|

Home > Regulation & Examinations >

Bank Examinations >

Credit Card Securitization Manual |

|||

|

Credit Card Securitization Manual

Chapter III. – Accounting for Credit Card Securitizations Introduction III ACCOUNTING FOR CREDIT CARD SECURITIZATIONS INTRODUCTION This section provides an overview of the accounting criteria for establishing sales treatment under Financial Accounting Standards Board (FAS) Statement No. 140, Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities (FAS 140), in the securitization of credit card receivables. FAS 140 was issued in September 2000 and replaces the similarly titled FAS Statement No. 125, but continues to carry over most of the provisions of FAS 125. Examiners should have a basic understanding of the accounting rules that govern credit card securitization transactions. This section is designed to provide examiners with this understanding, but it is not all inclusive. Examiners should seek the assistance of accounting subject matter experts and regional accountants for additional assistance and resource materials. Examiners reviewing securitization accounting should be familiar with the actual pronouncement and various other resources that offer further implementation guidance. In order to be consistent with the language in FAS 140, this chapter uses the term "transferor" when referring to the financial institution being examined versus the terms originator/seller used in other chapters. Typically, the transferor is also the servicer of the credit card receivables. FAS 140 applies to all transfers of financial assets after March 31, 2001 by both public and private entities. It is based on a "financial-components" approach, which focuses on legal and physical control of the transferred assets and recognizes that financial assets and liabilities can be separated into a variety of components. Under this approach, an entity recognizes the financial and servicing assets it controls as well as the liabilities it incurs. The entity also derecognizes financial assets for which control has been surrendered and liabilities that have been extinguished. FAS 140 is designed to provide consistent standards for distinguishing transfers that are accounted for as sales from those that are accounted for as secured borrowings. There is a common misconception that the entire securitization is either accounted for as a sale or a financing, but a securitization can really be accounted for in one of five ways7:

FAS 140 provides consistent standards for determining whether or not a transfer of financial assets constitutes a sale, calculating the gain or loss on the initial transfer of financial assets and/or extinguishment of liabilities as well as gains or losses on subsequent transfers, initially measuring and recording the interests that continue to be held by the transferor in the securitization transaction, subsequently measuring other interests that continue to be held by the transferor, and reporting and disclosing the transactions. It is important to note that the term "transferred assets" is not synonymous with the term "sold assets." TRANSFER OF ASSETS Paragraph 9 of FAS 140 establishes specific criteria to determine when control of financial assets is surrendered by the transferor. If control is deemed surrendered, those financial assets, other than the beneficial interest, will be accounted for as a sale to the extent that consideration is received in exchange for the assets transferred. Control is considered to be surrendered only if all of the following conditions are met:

CALL OPTIONS AND ROAPS Call options and ROAPS allow transferred assets to be reclaimed and must be evaluated to determine whether or not they result in the transferor maintaining effective control over the transferred assets. The unilateral ability to cause the return of specific transferred assets precludes sale accounting because the effective control is maintained rather than surrendered, which is a necessary element to achieve sale accounting. An attached call held by the transferor could result in the transferor maintaining effective control when the attached call gives the transferor the unilateral ability to cause the holder of a specified asset to return the assets. As such, a call option that allows a transferor to call transferred assets when amortized to a specific balance sheet at the date of transfer would preclude sales treatment only on the portion of assets that can be called, if not considered a clean-up call (discussed below). For example, if a transferor transfers financial assets, but retains a call option on those assets when they have amortized to 25 percent of the transferred balance, that 25% would be considered a financing that would have to be accounted for as a secured borrowing. In addition, a transferor that maintains the ability to call the transferred assets when they amortize to 25 percent of the transferred balance cannot treat the call option as a 10 percent clean-up call and a 15 percent non-clean-up call. Calls embedded (embedded call) by the issuer do not preclude sale accounting because the issuer rather than the transferor holds the call (paragraphs 50-54). In accordance with paragraph 87, securitization transactions that include the following ROAPS are permissible and do not preclude sales treatment:

The specific assets repurchased and the timing of the repurchase is determined by a triggering event, not by the transferor, and the repurchase must take place regardless of the transferor's intent. When the event is triggered, it is viewed as a repurchase of the receivables, which assumes the purchase is made at fair value. Examiners should keep in mind, however, that a transferor does not have to exercise a call option or a ROAPS for sale accounting to be prohibited. If effective control is maintained by the transferor then sale accounting is precluded. For example, effective control is maintained by the mere inclusion of a call option that gives the transferor the ability to reclaim specific assets for more than a trivial benefit. The FAS 140 implementation guide, noted later, provides a good reference table for evaluating call options and ROAPS. Clean-up call options are permitted exceptions to the effective control requirements of FAS 140. They are options that represent the transferor/servicer's (only if the transferor is also the servicer) right to purchase the remaining transferred financial assets (credit card receivables) if the amount of the outstanding assets falls to a level where the cost of servicing them becomes burdensome in relation to the benefits of servicing. In the final rule on the Capital Treatment of Recourse, Direct Credit Substitutes, and Residual Interest in Asset Securitizations, published in November 2001 and effective January 1, 2002, the Federal banking agencies stated that clean-up calls that are 10 percent or less of the original amount of receivables sold to third parties from the asset pool and that are exercisable at the option of the banking organization are not considered recourse or direct credit substitutes.11 Question 49 of FASB's A Guide to Implementation of Statement 140 on Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities, issued in February 2001 and revised in April 2002, discusses sale accounting treatment when calls exist, including an illustrative table summarizing FAS 140's provisions for different types of rights of a transferor to reacquire transferred assets. Upon the completion of a transfer of credit card receivables, assuming the transaction satisfies all the conditions to be accounted for as a sale (paragraph 9), the transferor is required to:

DETERMINING GAIN OR LOSS ON SALE Any interests that continue to be held by the transferor in the transferred assets, such as servicing assets and any other interest retained by the transferor, continue to be carried on the transferor's balance sheet. The transferor must complete a relative fair value allocation process of the previous carrying amounts of the assets sold and the interests that continue to be held by the transferor. In March 2006, FASB Statement No. 156 (FAS 156), Accounting for Servicing of Financial Assets, an amendment of FAS Statement No. 140, was issued. Entities could have adopted it as early as January 2006 but must adopt by January 2007. With the issuance of FAS 156, the transferor will no longer include servicing assets or liabilities in its relative fair value allocation model. This manual incorporates the impact of FAS 156, which establishes, among other things, the accounting for all separately recognized servicing assets and liabilities. Upon the completion of the transfer of financial assets, the transferor must first initially recognize and measure at fair value any servicing asset or liability each time it undertakes an obligation to service financial assets, identify the carrying value of all the elements transferred at the date of transfer (net of loss allowances, if any); identify any interests that continue to be held and any liabilities incurred as a result of the securitization; and estimate the fair value of each element obtained, held, or incurred. Next, the transferor must allocate the previous carrying value of the assets transferred and the interests that continue to be held by the transferor based on their relative fair values. The relative fair value is based on the date the assets were transferred (paragraphs 56-60). Determining whether the assumptions and the valuation model used to determine the fair values are realistic and appropriate is discussed further in the Residual Interest Valuation and Modeling chapter. In general, proceeds from receivables sales consist of the cash and any other assets obtained, including separately recognized servicing assets, less any liabilities incurred, including any separately recognized servicing liabilities. The gain or loss on credit card securitizations is limited to the receivables that have been sold at the inception of the securitization. Likewise, the servicing asset or liability recognized is limited to the servicing of the receivables sold at inception (a bank cannot book a servicing asset on anticipated future receivables to be sold to the trust.) As subsequent smaller monthly transfers occur in the revolving period, gain or loss on sale, beneficial interests, and assets and liabilities continue to be recognized consistent with FAS 140. SERVICING ASSETS/LIABILITIES When the right to service the sold credit card receivables is obtained and contractually separated from the underlying sold receivables, the servicing becomes a distinct and separate asset (or liability). A bank must recognize a serving asset when it contractually agrees to service the receivables as a result of the transfer of its own receivables (which qualify for sales treatment) or acquires or assumes the servicing responsibility from another servicer.

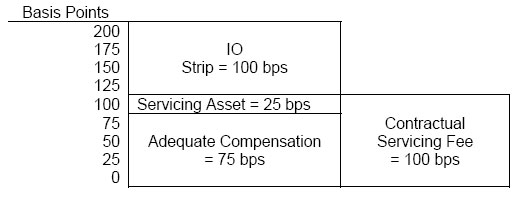

INTEREST-ONLY STRIPS (IO Strips) IO strips represent the present value of the expected future excess spread from the sold credit card receivables. IO strips are generally subordinated interests that provide additional credit enhancement to the certificate holders, and therefore, are recorded as an "other asset" on the seller/servicers balance sheet and report of condition. They are often referred to in this manual as credit-enhancing IO strips or CE IO strips. IO strips are created when there is excess interest and fee income after all servicing costs, credit losses, investor coupon, and any other required fees (such as premiums to a third-party insurer) are paid. Interest and fee income, together referred to as the yield, consist of annual percentage rate (APR) charges and any late fees or other fees (cash advance, overlimit, annual, nonsufficent funds (NSF), etc.). Interchange fees are not part of the IO strip calculation. Again, an IO strip can only be created for receivables sold; any interchange fee that may be generated in the future is not a component of a sold receivable, but a component of the account holders' future transactions and possible future receivables at various merchants. Similarly, cash advance fees are also excluded from the IO strip calculation. Cash advance fees are not typically incurred on existing receivables; instead they are incurred at the time the cash is advanced and the receivable is created. The IO strip is calculated based on the anticipated excess spread generated by the sold credit card receivables. The following is an example of how excess spread is calculated:

IO strips are initially recorded at allocated cost relative to fair value. The initial recorded amount is then adjusted up or down through earnings (if held in a trading account) or equity via other comprehensive income (if accounted for as available for sale) based on the asset's fair value. The seller/servicer accretes the asset into interest income. The IO strip is reported as an other asset but measured at its fair value, similar to an available-for-sale or trading security, and is periodically assessed for impairment (EITF 99-20). Fair value estimates (and thus any impairment) are based on continual evaluation of the cash flows over the expected life of the IO strip. FAS 140 does not dictate a specific method for estimating fair value of an asset; however, the statement does provide guidance in determining the fair value of an asset. Determining the reasonableness of the fair value calculation's assumptions and technique are discussed in the Residual Interest Valuation and Modeling chapter. ACCRUED INTEREST RECEIVABLE (AIR) The AIR asset represents the transferor's (seller's) subordinated residual interest in cash flows that are initially allocated to the investors' portion of a credit card securitization. Prior to the securitization transaction, the transferor directly owns a pool of credit card receivables, including the right to receive all of the accrued fees and finance charges on those receivables. However, through the securitization process, the seller's right to the cash flows from the collection of the accrued fees and finance charges generally is subordinated to the rights of the other beneficial interest holders. When the seller's (transferor's) right to the AIR cash flows is subordinated, the seller generally should include the AIR as one of the financial components in the initial accounting for the sale of the receivables and in computing the gain or loss on sale. It is important to understand the close relationship, but also the different characteristics, between AIR and the IO strip. The IO strip represents future income to be earned (subject to both prepayment risk and credit risk) whereas the AIR represents interest and fees already earned at a point in time and recognized under accrual accounting (subject to credit risk but not prepayment risk). The AIR typically includes the transferor's residual interest in the investors' portions of the billed but uncollected accrued fees and finance charges as well as the accrued but unbilled fees and finance charges. Initially, the AIR is recorded at its allocated carrying amount, which is typically less than its face amount. Subsequent to the securitization, the AIR should be accounted for on its allocated cost basis. Entities should follow existing applicable accounting standards, including FAS Statement No. 5, Accounting for Contingencies, in subsequent accounting for the AIR asset. The AIR is reported as an "other asset" for call report purposes. The Federal banking agencies issued FIL-131-2002, The Interagency Advisory on the Accounting Treatment of Accrued Interest Receivable Related to Credit Card Securitizations, on December 4, 2002. Subsequently, FASB issued a Staff Position (FSP) FAS140-1 (April 2003) entitled, Accounting for Accrued Interest Receivable Related to Securitized and Sold Receivables under FAS Statement No. 140." The advisory and the staff position describe the accounting guidance for AIR. In addition, because the AIR is a retained beneficial interest, Emerging Issues Task Force (EITF) Issue No. 99-20 also applies to the subsequent accounting. AIR is discussed further in the Residual Interest Valuation and Modeling and the Regulatory Capital chapters. CREDIT CARD SECURITIZATION EXAMPLE Exhibit C illustrates a simplified example of a credit card transaction and is intended to give examiners a brief overview of the initial accounting treatments for the various elements of the transaction. The example involves issuing two bond classes with a four year maturity. Exhibit C13

7 See: Deloitte & Touche, LLP, Securitization Accounting: The Ins and Outs (And Some Do's and Don'ts) of FAS 140, FIN 46R, IAS 39, and More...," June 2005 edition. 8 FAS 140 uses the term "beneficial interest," which for credit card securitizations typically is in the form of a pass-through ownership interest in the transferred assets. Beneficial interests in the same underlying assets do not constitute having received proceeds for the purposes of FAS 140 (e.g. seller's interest). 9 The American Institute of Certified Public Accountants has issued guidance on lawyers' letters in an auditing interpretations called "The Use of Legal Interpretations as Evidential Matter to Support Management's Assertion That a Transfer of Financial Assets Has Met the Isolation Criteria in Paragraph 9(a) of Statement of Financial Accounting Standards No. 140." [AICPA §UA9336.01-.21] 10 Or, if the transferee is a QSPE (paragraph 35), each holder of its beneficial interest. 11 "Interagency Questions and Answers on the Capital Treatment of Recourse, Direct Credit Substitutes, and Residual Interest in Asset Securitizations" issued in FIL-54-2002 on May 24, 2002. 12 Deloitte & Touche, LLP, Securitization Accounting: The Ins and Outs (And Some Do's and Don'ts) of FAS 140, FIN 46R, IAS 39, and More...," June 2005 edition. 13 The inspiration for this example is Deloitte & Touche, LLP's, Securitization Accounting Under FASB 140, January 2002, but the example was altered to reflect the issuance of FAS 156 Accounting for Servicing of Financial Assets, an amendment of FAS Statement No. 140. 14 For simplicity reasons, the fair value of the seller's interest in this example is assumed to equal book value. In reality, the fair value should be different with management appropriately supporting the fair value. 15 The fair value is allocated to the net carrying value of the assets, in this case $637,000,000, using the appropriate percentages (e.g. $637,000,000 x .7576 = $482,591,200). 16 Cash Proceeds: Fair Value of Class A & B ($525,000,000) less non-deferred transaction cost ($4,000,000 x .25) = $524,000,000. 17 Class A ($500,000,000) + Class B ($25,000,000) – transaction costs ($4,000,000) = $521,000,000. 18 The $4,000,000 in transaction costs are deferred over the 4 year term of the deal. 19 Adjust allocated carrying values of interests that continue to be held by the transferor to fair value in accordance with FAS 140 ($10,000,000 - $9,618,700 = $381,300). 20 Could also be to P&L if interests that continue to be held by the transferor were classified as trading. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Last Updated 05/24/2007 | supervision@fdic.gov | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||