neighborhood bank branches was also given.

Minority Depository Institution Activities

The preservation of minority depository institutions (MDI) remains a high priority for the FDIC. In 2017, the FDIC continued to support MDI and Community Development Financial Institution (CDFI) industry-led strategies for success. These strategies include increasing collaboration between MDI and CDFI bankers; partnering to share costs, raise capital, or pool loans; and making innovative use of federal programs. The FDIC supports this effort by providing technical assistance to MDI and CDFI bankers.